Rising bond yields threaten financial markets

May 6, 2021·Alasdair MacleodThere is a growing recognition in financial circles that price inflation will increase significantly in the near future, and official estimates that it will be a temporary phenomenon limited to an average of 2% are overly optimistic. There is, therefore, increasing speculation about the need for interest rates to rise.

The bond yield on 10-year US Treasuries has already more than doubled over the last year. It is in the nature of market cycles for equity and other financial assets to continue to rise in value during an initial increase in bond yields. It is the second increase that can be expected to turn bullish optimism about the economic outlook into the beginning of a bear market. Financial markets, already dislocated from fundamental realities, appear to be acutely vulnerable to such a change in sentiment.

This article points out that equity markets are driven more by money flows rather than perceived economic prospects. Bank credit for industry is contracting, commodity prices are soaring, and supply chains remain disrupted. Fuelled by earlier expansions of money supply and further expansions to come, the world faces a far larger increase in price inflation than currently contemplated, and therefore far higher interest rates, threatening to destabilise both financial markets and fiat currencies.

Public participation in equity markets is at an all-time high, not just through direct holdings — amateurish speculation is rife — but through passive index tracking funds and the like. With respect to these, the underlying assumption financial advisors make and tell their innocent clients is that trackers are risk free, because exposure to individual corporate failures is so diluted as to be immaterial. And over time, markets always rise, captured by investing in these funds. But this is deception, ignoring market cycles and systemic risks. Ignorance of the inevitable cyclical switch from greed for profits to fear of loss that defines the divide between bull and bear markets invalidates the permabulls’ advice.

Without doubt, the prowling bear in our so far untroubled scene is bond yields. Unnoticed, they have begun to rise as shown in the chart heading this article. With increasing urgency, it is time to consider the effect on market relationships. Over many investing cycles it has been observed that bond prices conventionally top out before equities. It is one of the most reliable warning signs, which, despite its track record is routinely dismissed by wishful thinkers until it is too late.

Instead, it is a commonplace to argue that prospects for corporate profits have improved at this stage of the economic cycle because of the growing certainty of a better economic outlook. And now that this time the civilised world is emerging from lockdowns, every analyst in the mainstream media delivers this message. For them, the rise in bond yields confirms that improving business conditions are in place to justify yet higher equity prices. But it is all a cycle, having little to do with economic prospects.

Today, we see that the relationship between declining bond prices and rising equities, and all the sentiment and commentary around them, are as we should expect.. But beware the bear lurking in the woods. It’s the second rise in bond yields that often slays the equity bull. I vividly recall meeting an industrialist the autumn of 1972, who told me that his business was the best it ever had been. He then paraded his ignorance of financial matters by telling me that it was wholly irresponsible for the London Stock Exchange to permit the FT 30 share index to have halved in the previous fifteen months. Following that conversation, the FT 30 halved again after interest rates were jacked up in October 1973, creating the infamous secondary banking crisis and losing 70% from its peak in May 1972 by January 1975. And the last I heard of the unfortunate industrialist his business had gone bust and he had committed suicide.

It is a mistake to take opinions or evidence of economic conditions as the principal reason to invest in equities. It is more important to follow the money, specifically the cycle of bank credit. While amateur investors are buying into equity market tops, bankers begin to see that the early signs of rising interest rates are disrupting business plans and will lead inevitably to corporate failures. This comes at a time when their own balance sheets are most highly leveraged. With this credit cycle, there are some additional features specific to it. Even though the ending of pandemic restrictions is expected to lead to a substantial recovery in economic activity, these extra features are extreme, and the bear case is therefore strong.

Banks have begun to withdraw credit from non-financial sector borrowers, meaning they will lack the finance to process and deliver goods to meet increasing demand. Banks are also over-leveraged as they usually are at this stage of the credit cycle, but they have never been more so than they are this time around. The transition from banking greed to banking fear always leads to a substantial cut in bank lending, with the potential outcome of banks being forced to liquidate collateral into falling markets. Unthinkable? It would have happened every credit cycle without central banks taking action to avoid it — which they have achieved every time so far since the 1930s. And consider interest rates, which are already at zero, and negative in euros, yen and Swiss francs. Where can they go to rescue a global economy failing for lack of bank credit?

The stand-out indicator is always bond yields. The chart at the head of this article strongly suggests to us that after the current pause they are heading higher — probably much higher. This article explains why, and what will be the consequences for financial markets. And why, despite higher bond yields, the purchasing power of fiat currencies have not only started to fall at an accelerating pace but will almost certainly continue to do so.

Immediately, almost everything began to recover with the exception of bond prices. But the initial increase in their yields can be justified on the basis that they were previously depressed by fears of deflation ahead of the spreading pandemic, and that with the worst fears of deflation had now passed a state of normality had returned. In the year following, equity markets recovered fully and have gone on to new highs. Commodity prices are now rising strongly, which so far is believed by market optimists to indicate recovering demand and therefore confirmation of economic recovery. Having some time ago changed the inflation target from 2% to an average of 2% over time, only last week the Fed saw no reason to expect a rise in price inflation to be more than a temporary phenomenon.

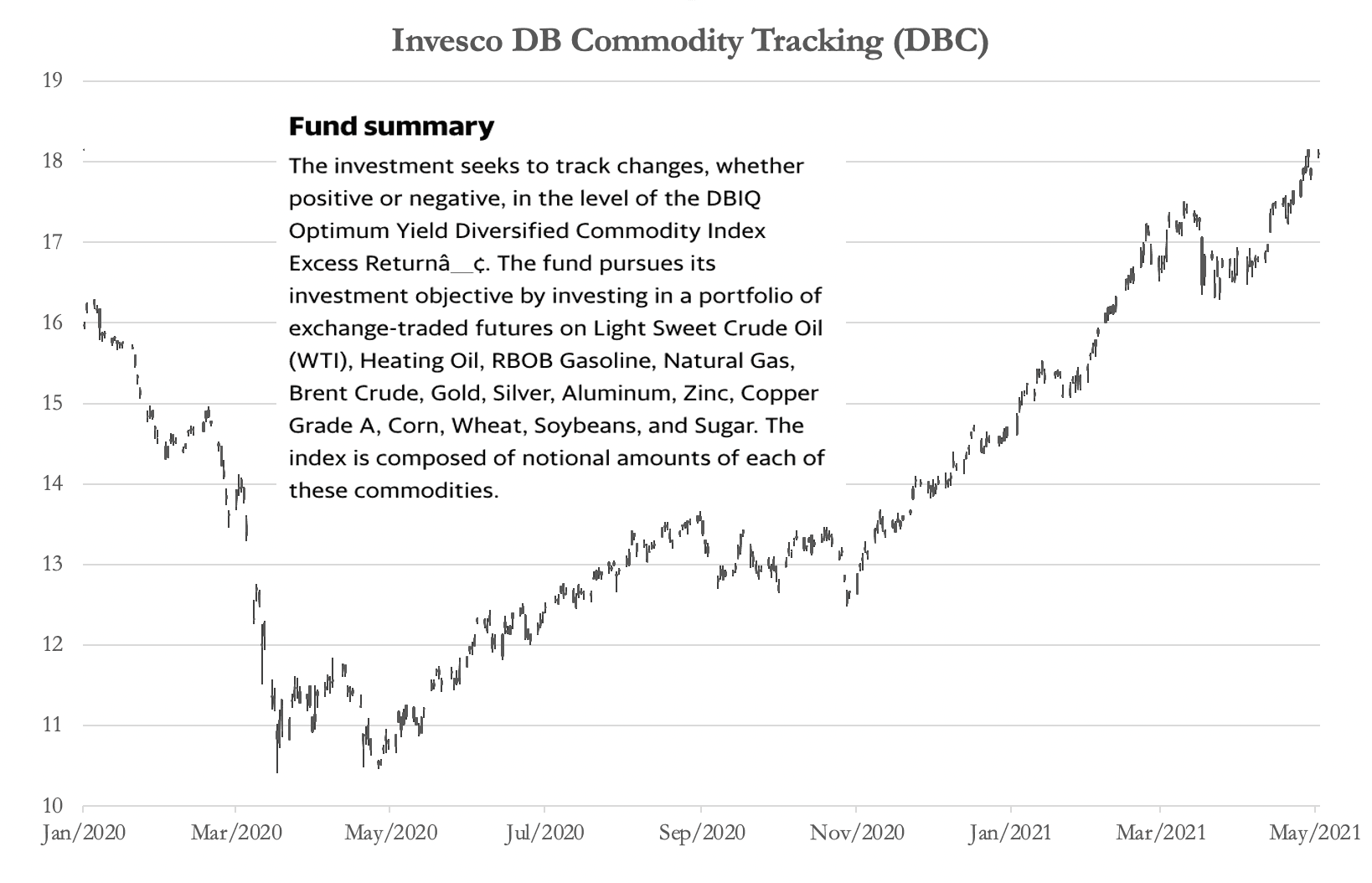

Officially, it’s a case of seeing no evil. But already the establishment consensus is testing more bearish ground. Infrastructure investment plans, not just in the US, but supporting green agendas everywhere are expected to drive oil and copper prices higher, along with a raft of other commodities. As well as state-induced infrastructure spending, in anticipation of strong post-pandemic demand manufacturers are bidding up commodity and raw material prices as well as the cost of the logistics to deliver them. Key industries, particularly agriculture, are suffering acute labour shortages. In many cases, skilled workers are not available. Even the most irresponsibly inflationist economists and commentators are beginning to point out that interest rates will probably have to rise because prices risk spinning out of control.

Fuelling it all is the expansion of base money by central banks. The St Louis Fed’s FRED chart below showing the Fed’s monetary base illustrates the point and is a proxy for the global picture, because the dollar is the reserve currency and the pricing medium for all commodities.

The bond yield on 10-year US Treasuries has already more than doubled over the last year. It is in the nature of market cycles for equity and other financial assets to continue to rise in value during an initial increase in bond yields. It is the second increase that can be expected to turn bullish optimism about the economic outlook into the beginning of a bear market. Financial markets, already dislocated from fundamental realities, appear to be acutely vulnerable to such a change in sentiment.

This article points out that equity markets are driven more by money flows rather than perceived economic prospects. Bank credit for industry is contracting, commodity prices are soaring, and supply chains remain disrupted. Fuelled by earlier expansions of money supply and further expansions to come, the world faces a far larger increase in price inflation than currently contemplated, and therefore far higher interest rates, threatening to destabilise both financial markets and fiat currencies.

Introduction

There is a rustling in the undergrowth, disturbing the sylvan setting where we complacently enjoy the dappled sunlight, innocently unaware of the prowling bear. The bear heralds another rise in bond yields as we grapple with the inflationary consequences of recent and current events.Public participation in equity markets is at an all-time high, not just through direct holdings — amateurish speculation is rife — but through passive index tracking funds and the like. With respect to these, the underlying assumption financial advisors make and tell their innocent clients is that trackers are risk free, because exposure to individual corporate failures is so diluted as to be immaterial. And over time, markets always rise, captured by investing in these funds. But this is deception, ignoring market cycles and systemic risks. Ignorance of the inevitable cyclical switch from greed for profits to fear of loss that defines the divide between bull and bear markets invalidates the permabulls’ advice.

Without doubt, the prowling bear in our so far untroubled scene is bond yields. Unnoticed, they have begun to rise as shown in the chart heading this article. With increasing urgency, it is time to consider the effect on market relationships. Over many investing cycles it has been observed that bond prices conventionally top out before equities. It is one of the most reliable warning signs, which, despite its track record is routinely dismissed by wishful thinkers until it is too late.

Instead, it is a commonplace to argue that prospects for corporate profits have improved at this stage of the economic cycle because of the growing certainty of a better economic outlook. And now that this time the civilised world is emerging from lockdowns, every analyst in the mainstream media delivers this message. For them, the rise in bond yields confirms that improving business conditions are in place to justify yet higher equity prices. But it is all a cycle, having little to do with economic prospects.

Today, we see that the relationship between declining bond prices and rising equities, and all the sentiment and commentary around them, are as we should expect.. But beware the bear lurking in the woods. It’s the second rise in bond yields that often slays the equity bull. I vividly recall meeting an industrialist the autumn of 1972, who told me that his business was the best it ever had been. He then paraded his ignorance of financial matters by telling me that it was wholly irresponsible for the London Stock Exchange to permit the FT 30 share index to have halved in the previous fifteen months. Following that conversation, the FT 30 halved again after interest rates were jacked up in October 1973, creating the infamous secondary banking crisis and losing 70% from its peak in May 1972 by January 1975. And the last I heard of the unfortunate industrialist his business had gone bust and he had committed suicide.

It is a mistake to take opinions or evidence of economic conditions as the principal reason to invest in equities. It is more important to follow the money, specifically the cycle of bank credit. While amateur investors are buying into equity market tops, bankers begin to see that the early signs of rising interest rates are disrupting business plans and will lead inevitably to corporate failures. This comes at a time when their own balance sheets are most highly leveraged. With this credit cycle, there are some additional features specific to it. Even though the ending of pandemic restrictions is expected to lead to a substantial recovery in economic activity, these extra features are extreme, and the bear case is therefore strong.

Banks have begun to withdraw credit from non-financial sector borrowers, meaning they will lack the finance to process and deliver goods to meet increasing demand. Banks are also over-leveraged as they usually are at this stage of the credit cycle, but they have never been more so than they are this time around. The transition from banking greed to banking fear always leads to a substantial cut in bank lending, with the potential outcome of banks being forced to liquidate collateral into falling markets. Unthinkable? It would have happened every credit cycle without central banks taking action to avoid it — which they have achieved every time so far since the 1930s. And consider interest rates, which are already at zero, and negative in euros, yen and Swiss francs. Where can they go to rescue a global economy failing for lack of bank credit?

The stand-out indicator is always bond yields. The chart at the head of this article strongly suggests to us that after the current pause they are heading higher — probably much higher. This article explains why, and what will be the consequences for financial markets. And why, despite higher bond yields, the purchasing power of fiat currencies have not only started to fall at an accelerating pace but will almost certainly continue to do so.

Why bond yields are rising

The 10-year US Treasury yield fell to only 0.48% in March 2020, when deflationary fears were mounting. The S&P 500 index had fallen by 32% in just five weeks as China’s covid crisis was followed by the prospect of other jurisdictions going into pandemic lockdowns. Commodity prices were collapsing. The Fed then did what it always does in these conditions. It cut interest rates to the minimum possible (zero this time) and it flooded markets with money ($120bn in QE every month) along with some other market fixes to cap corporate bond yields from rising to reflect lending risks.Immediately, almost everything began to recover with the exception of bond prices. But the initial increase in their yields can be justified on the basis that they were previously depressed by fears of deflation ahead of the spreading pandemic, and that with the worst fears of deflation had now passed a state of normality had returned. In the year following, equity markets recovered fully and have gone on to new highs. Commodity prices are now rising strongly, which so far is believed by market optimists to indicate recovering demand and therefore confirmation of economic recovery. Having some time ago changed the inflation target from 2% to an average of 2% over time, only last week the Fed saw no reason to expect a rise in price inflation to be more than a temporary phenomenon.

Officially, it’s a case of seeing no evil. But already the establishment consensus is testing more bearish ground. Infrastructure investment plans, not just in the US, but supporting green agendas everywhere are expected to drive oil and copper prices higher, along with a raft of other commodities. As well as state-induced infrastructure spending, in anticipation of strong post-pandemic demand manufacturers are bidding up commodity and raw material prices as well as the cost of the logistics to deliver them. Key industries, particularly agriculture, are suffering acute labour shortages. In many cases, skilled workers are not available. Even the most irresponsibly inflationist economists and commentators are beginning to point out that interest rates will probably have to rise because prices risk spinning out of control.

Fuelling it all is the expansion of base money by central banks. The St Louis Fed’s FRED chart below showing the Fed’s monetary base illustrates the point and is a proxy for the global picture, because the dollar is the reserve currency and the pricing medium for all commodities.

From the beginning of March 2020, which was the month the Fed announced virtually unlimited monetary expansion, base money has grown by 69%. It is this rapid growth in central bank money which is undoubtedly behind rising commodity prices, or put more accurately, is why the purchasing power of the dollar in international markets is falling.

When the outlook for the purchasing power of a fiat currency falls, all holders expect compensation in the form of higher interest rates. Partly, it is due to time preference — the fact that an owner of the currency has parted with the use of it for a period of time. And partly it is due to the expectation that when returned, the currency will buy less than it does today. Official forecasts of the CPI state that the dollar’s purchasing power will probably sink to 97.5 cents on the dollar, then the yield on the ten-year UST should be at least 2.56% (2.5%/0.97), otherwise new buyers face immediate losses. The official expectation that the rise in the rate of price inflation will be temporary is immaterial to an investment decision today, because the yield can be expected to evolve over time in the light of events.

This is before adding something to the yield for time preference (admittedly minimal in a freely traded bond), plus something for currency risk relative to an investor’s base currency and plus something for creditor risk. Stripped of these other considerations, on the basis of expected inflation alone a current yield of 1.61 appears to be far too low, and a yield target of at minimum of 2.5% appears more appropriate.

Apologists for the dollar argue that the deeper the crisis, the greater is the desire for dollars. It is true that many holders of dollars accord to it a safe-haven status compared with their own currencies. But that is fundamentally an argument that applies to short-term liquidity more than to any other reason to hold dollars, with the exception, perhaps, of holders whose base currencies are minor and systemically weak. But with the dollar’s trade weighted index sinking itself since March 2020 that is not true of the wider currency universe. With the dollar falling against other currencies and non-Governmental foreign ownership of dollar financial assets over-owned to the point which exceeds US GDP, the safe haven argument for the dollar lacks credibility.

The Fed’s apparently optimistic assumptions about the dollar’s stability appear to play to its own vested interest. Naturally, there is a reluctance to admit to a greater erosion of its prospective exchange rate, which consequently might require a change in interest rate policy. But commodity prices are soaring, and as locked-up consumer and business spending is unleashed, the supply of goods will be limited, partly due to a lack of domestic capital resources due to the commercial banks restricting bank credit, and partly due to continuing chaos in the supply chains. Instead of a price inflation rate at 2.5%, we should look for a significantly higher rate with which to discount the future purchasing power of the dollar.

It is likely to be only a brief matter of time before holders of all fiat currencies address this issue soberly without the bullish sentiment currently pervading in markets. However, the advanced signs of one final fling for financial assets were visible to those who understand money in March 2020, when the Fed cut its funds rate to zero and announced QE of $120bn per month. It has been a theme of these articles ever since.

Since then, commodities have soared in price along with other inflation hedges, such as cryptocurrencies, equities and residential property. Other than the purchasing power of currencies, the fallers are fixed interest bonds as their yields have risen.

The first class of dollar holder to be affected is foreigners. Some of them are businesses which don’t really need dollars, given they will end up holding even more by exporting to the US. They must be learning it is better to have stockpiled the raw materials for production.

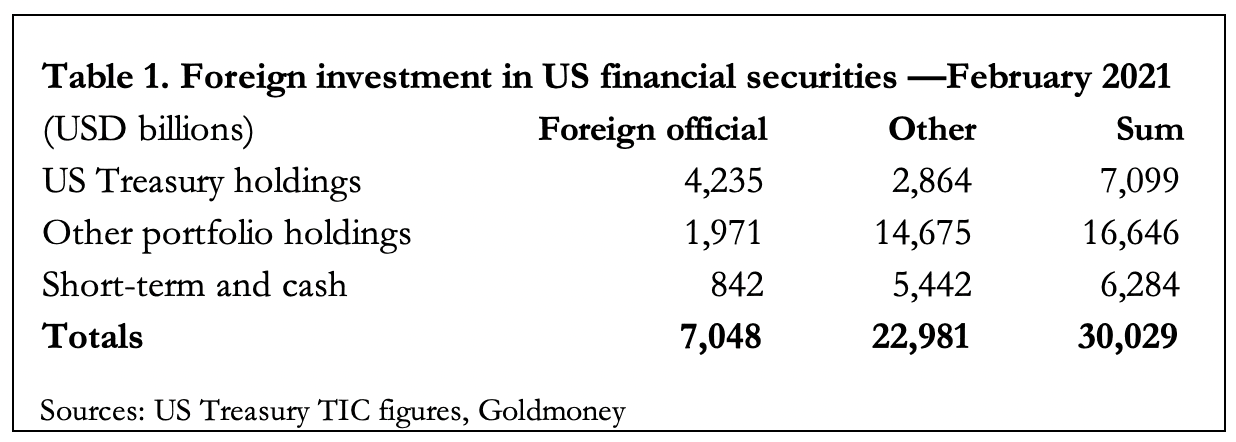

Some of them are investors based in other currencies, diversifying their portfolios, ephemeral holders of financial assets who will sell them when bond yields rise further. This liquidation potential in foreign hands is a major consideration because of the enormous quantities involved. The splits between official and private sector holders (Others) are shown in Table 1 below.

When the outlook for the purchasing power of a fiat currency falls, all holders expect compensation in the form of higher interest rates. Partly, it is due to time preference — the fact that an owner of the currency has parted with the use of it for a period of time. And partly it is due to the expectation that when returned, the currency will buy less than it does today. Official forecasts of the CPI state that the dollar’s purchasing power will probably sink to 97.5 cents on the dollar, then the yield on the ten-year UST should be at least 2.56% (2.5%/0.97), otherwise new buyers face immediate losses. The official expectation that the rise in the rate of price inflation will be temporary is immaterial to an investment decision today, because the yield can be expected to evolve over time in the light of events.

This is before adding something to the yield for time preference (admittedly minimal in a freely traded bond), plus something for currency risk relative to an investor’s base currency and plus something for creditor risk. Stripped of these other considerations, on the basis of expected inflation alone a current yield of 1.61 appears to be far too low, and a yield target of at minimum of 2.5% appears more appropriate.

Apologists for the dollar argue that the deeper the crisis, the greater is the desire for dollars. It is true that many holders of dollars accord to it a safe-haven status compared with their own currencies. But that is fundamentally an argument that applies to short-term liquidity more than to any other reason to hold dollars, with the exception, perhaps, of holders whose base currencies are minor and systemically weak. But with the dollar’s trade weighted index sinking itself since March 2020 that is not true of the wider currency universe. With the dollar falling against other currencies and non-Governmental foreign ownership of dollar financial assets over-owned to the point which exceeds US GDP, the safe haven argument for the dollar lacks credibility.

The Fed’s apparently optimistic assumptions about the dollar’s stability appear to play to its own vested interest. Naturally, there is a reluctance to admit to a greater erosion of its prospective exchange rate, which consequently might require a change in interest rate policy. But commodity prices are soaring, and as locked-up consumer and business spending is unleashed, the supply of goods will be limited, partly due to a lack of domestic capital resources due to the commercial banks restricting bank credit, and partly due to continuing chaos in the supply chains. Instead of a price inflation rate at 2.5%, we should look for a significantly higher rate with which to discount the future purchasing power of the dollar.

It is likely to be only a brief matter of time before holders of all fiat currencies address this issue soberly without the bullish sentiment currently pervading in markets. However, the advanced signs of one final fling for financial assets were visible to those who understand money in March 2020, when the Fed cut its funds rate to zero and announced QE of $120bn per month. It has been a theme of these articles ever since.

Since then, commodities have soared in price along with other inflation hedges, such as cryptocurrencies, equities and residential property. Other than the purchasing power of currencies, the fallers are fixed interest bonds as their yields have risen.

The first class of dollar holder to be affected is foreigners. Some of them are businesses which don’t really need dollars, given they will end up holding even more by exporting to the US. They must be learning it is better to have stockpiled the raw materials for production.

Some of them are investors based in other currencies, diversifying their portfolios, ephemeral holders of financial assets who will sell them when bond yields rise further. This liquidation potential in foreign hands is a major consideration because of the enormous quantities involved. The splits between official and private sector holders (Others) are shown in Table 1 below.

It should be noted that American holdings of foreign currencies are minimal becaause lending to foreigners is overwhelmingly in dollars instead of foreign currencies, and America’s massive trade deficit ensures that while dollars accumulate in foreign hands, foreign currencies do not accumulate in American hands. This makes the figures in Table 1 as a dollar crisis waiting to happen all too real.

Once non-official holders awaken to what is happening to their dollars and to the consequences of increasing bond yields for the wider classes of financial assets, they will almost certainly reduce their holdings of nearly $23 trillion. Holdings of all dollar-denominated financial assets will be at risk, and where they go, financial assets denominated in all other currencies naturally follow. We can expect the dollar to continue its fall against other currencies as well, in part driven by President Biden’s highly inflationary spending plans. Irrespective of the domestic economic conditions, the Fed will then have no practical alternative to raising interest rates to stabilise the dollar against other currencies. But we can be sure the Fed will be extremely reluctant to do so.

As the much-vaunted post-lockdown consumer spending is unleashed, the lack of available production supply together with supply chain chaos can only result in consumer prices rising significantly above the Fed’s average target of 2%. Not only will this naturally lead to higher bond yields, but the valuation basis for equity markets will shift, undermining prices. Even if the Fed tries to offset it by increasing QE to feed more cash into bonds and equities, it will be impossible to offset the valuation effect. Equities will almost certainly succumb to an interest rate shock. At the same time, the increase in bond yields will undermine government finances. The prospect of increasing losses on portfolio investments will inevitably lead to the foreign liquidation described above, causing a weaker dollar and yet higher bond yields.

In these conditions the Fed will be trapped. It cannot let bond and equity prices slide and risk commercial banks accelerating the contraction of bank credit, leading inexorably to the liquidation of loan collateral. Investment sentiment would turn deeply negative. Nor can it stand back and let markets sort themselves out, because of the record levels of corporate and other debt which would become impossible to refinance. Nor can it just print money in order to rescue everything, because the dollar will be further undermined. That leaves it with only one alternative left to pursue, albeit with the greatest reluctance. And that is to raise interest rates — substantially.

Neo-Keynesians, who appear to subscribe to the belief that interest is usuary and savers must be denied returns for the benefit of everyone else, are embedded in central banks and are certain to denounce this attempt at a remedy. But the experience of the 1970s confirms that central banks will raise rates, too little too late, before eventually deciding to kill market expectations of higher interest rates by pre-empting them. Famously, this is what Paul Volcker did in 1979-81. What is less remembered is that despite prime rates hitting 20%, money supply growth continued, so that the interest cost was covered by inflationary means. This is illustrated in the chart below.

From this earlier precedent, we can conclude that in the choice between ceasing to print money and raising interest rates, the Fed will raise interest rates. This adds to the growth of money supply, as can be detected by the increased rate of climb from 1979 onwards. But what would be the effect of such a policy today?

In the 1970s, the build-up of domestic debt beyond that required to genuinely finance production had yet to occur, and the financialisation of the US economy did not happen until the mid-1980s. The increase in debt was mainly sovereign as US banks recycled oil dollars to Latin America. The only significant domestic casualty from high interest rates was the Savings & Loan industry.

Today, the US and other economies are loaded up with debt, much of which is unproductive. A sharp rise in interest rates to contain price inflation would drive the world’s economy into an humungous debt-induced slump. And while that is exactly what is needed to clear out all the zombie deadwood, it is not within the Fed’s remit to take such action. Furthermore, with government borrowing already out of control, the US Government would be forced to curtail its spending dramatically at a time of rapidly escalating welfare obligations.

But we are previewing the end of the road, describing events which logically procede from the dangers before us today. But for now, the consequences of rising bond yields are that they will bring a rapid shift from overtly bullish assumptions to a more considered bearish outlook, bringing with it a wholly different perspective. Instead of bad and inflationary policies being tolerated or even demanded by investors, their thinking turns on a dime to a fear of anything and everything. Under bearish circumstances, every turn of the central management of economic outcomes only makes things worse, when before it appeared to resolve them. Greenspan and the Fed chairmen who followed him were correct about the psychology of improving markets, while they kept quiet about the negative psychology of bear markets. Suddenly, we will find that Charon is waiting to ferry the bodies of the bulls over the river Styx.

Such is the violence of market imbalances that when they are unleashed from the Fed’s control, not only will financial markets face rapid value destruction, but fiat currencies will also be undermined by the need to accelerate the pace of monetary inflation. The emphasis for inflationary policies will shift from financing governments by debauching the money to debauching the money in order to rescue the wider economy. The Fed and its sister central banks will seek to supplement contracting bank credit, make capital freely available to businesses which would otherwise collapse, continue with helicopter drops of money to consumers, and compensate for supply chain disruption. The policy planners are likely to be so confused and the task so enormous that they will end up robbing Peter to pay… who else but Peter himself.

The relevant precedent for this madness comes from 1720, when John Law in France, who among other things was appointed Controller General of Finance, printed unbacked livres to inflate and then support the collapsing Mississippi bubble. His venture lived on to fight Clive in India, but the livre became worthless within seven months. Today, some contemporary corporations will survive, as did Law’s Mississippi venture, but by tying the bubble to the currency, the currency failed completely and is almost certain to do so again today.

There is a common misconception that does not accord with the facts: that higher interest rates are bad for the gold price. It is assumed by those promoting this nonsense that gold does not have an interest rate and is therefore at a disadvantage compared with fiat money. This is only true of both physical gold and fiat cash to hand, when neither folding notes nor gold pay interest. But both can be loaned and leased to borrowers for interest. It’s just that the interest on ephemeral fiat tends to be higher than on physical gold, because gold is the more stable form of money with no issuer risk.

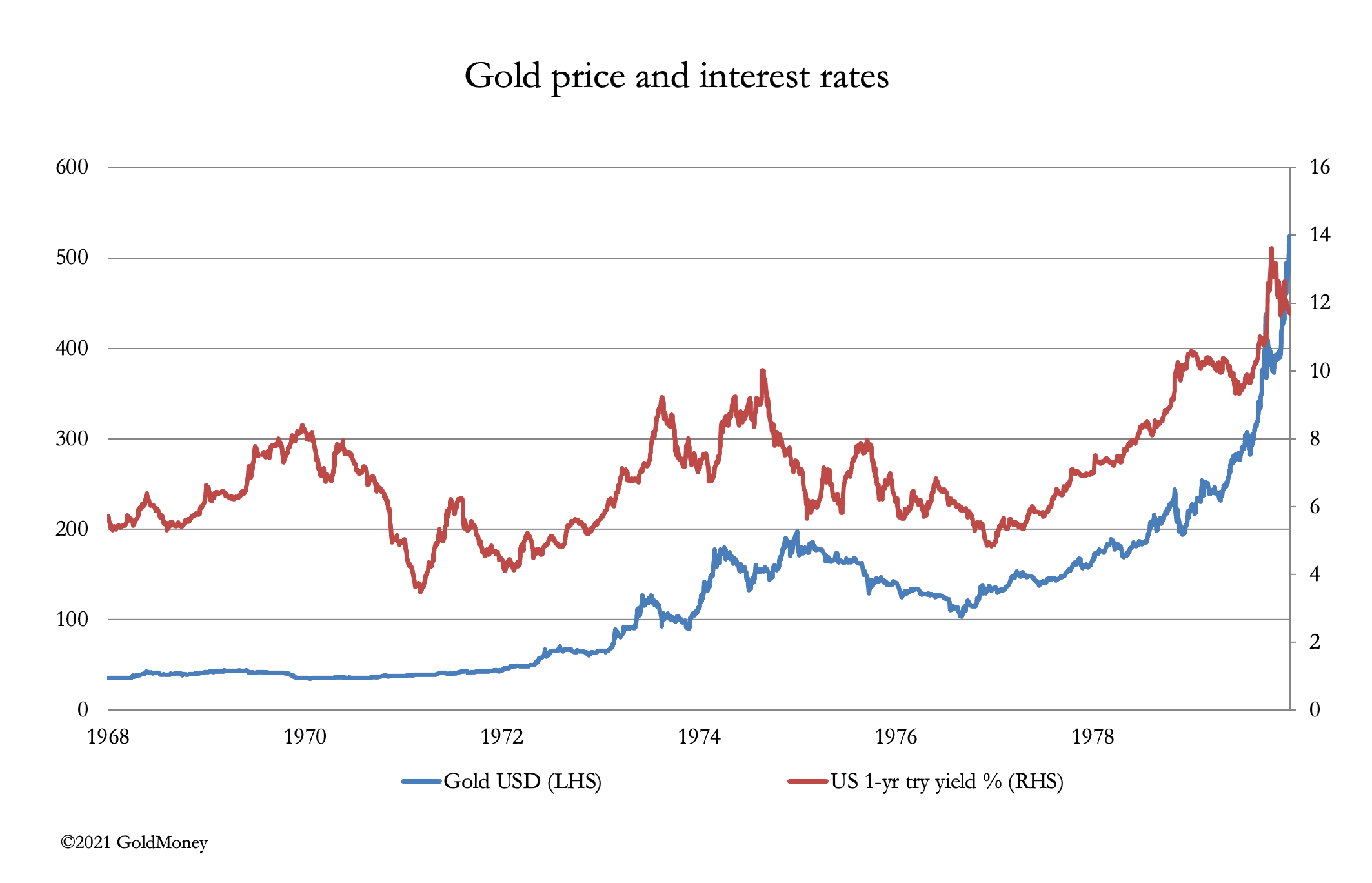

That rising interest rates on fiat currencies are no deterrent to a rising gold price is confirmed in the chart below, which shows how these relationships evolved in the 1970s.

Not only did the decade commence with the yield on the 1-year US Treasury bond at less than six per cent, ending at more than double that, but the gold price rose from $35 to $524 by the end of the decade. Furthermore, the chart shows that from 1972 onwards, gold tended to rise with the yield on the bond and fall with it, defying those who fail to grasp the true relationship.

All this assumes that the collapse of fiat currencies’ purchasing power will take some time. But the truth of the matter is we do not know either the timing or how long it will take. It is unlikely to echo the great European inflations of the 1920s, because to a large degree commerce subsisted on the alternative of gold-backed dollars, instead of local currencies. Today, the collapse of the dollar will mean there is unlikely to be any alternative currency available, because they are all tied to the dollar.

A collapse of financial asset values taking the currencies down with them appears to be more in common with a repetition of John Law’s bubble and subsequent collapse, which incidentally was a forerunner of Keynesianism in action. But a fiat currency going to zero today could take less time, given instantaneous modern communications. In that event, anyone who does not plan to get hold of some physical gold and silver with a high degree of urgency could end up sinking with nothing but valueless fiat currencies.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.

Once non-official holders awaken to what is happening to their dollars and to the consequences of increasing bond yields for the wider classes of financial assets, they will almost certainly reduce their holdings of nearly $23 trillion. Holdings of all dollar-denominated financial assets will be at risk, and where they go, financial assets denominated in all other currencies naturally follow. We can expect the dollar to continue its fall against other currencies as well, in part driven by President Biden’s highly inflationary spending plans. Irrespective of the domestic economic conditions, the Fed will then have no practical alternative to raising interest rates to stabilise the dollar against other currencies. But we can be sure the Fed will be extremely reluctant to do so.

The latent primacy of markets over monetary policy

Without doubt, there were urgent reasons for the Fed to rescue stocks and other markets in March 2020. For several decades successive Fed chairmen from Alan Greenspan onwards have openly admitted that a rising stock market is central to monetary policy, because of its roles for wealth creation and the enhancement of economic confidence. But the market rescue fourteen months ago also confirmed, if confirmation was needed, that the Fed would always address any financial and economic crisis by inflationary means. This has not yet led to the inflationary crisis that will eventually occur.As the much-vaunted post-lockdown consumer spending is unleashed, the lack of available production supply together with supply chain chaos can only result in consumer prices rising significantly above the Fed’s average target of 2%. Not only will this naturally lead to higher bond yields, but the valuation basis for equity markets will shift, undermining prices. Even if the Fed tries to offset it by increasing QE to feed more cash into bonds and equities, it will be impossible to offset the valuation effect. Equities will almost certainly succumb to an interest rate shock. At the same time, the increase in bond yields will undermine government finances. The prospect of increasing losses on portfolio investments will inevitably lead to the foreign liquidation described above, causing a weaker dollar and yet higher bond yields.

In these conditions the Fed will be trapped. It cannot let bond and equity prices slide and risk commercial banks accelerating the contraction of bank credit, leading inexorably to the liquidation of loan collateral. Investment sentiment would turn deeply negative. Nor can it stand back and let markets sort themselves out, because of the record levels of corporate and other debt which would become impossible to refinance. Nor can it just print money in order to rescue everything, because the dollar will be further undermined. That leaves it with only one alternative left to pursue, albeit with the greatest reluctance. And that is to raise interest rates — substantially.

Neo-Keynesians, who appear to subscribe to the belief that interest is usuary and savers must be denied returns for the benefit of everyone else, are embedded in central banks and are certain to denounce this attempt at a remedy. But the experience of the 1970s confirms that central banks will raise rates, too little too late, before eventually deciding to kill market expectations of higher interest rates by pre-empting them. Famously, this is what Paul Volcker did in 1979-81. What is less remembered is that despite prime rates hitting 20%, money supply growth continued, so that the interest cost was covered by inflationary means. This is illustrated in the chart below.

From this earlier precedent, we can conclude that in the choice between ceasing to print money and raising interest rates, the Fed will raise interest rates. This adds to the growth of money supply, as can be detected by the increased rate of climb from 1979 onwards. But what would be the effect of such a policy today?

In the 1970s, the build-up of domestic debt beyond that required to genuinely finance production had yet to occur, and the financialisation of the US economy did not happen until the mid-1980s. The increase in debt was mainly sovereign as US banks recycled oil dollars to Latin America. The only significant domestic casualty from high interest rates was the Savings & Loan industry.

Today, the US and other economies are loaded up with debt, much of which is unproductive. A sharp rise in interest rates to contain price inflation would drive the world’s economy into an humungous debt-induced slump. And while that is exactly what is needed to clear out all the zombie deadwood, it is not within the Fed’s remit to take such action. Furthermore, with government borrowing already out of control, the US Government would be forced to curtail its spending dramatically at a time of rapidly escalating welfare obligations.

But we are previewing the end of the road, describing events which logically procede from the dangers before us today. But for now, the consequences of rising bond yields are that they will bring a rapid shift from overtly bullish assumptions to a more considered bearish outlook, bringing with it a wholly different perspective. Instead of bad and inflationary policies being tolerated or even demanded by investors, their thinking turns on a dime to a fear of anything and everything. Under bearish circumstances, every turn of the central management of economic outcomes only makes things worse, when before it appeared to resolve them. Greenspan and the Fed chairmen who followed him were correct about the psychology of improving markets, while they kept quiet about the negative psychology of bear markets. Suddenly, we will find that Charon is waiting to ferry the bodies of the bulls over the river Styx.

Such is the violence of market imbalances that when they are unleashed from the Fed’s control, not only will financial markets face rapid value destruction, but fiat currencies will also be undermined by the need to accelerate the pace of monetary inflation. The emphasis for inflationary policies will shift from financing governments by debauching the money to debauching the money in order to rescue the wider economy. The Fed and its sister central banks will seek to supplement contracting bank credit, make capital freely available to businesses which would otherwise collapse, continue with helicopter drops of money to consumers, and compensate for supply chain disruption. The policy planners are likely to be so confused and the task so enormous that they will end up robbing Peter to pay… who else but Peter himself.

The relevant precedent for this madness comes from 1720, when John Law in France, who among other things was appointed Controller General of Finance, printed unbacked livres to inflate and then support the collapsing Mississippi bubble. His venture lived on to fight Clive in India, but the livre became worthless within seven months. Today, some contemporary corporations will survive, as did Law’s Mississippi venture, but by tying the bubble to the currency, the currency failed completely and is almost certain to do so again today.

Gold and rising interest rates

As a consequence of current events, the failure of fiat currencies is increasingly assured. Unlike the runaway inflation in the 1970s which followed the ending of the Bretton Woods Agreement, debt levels are now so high and state intervention in markets so great that hiking interest rates in the manner deployed by Paul Volcker would simply prick the everything bubble. Debt defaults would be overwhelming. Nevertheless, as the purchasing power of fiat currencies continues to slide, higher and higher interest rates become inevitable as markets try to discount yet further declines towards their ultimate valuelessness.There is a common misconception that does not accord with the facts: that higher interest rates are bad for the gold price. It is assumed by those promoting this nonsense that gold does not have an interest rate and is therefore at a disadvantage compared with fiat money. This is only true of both physical gold and fiat cash to hand, when neither folding notes nor gold pay interest. But both can be loaned and leased to borrowers for interest. It’s just that the interest on ephemeral fiat tends to be higher than on physical gold, because gold is the more stable form of money with no issuer risk.

That rising interest rates on fiat currencies are no deterrent to a rising gold price is confirmed in the chart below, which shows how these relationships evolved in the 1970s.

Not only did the decade commence with the yield on the 1-year US Treasury bond at less than six per cent, ending at more than double that, but the gold price rose from $35 to $524 by the end of the decade. Furthermore, the chart shows that from 1972 onwards, gold tended to rise with the yield on the bond and fall with it, defying those who fail to grasp the true relationship.

All this assumes that the collapse of fiat currencies’ purchasing power will take some time. But the truth of the matter is we do not know either the timing or how long it will take. It is unlikely to echo the great European inflations of the 1920s, because to a large degree commerce subsisted on the alternative of gold-backed dollars, instead of local currencies. Today, the collapse of the dollar will mean there is unlikely to be any alternative currency available, because they are all tied to the dollar.

A collapse of financial asset values taking the currencies down with them appears to be more in common with a repetition of John Law’s bubble and subsequent collapse, which incidentally was a forerunner of Keynesianism in action. But a fiat currency going to zero today could take less time, given instantaneous modern communications. In that event, anyone who does not plan to get hold of some physical gold and silver with a high degree of urgency could end up sinking with nothing but valueless fiat currencies.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.