Market Report: Unchanged on the week

Jul 14, 2017·Alasdair Macleod

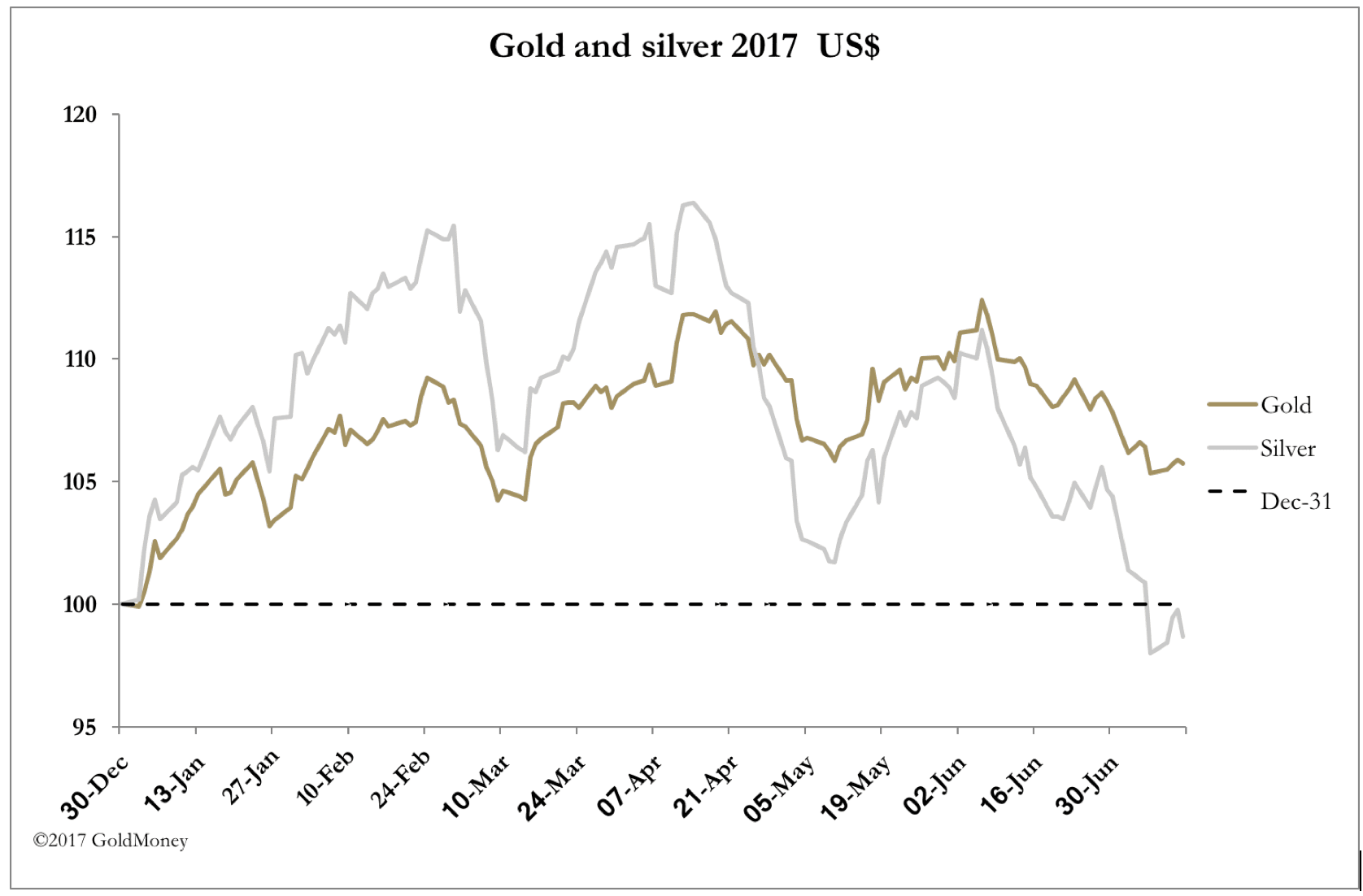

Gold and silver prices steadied this week, with gold up only $3 at $1218 in early European trade this morning (Friday), and silver unchanged at $15.68. As our headline chart shows, silver is now marginally lower on the year, and gold’s rise has been pared to 5.75%. All this has happened against a background of a weaker dollar, so in terms of performance, gold’s rise against the dollar is as good as it gets. Our next chart shows gold’s performance indexed to the start of the year against the four major currencies.

Priced in euros, gold is now down on the year, by 2%. The point is worth making to refute those who buy and sell gold on charts alone: they are ignoring the value gold offers most of the world’s population priced in other currencies. For example, there has been a rebound in Indian demand, with the official figures for May rising to 124 tonnes for the month. Given the smuggling trade, this is bound to understate the true figure. Silver demand also jumped sharply. Chinese public demand for gold in June rose to 155.5 tonnes, which for the first six months now stands at 1,021 tonnes. China and India between them are absorbing gold at an annualised rate of 3,160 tonnes, not far off total global mine supply. For this demand to be satisfied, the rest of the world, including members of the public, central banks and other government institutions such as sovereign wealth funds must draw down on existing above-ground stocks to satisfy their demand. This tells us that serious supply problems must be developing in the physical market, which is confirmed by backwardations for future deliveries.

We must look towards Comex for evidence as to what is going on, and here, the most striking data is the net contract position for the swap dealers. This is shown for gold in our next chart.

The net position is long 21,063 contracts (data correct at 3rd July), which is close to the record level seen in December 2015. The fall in the gold price since that date, to under $1210 at one stage, suggests the swaps have increased their net longs even further. This is important, because the bullion banks, represented by swaps, have closed their habitual shorts, and it is now in their interest to see prices rise.

Hapless speculators, in the form of hedge fund managers trading off the charts, are the fodder for the bullion banks’ profitable game, always at their most bearish before the market recovers, and conversely at their most bullish when the swaps are most short. This is confirmed in our last chart, which shows hedge funds to be almost level.

The important news event this week was Janet Yellen’s two-day testimony to the Senate, when she adopted a more dovish tone towards both interest rates, which she said were closer to a “neutral policy stance” than previously indicated. At any other time, this backing down from a more aggressive stance would have led to a more significant bounce in precious metals.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.