Why gold is always money

May 4, 2023·Alasdair MacleodThat America faces a severe banking crisis has become plain to see, but the authorities’ response less so. Almost certainly, the crisis has much further to go in America, spreading to other jurisdictions. We can only hope that central banks will protect all depositors, but that is far from certain in this early stage.

These febrile conditions are made infinitely more difficult by the contraction of bank credit. The cyclical nature of bank credit means that the shortage of credit will intensify, driving up borrowing costs even in the face of a recession. Interest rates are no longer under the control of central banks, though market participants have yet to realise it.

It has important implications for the valuation of credit. In order to understand the consequences, this article draws out the legal and practical distinctions between money, defined as gold and silver but principally gold, and credit in the form of banknotes and bank deposits.

The value of credit is a matter of the confidence in it. You may think that your dollars, euros, or pounds are money, but you would be wrong. They are credit. The cost of being wrong will not be just to see your bank deposits threatened systemically, but potentially the entire currency system undermined by loss of faith in it.

To properly understand these dangers, this article defines and describes the differences between credit and money. It is credit which is threatened with collapse. Only true money, which very few westerners possess will survive.

Introduction

It is commonly believed today that money is the currency issued by central banks as bank notes. Indeed, all credit is often described as such, and that gold’s role as money is obsolete. Furthermore, the establishment view is that coinage divided into fractions of bank note units need no longer be made of silver and copper, since they take their status from the bank notes to which they refer.

These modern notions of money are on the verge of their ultimate test, since this incorrect definition for many extends to the entirety of circulating media which have suffered substantial debasements in the last year. It was triggered by an excess of government spending over revenue income and a complete disregard for confidence in currency values, particularly for the dollar but also for the other major western currencies.

This test is not confined to the loss of confidence in these currencies by their domestic users. Their validity as money, as opposed to a form of unhinged currency, is in the early stages of being challenged by foreign interests, particularly by Russia, China, and now by many other nations either hostile to western interests or seeking to defend themselves from the consequences of their increasingly probable collapse. For collapse is what they face — an entire over-leveraged western banking system forced to adjust to rising interest rates. Banks are contracting their balance sheets forcing interest rates even higher, and consequently a collapse of financial asset values is in prospect.

Furthermore, major central banks themselves, led by the Fed, the ECB, the Bank of England, and the Bank of Japan have created losses for themselves and their governments amounting to many multiples of their equity. The only exception is the Bank of England which has an explicit guarantee from the UK Treasury to cover all its losses, so far amounting to about £200 million compared with its paid-up equity of £15 million.

We do not yet have details of how China and Russia intend to respond to the increasingly likely collapse of the western alliance’s highly financialised economies. We do know that Asian economies are radically different, based on energy, commodities, and production of goods. In this respect they are relatively stable at a time of financial crisis. But their plans to ensure that their currencies don’t get entangled in a western currency calamity are yet to be revealed.

We do know from Sergey Glazyev, Putin’s Minister of Integration and Macroeconomics charged with designing a new trade settlement currency for the Eurasian Economic Union, that he plans to incorporate gold backing for it. And from his article on 27 December in Vedomosti (a Moscow-based business magazine), we know that he envisages the rouble being backed by gold as well.

That, in a nutshell, is the challenge faced by the West’s currencies. Whether they are truly money having replaced gold is about to be tested by a return of gold into the monetary systems of Russia and central Asia, and probably of China as well. Others might follow.

This article is intended to guide its readers towards an understanding of the issues involved. But it is not just what constitutes the ultimate money, be it dollars or gold. It is about disregarding statist propaganda and understanding established legal definitions and distinctions. And particularly, it is about understanding the difference between money and credit.

The overriding importance of credit

“It is somewhat surprising that in this great mercantile country there is not a single treatise in the English language which contains an exposition of the juridical and mathematical principles of the colossal system of credit, together with the application in practical commerce.”

With the exception of his own treatise on the subject, this quotation from Henry Dunning Macleod’s Preface to his Theory of Credit is as true today as it was in 1889 when it was published.

He pointed out that the Romans invented banking, cheques, and bills of exchange and defined the legal principals of credit. These were incorporated in the Pandects of Justinian, which were the code for the Western Roman Empire, and in the Basilica, the code of the Eastern Empire. And these two legal digests have been the mercantile law of Europe ever since and are still reflected in every European treatise on jurisprudence.

But for the avoidance of doubt, we must start our subject by clarifying it with some important definitions:

- Money. For the purposes of this article, we restrict the definition of money to credit with no counterparty risk. In accordance with the principals of the division of labour, the possession of money is unspent credit, the result of earnings and profits gained through production. As the highest form of credit, its superiority over credit with counterparty risk has always been unquestioned, confirmed in law, and differentiated from other forms of credit. For convenience it is standardised into recognised coin, consisting of standardised weights of physical gold, silver, and copper. Only these can be said to be true money.

- Credit. Credit is anything of no direct use, but which is taken in exchange for something else in the belief or confidence that we have the right to exchange it away again. It is therefore the right or property of demanding something else when we require it.

- Currency. The term “currency” has become synonymous with the phrase “circulating medium”. Originally, the term arose from money being described as current, so we had the “currency of money”. Currency has therefore become a general description covering both money and credit used for the buying and selling of goods and services.

- Banknotes. Banknotes are obligations of an issuing bank in circulation. They are not to be confused with money, as is commonly the case today, even by many respected economists.

- Bank deposits. Bank deposits are credit owed by a bank to its depositors. Many depositors incorrectly confuse their bank’s obligation to them with a custodial function, where they own a deposit which the bank is holding for them.

- Bank loans. A bank loan is credit created by a bank in favour of a borrower.

In practice, even under gold standards money was hardly ever used as currency, its use generally being restricted to silver and copper coins for smaller transactions. The primary role of money was always as a backstop to credit, securing credit’s value and ultimately for credit to be paid in money should a creditor so demand when credit is due to be settled.

The evolution of Roman law with respect to money and credit

The origin of Roman Law was the Twelve Tables (or tablets), ratified in 449 BCE and venerated by Romans as their primary legal source. They were superseded by later changes in Roman law, but never abolished. And according to Gaius, of whom more follows, it was at this time that the first Roman coin, the aes made of bronze, was introduced. In its early form it was more a standardised weight than a coin as we know it today, weighing a little under one third of a kilo.

Credit certainly existed before then, though not on a formal basis. Trade has always required credit, because time elapses between the acquisition of materials and their delivery to market. The Phoenicians were trading throughout the Mediterranean, and even beyond, a thousand years before Rome’s Twelve Tables and in addition to bartering would certainly have required credit to do so, because they had no coinage before Roman times. Clearly, the need to fix the value of credit led to demand for its expression in a superior form of credit without counterparty risk — real money.

The Twelve Tables was also at a time of intellectual revolution, being contemporary with the great Greek philosophers — Socrates, Plato, and Aristotle among others. Coincidentally, Confucius was advancing Chinese philosophy only fifty years before.

Roman law took its next evolutionary step when Gaius wrote his Institutiones as well as a commentary on the Twelve Tables in about 161 CE. It provided a template for Justinian’s Institutes (or Pandects) with some of Gaius’s passages even copied verbatim. Gaius’s original manuscript was lost until it was rediscovered at Verona in 1816 by a German scholar.

With respect to credit and banking, fifty years later the rulings of Ulpian and Paulus superseded and improved on Gaius’s by ruling that credit could be transferred for value without the agreement of both originating parties. This meant that debt could be freely sold without the consent or knowledge of the debtor. It was probably on Ulpian’s advice that the emperor Alexander Severus in 224 CE published his Constitution formalising this freedom.

This vital step meant that credit could be incorporated as personal wealth, which we can define simply as comprised of anything which can be valued or sold in a medium of exchange. By the time of Justinian’s Pandects in 553 CE, the legal principal of the transferability of credit was well established and incorporated in them, and also confirmed in the Basilica of the Eastern Empire which followed 339 years later.

Between the Pandects and the Basilica, the principal that money was the highest form of credit from which lesser forms took their cue became firmly established in the two Roman Empires and in their successor nations throughout Europe. The great waves of discovery and colonisation by these nations in more recent centuries spread not only their Christianity, but their laws founded on Roman origins.

For a time, English common law was in a confused position, having inherited its precedents from Gaius, which were current when the Romans left Britain in 410 CE, and before Justinian’s Pandects over a century later. Severus’s Constitution appears to have not been fully adopted.

However, with respect to the transferability of credit and therefore the inclusion of debt as personal wealth, the situation was regularised when conflicts between common law and the Court of Chancery which dealt with matters of equity were abolished in 1875 after enabling legislation was passed in 1873.

Credit is the basis of incorporeal wealth

The definition of wealth is anything which can be exchanged for value, and Roman law evolved to recognise three categories:

- Corporeal wealth, which includes buildings, land, physical commodities, livestock, grains, and gold, and all exchangeable physical items.

- Immeasurable wealth, which includes personal qualities, such as skills, goodwill, patents, and trademarks.

- Incorporeal wealth, which includes abstract rights, such as rights of action, bonds, equity, and debt.

The first two categories should be plain enough. But in the past, there has been some controversy about the treatment of debt. It has been argued that a homeowner, for example, might value his property at a certain figure, but that should be reduced by the mortgage on it to give a net value, the net value being his wealth in the property.

That might seem reasonable enough, but the debt is not due until sometime in the future. Yet the homeowner has the full benefit of the property. For this reason, the law holds that the debt obligation is not to be confused with the debt itself. The debt only comes into existence when payment is due. Therefore, in the case of the homeowner above, he would be correct in ignoring the mortgage debt until payment is due in calculating his wealth.

Every debt obligation is matched by corresponding credit, which as confirmed in Roman law has an exchangeable value. Examples include the ownership of bonds, listed on an exchange or not, credit card debts securitised or not, and mortgages securitised or not. Treasury and commercial bills, bills in trade finance, and equities which are entitlements to an income stream in perpetuity, are all debt obligations with matching and marketable credit.

Therefore, if there is an increase in the quantity of debt, there is an increase in the quantity of wealth because of the increase in credit which is incorporeal wealth. The sustainability of levels of debt are a different matter — that requires the discipline of an ability to repay or refinance when debts are due and will be reflected in the value of the matching credit.

Makeup of a modern monetary system

For exactly nine decades, a process of doing away with the link between inferior classes of credit and legal money, which is gold, has been led by America. By Executive Order 6102, American citizens were forced to surrender all but a small amount of their gold coin, gold bullion, and gold certificates on or before 1 May 1933. That was followed by a devaluation of the dollar against gold the following January. And in July 1944, the Bretton Woods Agreement was signed, restricting encashment of dollars for gold to central banks, the IMF, and the World Bank — organisations created by the same Bretton Woods Agreement. And in August 1971, the Bretton Woods Agreement was suspended by President Nixon, to be formally ended by the Jamaica Accord in 1976.

Consequently, fixed exchange rates against the dollar for other currencies were abandoned, and the dollar became everyone’s reserve currency. To secure the dollar’s position, the US Government commenced an intensive propaganda campaign to persuade both American citizens and foreigners that gold was no longer part of the monetary system and had been superseded by the dollar.

The consequences of ignoring legal and practical precedents are hiding in plain sight. From the rate of exchange whereby dollars could be freely redeemed for gold at $20.67 to the ounce at the time of the Executive Order, the market relationship with gold indicates that the dollar as a currency has lost 99% of its value over that time.

The dollar itself consists of two types of unanchored credit: bank notes and other obligations issued by the Federal Reserve Board, and deposits recorded as commercial bank liabilities. Their ratio is currently about one to eight times, but it is estimated that as much as half the note issue circulates abroad, in which case it is closer to double.

In recent decades, quantitative easing has increased central bank obligations to the commercial banks, reflected in an increase in their reserves. The increase in bank reserves was matched by increased deposit liabilities to the institutions — insurance companies, pension funds, and banks trading for their own books — which have sold government, agency, and other bonds to their relevant central banks.

For a number of reasons, from the increase in the quantity of bank and central bank credit to geopolitical factors, the purchasing power for consumer goods of most western alliance currencies has deteriorated markedly over the last fifteen months. Assuming this established trend continues, they will lose further ground over time against legal money — gold. Clearly, for the situation to stabilise, credit needs to have its golden anchor restored.

Credit needs an anchor in value

As demonstrated by the legal heritage of gold in all significant jurisdictions with law derived from Europe, if credit is anchored to gold then its value becomes stabilised both internationally and domestically. The link must be credible and for durability’s sake should be accessible to all. This was the thinking behind the introduction of the British gold sovereign coin in 1817, an arrangement that secured sterling’s purchasing power until the outbreak of war in 1914. The chart below shows how wholesale prices stabilised, after the suspension of specie convertibility in 1797.

The early years of the nineteenth century commenced with the suspension of specie payments, following the Bank Restriction Act of 1797. The Act was enabled to protect the Bank of England’s dwindling bullion reserves of gold and silver coins following a succession of poor grain harvests and preparations for war against an increasingly belligerent France. The suspension lasted through the Napoleonic wars until the introduction of the sovereign in 1817.

Following war-time inflation and the remedial actions taken, the general level of wholesale prices declined until the early 1820s, when despite a series of banking crises, price fluctuations tended to diminish over time. The reason prices stabilised was due to evolutionary improvements in the commercial banking system. The London banks had established a joint clearing system in 1775, and in 1854 joint stock banks (banks with outside shareholders) joined the system. This was followed by the Bank of England becoming a member in 1864.

Between 1844 (the time of the Bank Charter Act) and 1900, the wholesale index in the chart above was unchanged, having dipped slightly after 1875. It was also remarkably stable. But between 1844 and 1900, the sum of Bank of England banknotes in circulation and commercial bank deposit obligations increased eleven times, and there was a material increase in the quantity of short-term, commercial bills funding foreign trade as well. Monetarist theory would suggest that the expansion of credit on such a scale would undermine the purchasing power of the currency, but plainly it did not.

The evidence is that so long as credit is tied firmly to gold, it will continue to take its value from it. And it will continue to do so until gold stocks in bullion or coin are drained from the note issuing bank to the point where the link is threatened.

It also explains why dollar prices were stable during the Bretton Woods Agreement, even though the connection was tenuous. The point is that given US official gold reserves were substantial, credit markets trusted the arrangement and derived their value from it.

Furthermore, the loss of the tie between gold and the dollar following the Bretton Woods Agreement’s suspension confirms the importance of firmly linking the value of all forms of credit to gold.

The next chart illustrates the point with respect to that most important commodity without which human progress would collapse — in this case the price of WTI oil in both dollars and gold, which is the marker for energy values.

The dollar price of oil was remarkably stable before the early seventies and priced in gold has remained so ever since. But shortly after the end of the Bretton Woods regime, priced in dollars the oil price exploded upwards, and became extremely volatile. Some of that volatility affected the price of oil measured in gold. In January 1974, priced in dollars oil more than doubled, while priced in gold it fell by 21%.

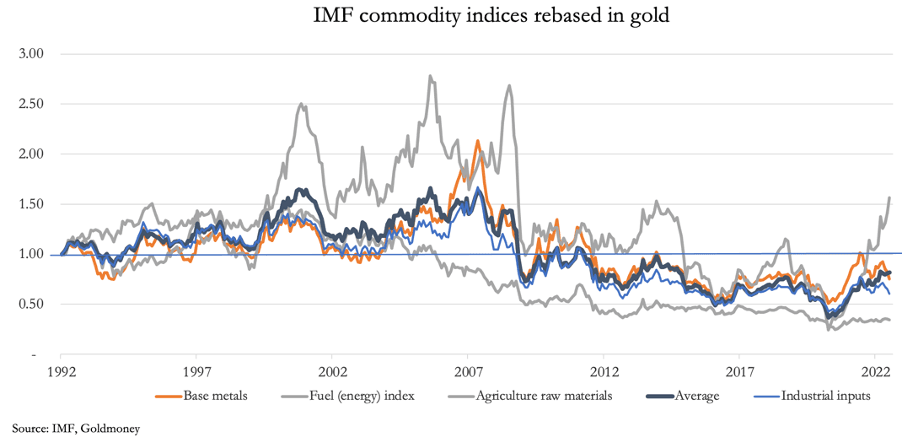

Price analysis misses this vital point, with economists, financiers, and businesses alike believing that the dollar is stable, and it is the oil price which is volatile. While there is some volatility in the oil price, it is actually the dollar which is unstable. The dollar is entirely credit, unanchored to legal money which is gold. This finding is confirmed in the pricing of a wide range of commodities in gold, which is our next chart.

While individual sectors have fluctuated in value over the last three decades, priced in gold they have been considerably less volatile than in fiat currencies. And their average value (the black line) has been remarkably constant. The low point was in early-2020 when futures speculation drove the dollar price of oil briefly into negative territory. But by mid-2022, the average value of these commodity baskets had declined by only 18% from January 1992, when the IMF’s data series began.

It is a fact that major currencies have become completely detached from legal money. The British gold sovereign was exchangeable for a one-pound note before the First World War: today the value of a pound note has reduced to one quarter of one per cent of one sovereign — put conventionally, a sovereign now costs £400.

The next chart shows how the four major currencies have declined relative to gold since the abandonment of Bretton Woods.

Even the mighty yen has lost over 95% of its value. The euro, based on the basket of currencies that contributed to its creation in 2000, has lost 98.7%, and the dollar 98.3%.

The banking crisis and credit contraction

There is a long-established cycle of bank behaviour, whereby bankers progressively become more confident in their lending until they become over-leveraged. They are then extremely vulnerable to a change in lending sentiment from greed for profit to fear of losses. Since the early nineteenth century this cycle of credit expansion and contraction has averaged about ten years. It is worth noting that since the last banking crisis in 2009, fourteen years have elapsed, making this cycle unusually extended.

The next chart indicates how bank balance sheet leverage in the US’s commercial banking system has evolved over the last thirty years.

It is against this background of record balance sheet leverage that US commercial bank credit is now contracting. The increasing financialisation of the US and other western economies coupled with the suppression of interest rates by central banks inflated a financial bubble, which came to an end last year when consumer price inflation forced a change on interest rate policies.

Unusually, the world’s most senior commercial banker, Jamie Dimon of JPMorgan Chase, at a banking conference in New York in June last year warned of an economic hurricane approaching. The implication was that his bank would become more cautious over lending and risk exposure generally. He was signalling his pivot from maximising the bank’s profits through balance sheet leverage to risk containment. And as the chart above shows, the relationship between balance sheet size and Tier 1 equity for the entire US banking industry topped out at that time.

Dimon’s warning would have been echoed in the lending policies of the other major banks. Together, bankers act as a cohort, and his hurricane comment would not have fallen on deaf ears.

Since then, some significant banks have failed in America, and Credit Suisse in Switzerland as well. That has only increased bankers’ fears of risk over the entire international banking system — excepting China and Russia where economic and financial prospects are markedly better and isolated from the western banking system. So far, this new environment of lending caution has led to the withdrawal of credit principally from financial activities. It will soon become evident in the non-financial economy as well. And the recognition of systemic risk has spread to depositors shifting their deposits from smaller, regional banks where deposit protection is limited, to the larger banks deemed too-big-to-fail.

Much has been written about the on-balance sheet losses arising from investments in bonds, due to rising interest rates, bond yields, and yield curve inversions. Investors hope that the gathering crisis will mean an end to interest rate rises and a prospect that they will soon fall due to the somewhat patchy evidence of declining consumer demand. But this misunderstands the consequences of contracting bank credit.

Participants in both financial and non-financial activities depend on the ready availability of bank credit. But banks can refuse to novate outstanding loans and demand their repayment as they come due, and they can reduce their revolving credit facilities, sometimes with little notice in accordance with their terms. Demand for credit in the financial sector tends to continue or even increase for a while because investors are generally unaware of changing credit conditions. And industrial borrowers experience cash flow difficulties in an economic slowdown, requiring credit facilities to be sustained or even increased.

Consequently, a contraction in bank credit can increase demand for it, and there can only be one outcome: for the fewer borrowers who succeed in persuading their bankers to extend loan facilities, it will be at increased interest rates. Furthermore, the history of banking confirms this analysis is correct.

It is a myth, therefore, that a central bank can retain control over interest rates when the increase in commercial bank lending slows or even reverses. Hopes that banks in trouble and a deteriorating economic outlook will lead to lower interest rates are misplaced. But the tendency for interest rates to rise even further, driven by the withdrawal of credit irrespective of the inflation outlook undermines financial asset values even further with dire consequences for an economy, financial asset values, the funding of government finances, and for the commercial banks themselves.

It is at this stage that the folly of divorcing the value of credit from legal money will rapidly become apparent. With all the risks, with all the foreign ownership of dollars in particular, and with the prospect of a central bank prioritising the protection of financial asset values and underwriting the entire financial system, the value of credit is bound to face its most serious challenge.

The only remedy is unlikely to be adopted — reintroduce a firm link between credit and gold. A central bank would then have to ignore the consequences and severely limit the expansion of its own obligations, prioritising the maintenance of the currency’s value or face a run on its gold reserves. Given entrenched Keynesianism and central bankers’ group-thinking, it can be ruled out.

The future for credit

It would appear that the current dollar dominated fiat currency regime is drawing to a close. We can cite the following as evidence of its impending demise:

- The last fifty-two years since the end of the Bretton Woods Agreement culminated in a global financial bubble on a scale never seen before. It ended with negative interest rates in Europe and Japan (where they still persist).

- The unshackling of credit values from gold has fuelled credit expansion for financial speculation. The increasing financialisation of US, UK, and most European economies has chased production of goods abroad, hollowing out their economies, and increasing domestic dependence on ephemeral services.

- In the main, these conditions have not been supported by genuine savings. Instead, consumers rely on increasing levels of debt to maintain unaffordable lifestyles. This is in stark contrast with the principles behind the division of labour, whereby production is turned into consumption, with some of that consumption deferred to become capital available for driving economic progress.

- Bubble conditions have left massive amounts of unproductive debt, which cannot be repaid when due, and now the banks have neither the desire nor the balance sheet capacity to extend them. Properly accounted for, the entire banking system is so overleveraged that even losses in this early stage of credit contraction are estimated to wipe out bank equity in the US, Europe, and Japan.

- Having taken on massive quantities of government debt at the highest possible prices through quantitative easing, the major central banks themselves are in negative equity. They are in no condition to absorb the costs of assuming the liabilities of failing commercial banks without debauching their currencies.

The combination of a deflating financial bubble and a collapsing fiat currency resulted in the collapse of John Law’s Mississippi bubble. We see similar conditions today, justified in large measure by Keynesian macroeconomics, which pursue similar economic policies to those propounded by Law. It was the livre which became valueless then, so we can expect the existence of dollars, euros, yen, and pounds to be similarly threatened.

The moral of this sorry tale is that expanding credit is a good thing, creating wealth as incorporeal value subject to two conditions. Its value must be soundly tied to legal money, which is physical gold. And credit must only be created in anticipation that the debtor uses it wisely and that it will be eventually settled.

The rise and rise of Asia

While the major western currencies and their credit systems are descending into crisis, China in partnership with Russia is planning an industrial revolution for all of Asia. So far, they have been careful not to disrupt the international monetary system beyond expressing a desire to do away with dollars in their Asian backyard.

This changed with the invasion of Ukraine and the sanctions imposed on Russia. Russia’s currency reserves in dollars and euros were rendered worthless, and Russia is no longer selling her gold output into western markets, though she is selling some through Dubai and Hong Kong. Apart from these sales, the indications are that Russia is securing her currency by accumulating gold reserves and making gold in the Gokhran —the State Fund for Precious Metals — available for monetary purposes in addition to the Central Bank of Russia’s reserves. It cannot be confirmed, but it is thought that this secret fund holds an estimated 10,000 tonnes, so it will be possible for Russia to declare and demonstrate reserves considerably in excess of those held by the US Treasury.

China has undoubtedly accumulated substantial quantities of gold since 1983, when the Peoples Bank was appointed to manage China’s gold and silver reserves. Investment in gold mining and refining was stepped up, and China rapidly became the largest nation by gold mine output. Other than small amounts permitted for Hong Kong jewellery fabrication, no gold leaves China. And over 21,000 tonnes have been delivered into public hands from the Shanghai Gold Exchange since the public was first permitted to buy gold in 2002.

Given that the Peoples Bank began accumulating gold in 1983, between then and 2002 at contemporary prices China’s state-owned gold accumulation will have been substantial. It is likely to amount to some 20,000—25,000 tonnes, when capital flows and state policies towards mining and refining are considered. That amount has almost certainly increased since.

Whatever the figures, it is clear that both Russia and China anticipated a western currency crisis and have deliberately taken steps to protect themselves against it.

They understand what we have forgotten: the distinction between money and credit.