The US Government Debt Crisis

Apr 25, 2019·Alasdair MacleodThis article explains why the US Government is ensnared in a debt trap from which there is no escape. Its finances are spiralling out of control. In the context of a rapidly slowing global economy, the budget deficit can only be financed by QE and bank credit expansion. Do not draw comfort from trade protectionism: it will not prevent the trade deficit increasing at the expense of domestic production, unless you believe there will be an unlikely resurgence in personal saving rates. We can now begin to see how the debt crisis will evolve, leading to the destruction of the dollar.

Introduction

At the time of writing (Thursday April 24) bond yields are crashing, the euro has broken down against the dollar and equities are hitting new highs. Obviously, equities are taking their queue from bonds. But bond yields are crashing because the global economy is sending some very worrying signals. Equity investors will be hoping monetary easing (which they now fully expect) will kick the can down the road once again and economies will continue to bubble along. They are ignoring some very basic economic facts…

Regular readers of my Insight articles will be aware of strong indications that the expansionary phase of the credit cycle is now over, and that we at grave risk of falling headlong into a global credit and systemic crisis. The underlying condition is that economic actors and their bankers accustomed to credit expansion are beginning to realise the assumptions behind their borrowing commitments earlier in the credit cycle were incorrect.

That’s why it is a credit cycle. It is driven by prior credit expansion which corrals all producers into acting in an expansionary manner at the same time. Random activity, the condition of a true laissez-faire economy, ceases. Instead, credit conditions act on profit-seeking businesses in a state-managed context. Entrepreneurs take the availability of subsidised credit to be a profit-making opportunity. The same cannot be said of governments because they do not seek profits, only revenue.

If a government acts responsibly it should never have to borrow, except perhaps in an emergency, such as to defend the country against invasion. The evolution into unbacked fiat currencies has changed all that by permitting governments to finance themselves through the printing press.

There is only one way a government funds the excess of spending over tax revenue without it being inflationary, and that is to borrow money from savers. There is a downside to this. The government bids for existing savings, including those held in pension and insurance funds, diverting them from other borrowers. In the 1980s this was described as “crowding out” other borrowers and had the effect of increasing interest rates to the point where these other borrowers stop borrowing. In the post-war years, this has been the consequence of spendthrift socialism.

The other two sources of finance for high-spending governments are simply inflationary. Bank credit is expanded to finance short-term treasury bills and treasury bonds. Before 2008, a combination of savings and bank credit expansion was used to cover government funding requirements. But since the great financial crisis, money-printing by central banks through quantitative easing has opened a new avenue for government funding. It is this last financing mechanism which future historians are likely to attribute to the beginning of the end for fiat currencies.

Notionally, quantitative easing is promoted as a monetary policy to stimulate the economy by injecting large amounts of base money into a failing banking system and allowing banks to build their reserves. But the more important effect is it permits a government to spend even more beyond its tax revenues.

Keynesian theory, at least in its original form, recommended excess government spending to stimulate the economy early in what Keynes termed the business cycle. The assumption was that a stronger economy resulting from the earlier credit expansion would improve government finances by increasing tax revenue, and thereby achieve a budget surplus later in the cycle. From time to time governments still pay lip service to the concept of balancing the budget over the business cycle, but not so much now.

As a fiscal policy, balancing budgets over the cycle is no longer relevant; nor is the way in which deficits were funded in classical economic models. The character of today’s welfare-driven economies has changed, with the majority of consumers no longer saving, except though pension and insurance funds. In recent decades these institutionalised savings have reduced their exposure to bonds while increasing their equity investments. They seek returns through capital gains rather than compounding interest. Monetary policy has always favoured the suppression of interest rates and of lower bond yields, encouraging this trend. Savings as a means of financing government debt have virtually disappeared on a personal level and have declined in importance in all but specialised bond funds.

Therefore, the Keynesian desire to maximise current consumption by denigrating savers is almost fulfilled in a number of leading economies. The way in which welfare-driven spendthrift governments fund themselves has changed radically from when individuals invested their savings in government bonds. Instead, governments have become increasingly dependent on financing budget deficits by inflationary means.

US Government borrowing is out of control

There are a number of Western governments whose accumulating debt has become so large relative to their economies that their finances are undeniably out of control. For the purpose of this analysis, we shall restrict our attention to that of the US Government, because it is the issuer of the world’s reserve currency.

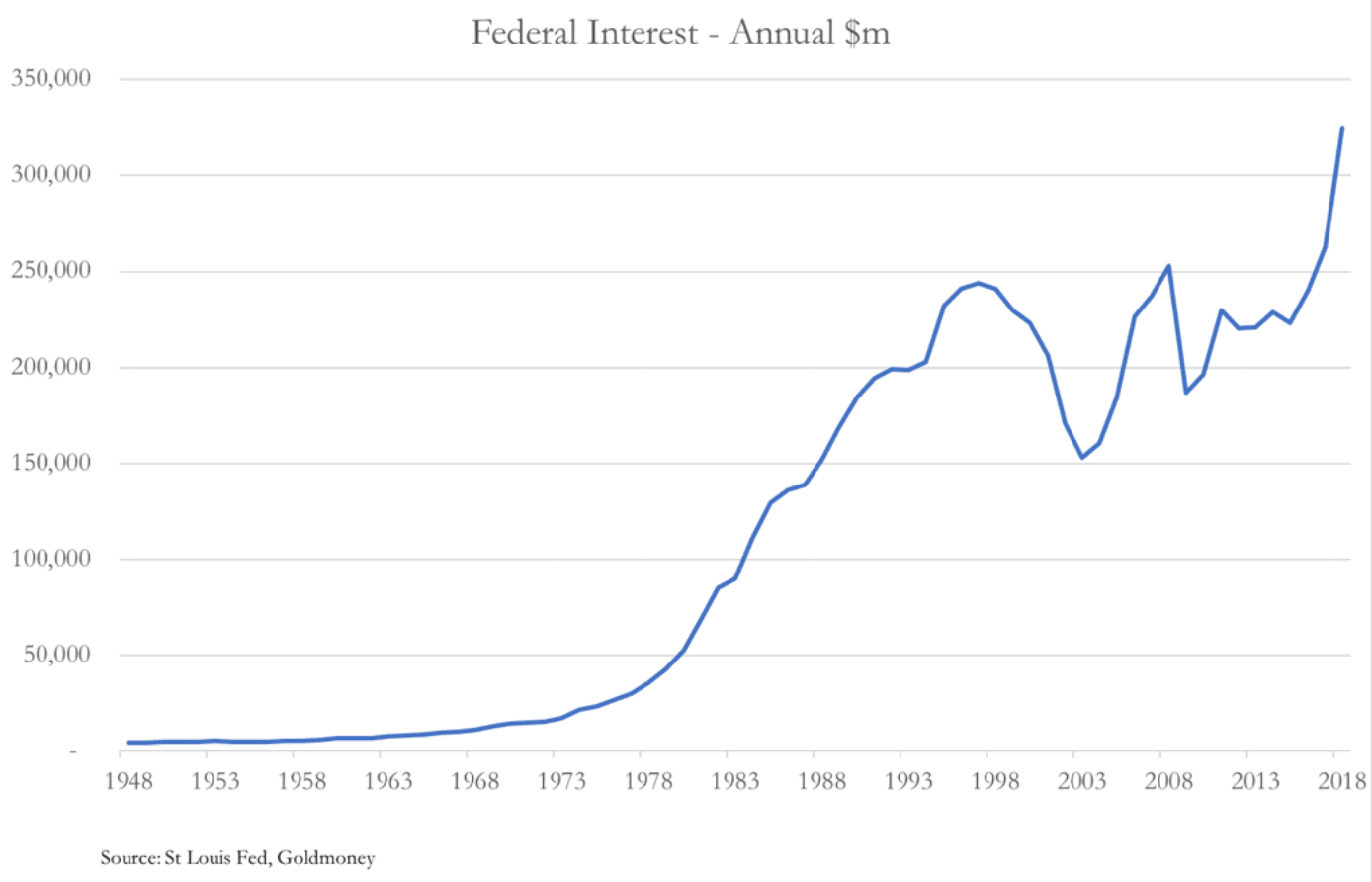

Despite the Fed’s suppression of interest rates over the long-term, the cost of federal government borrowing has escalated noticeably, as the following chart up to fiscal 2018 clearly shows.

My colleague, James Turk, calculates the US Government’s insolvency ratio (the interest cost as a percentage of government revenue) to be 17.2% for the first six months of fiscal 2019.[i] In other words, for every $100 raised in taxes, $17.20 goes to pay interest. On this measure, federal government finances are already in crisis.

The Congressional Budget Office’s out-of-date forecast for the 2019 deficit stands at $897bn. The most recent estimates from the Office of Management and Budget (part of the president’s office) is a deficit of $1,092bn for the year. In other words, the debt and interest problem has accelerated significantly in the last six months. Turk concludes the Fed has no option but to reduce interest rates to rescue the finances of the US Government.

It’s a pretty pass. The problem can be viewed from another angle: there has been insufficient growth in nominal GDP to produce the taxes to finance the debt. In the absence of GDP growth, the only way the threat of escalating debt can be addressed is by eliminating the federal deficit. Under current policies, that is not happening, and according to the CBO, budget deficits are set to increase out to 2028 at least.

For fiscal 2019, the CBO had assumed an increase in GDP of 5.02% and 4.08% for 2020. In the light of the sharp economic slow-down which is now becoming apparent, these estimates appear to be incorrect. In other words, not only is the US Government’s insolvency ratio going through the roof, not only is the budget deficit out of control, but the assumptions over GDP growth appear to be far too optimistic.

Since the Lehman crisis in 2008/09 the US Government has been using a singularly bad escape route from the GDP problem by fiddling the inflation figures. To appreciate the full ramifications, we need to understand what GDP represents. GDP is simply a total of recorded qualifying transactions in the economy during a stated period, normally annual or annualised. Growth in the GDP number is not a record of anything else other than monetary inflation applied to those qualifying transactions. In other words, the solution to the lack of inflation in the GDP number is to simply inflate it. This is done through accelerated quantitative easing and by the Federal government increasing its spending in the domestic economy.

As a fix, it may temporarily benefit government finances. But it is the worst thing a government can do, because through wealth-transfer it impoverishes and destroys the non-government economy upon which the government relies for its future tax revenue. While the attractions of easy money to a spendthrift government are immediate and doubtless will be recommended by mainstream economists and commentators, it is the road to accelerating price inflation and the eventual collapse of the currency.

To date, the effect of monetary inflation on the economy has been deliberately concealed. If it had not, the true state of government finances would have been obvious to the general public years ago. By statistical method, mandated index-linked adjustments for price inflation have been reduced to a fraction of what they should be to reflect the true cost of living. When it comes to considerations of pure cost, the benefits of this suppression to government finances are obvious. The more insidious problem is that cost overruns dominate government spending, reflecting the true effects of monetary inflation on prices.

It is an increasingly serious problem. According to the Chapwood Index[ii], price inflation on the goods and services Americans typically buy has been running at close to 10% on average in 50 major cities over the last five years. Instead, financial analysts doggedly accept government CPI statistics, which claim price inflation has averaged only 1.52% over the same timescale. The Chapwood Index reckons by mid-2018 prices were rising annually at 12.6% in New York City, 12.1% in Los Angeles and 11.9% in Chicago. If we accept the Chapwood estimates and apply them as a GDP deflator, we must conclude that in real terms the US economy has been in a continual slump since the financial crisis, and that there is a huge gulf between official interest rates and those that would be demanded by savers if free markets were permitted to operate properly.

One of the oldest clichés in politics is you can fool all of the people for only some of the time. There will come a point where all of the people, collectively the markets, wake up to state-sponsored statistical fraud. With price inflation appearing to accelerate, public apathy over price inflation will be replaced by a substantial and possibly sudden adjustment to money-preferences relative to goods.

The timing of an economic awakening is likely to be linked to the credit cycle, when public support for reflationary actions evolves from complacency to sudden concern. It is one thing to tolerate government intervention when things appear to be going reasonably well or there is a prospect of it succeeding, but when the economy runs into trouble a different mood prevails. If the recent economic slowdown gathers pace public psychology will make that change.

I have argued in other Insight articles that the combination of trade protectionism and the end of the expansionary phase of the credit cycle is a lethal economic combination.[iii] The empirical evidence from the 1929-32 episode could not be clearer. At that time, the Smoot-Hawley Tariff Act coincided with the top of the 1920s credit cycle. Through its trade policy, the US Government is imposing the same conditions today that led to the Great Depression in the 1930s. This time the same combination is being applied with the dollar as reserve currency, backed only by what will become the diminishing faith in and credit of the US Government. And we will then face the prospect of a further acceleration of money-printing in the form of QE.

Assuming the conditions of the 1929-32 Wall Street crash are being only half-replicated, US Government funding requirements will go through the roof. Under the guise of bailing out a deteriorating economy, it is clear that the US Government will not cut its spending. We are seeing a well-established maxim being proved, and that is no government with a fiat currency can resist resorting to the printing press.

The foreign dimension is changing things for the worse

The most inflationary funding mechanism is for one government department (the treasury) to issue bonds to the public and the banks, and another government department (the central bank) to buy them off the public and the banks by issuing raw currency. So as to not raise inflationary suspicions, this overtly inflationary mechanism is called quantitative easing and it is set to return big-time.

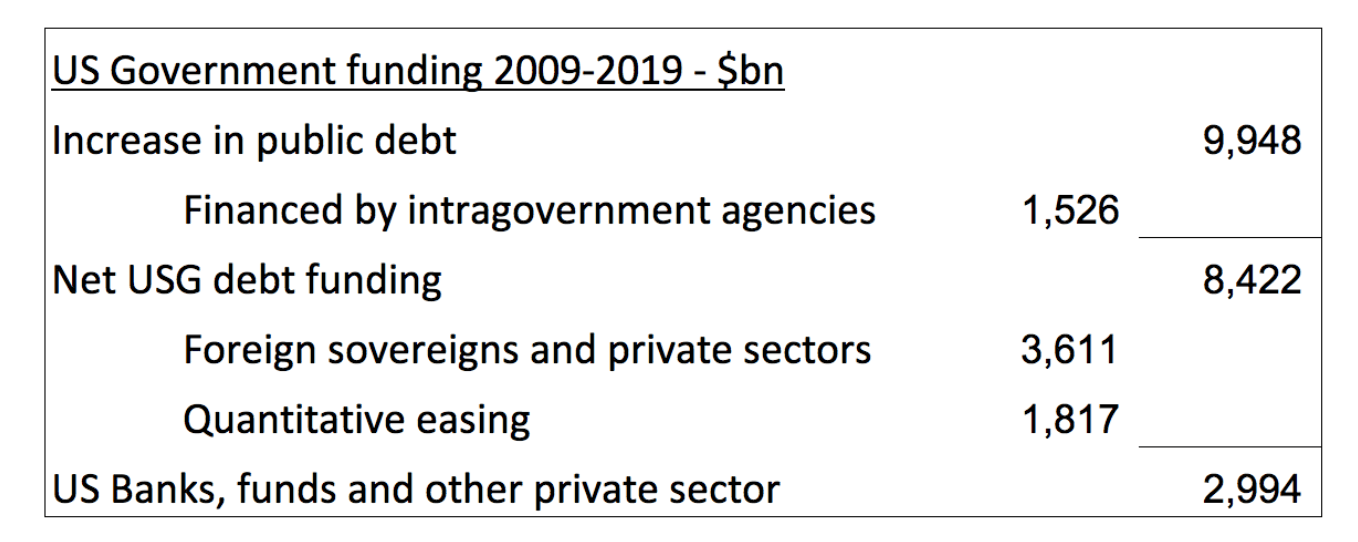

So far, QE has covered only part of the US Government’s funding requirement since the Lehman crisis. The full breakdown is shown in the following table, which incorporates both long-term and short-term debt.

It should be noted that foreigners bought an estimated $3,611bn of Treasury debt, significantly more than US banks, funds and other US private sector investors.[iv] By mid-2018, total foreign investments in US Treasuries amounted to $6,201bn, so their holdings have more than doubled since the Lehman crisis. Foreign funding of US debt is the consequence of trade deficits, because dollars end up in foreign hands. It is only part of the trade deficit reinvestment story, but that is what concerns us here.

Foreigners invest in US Treasury and other dollar assets because they need a reserve of dollars to facilitate international trade. Furthermore, with few exceptions they are the most important component of foreign exchange reserves maintained by foreign governments, their central banks and sovereign wealth funds.

Therefore, the level of foreign ownership of dollars is determined primarily by the long-term outlook for trade conditions. If trade is generally expanding foreigners will tend to increase their holdings of dollars, and if trade is contracting, they are likely to reduce them. Some holders will speculate by holding more or less than they normally would on trade considerations alone, but the underlying relationship between the volume of trade and dollar holdings is the most important factor.

In recent years there has been a tendency for some central banks and sovereign wealth funds to reduce their dollar exposure, leading to liquidation of their US Treasury holdings. Between 2015-18, foreign governments and associated sovereign accounts sold a net $893bn of US Treasury securities, most of which was compensated for by foreign private sector purchases. Private sector holdings are likely to be more influenced by the trade outlook than government holdings, which are more strategic in nature.

Given the deteriorating outlook for international trade, it appears likely that foreign corporations will now reduce their dollar holdings, adding to net sales by foreign governments. That being the case, at the same time that the US Government’s funding requirement starts increasing above forecasts, foreigners will be liquidating their Treasury holdings and selling dollars. Therefore, QE is set to become the principal funding mechanism for US Government debt.

Those who reckoned that the Triffin dilemma would guarantee infinite demand for the dollar despite the US Government’s poor financial management could be in for a severe shock. The long-run effect on both the dollar and bond yields is clear to see and should not be underestimated.

How an increasing budget deficit intensifies the slump

Neo-Keynesian economists claim that a budget deficit puts demand into the economy that otherwise would not be there. Along with everyone else they will be alarmed at the speed the budget deficit escalates during a slump, but they are sure to argue that to reduce it will only make things worse.

Assuming there is no change in the savings ratio, the twin deficit phenomenon suggests that an increasing budget deficit will be matched by an increasing trade deficit. (A fuller explanation of the relationship between the deficits and changes in the level of savings is to be found here.) The source of confusion over what is a simple accounting identity is the Keynesians’ denial of Say’s law, incorrectly described by Keynes himself in his General Theory. The correct interpretation of Say’s law is that socially active humans specialise in their production to acquire the goods and services they don’t produce yet need and desire. Money is no more than the transmission mechanism which turns production into consumer goods. Money saved turns production into future goods. It is why the division of labour works to improve our living standards more effectively than any other form of social cooperation.

The key bit is the role of money. Through their control of currency, governments and their licenced banks inflate its quantity. More currency in circulation acts on demand without it being earned and therefore the extra goods and services being produced. Inevitably, prices tend to rise as that money is absorbed in the existing framework of production and consumption. And when prices rise, demand switches to extra imports.

If people saved the inflated money, it would not fuel consumption and therefore a trade deficit would not arise. But Keynesians discourage saving, and as noted earlier in this article, their misplaced policies have virtually destroyed personal savings, except for institutionalised pensions and insurance funds. Allowing for consumer debt, to all intents there are no consumer savings in America. The budget deficit is therefore financed almost entirely by inflationary means, so when an economic slump increases the budget deficit, it must also increase the trade deficit.

Far from maintaining demand levels an increase in the budget deficit, by leading to an increase in the trade deficit, has a catastrophic effect on domestic production. This is because in slump conditions an increasing trade deficit will simply displace domestic production. And attempts to alter the balance in favour of domestic production by raising tariffs against imported goods always fail because of the twin deficit problem. A close study of the consequences of the Smoot-Hawley Tariff Act illustrates this point in spades.

Therefore, unemployment will rise, and the currency will fall. Doubtless, Keynesians will console themselves that a lower currency makes labour costs competitive, an error from which they have been proved incapable of learning. What they miss is that a savings-driven economy, which tends to run trade surpluses for the same reasons a country like America without savings runs deficits, uses consumer savings to invest in reducing unit production costs and improved products. This is shown to be the case by empirical evidence from Germany and Japan in the post-war years, when their rising currencies failed to eliminate their export surpluses.

All that will happen is foreigners end up having more dollars to sell. The currency weakens on the foreign exchanges while its purchasing power in the domestic economy declines. The US Treasury will be funding escalating budget deficits and killing domestic production in the process.

Why bond yields will rise, and the dollar will fail

In the great depression, the dollar was convertible into physical gold at $20.67 to the ounce, and then notionally at $35 from January 1934 onwards. This meant that the interest cost to the US Treasury reflected that of lending gold plus a premium for issuer risk. Today, there is no gold backing, and lenders are aware they must take currency risk into account.

So long as lenders believe government finances are reasonably stable and state-issued statistics are credible, a central bank can depress borrowing costs through an expansionary monetary policy. This is the current position; but when it is no longer the case, a central bank faces an impossible task.

If my thesis that a combination of trade protectionism and the top of the credit cycle is leading the global economy into an economic slump is correct, the consequences will dramatically undermine the US Government’s finances for the reasons detailed in this article. Budget and trade deficits will escalate; the former can only lead to the most inflationary form of funding being deployed and the latter will depress domestic production. And at its hour of greatest need, foreigners will be selling down their dollar portfolios, visiting a new, post-Triffin crisis upon the nation.

It will soon become obvious that the US Government, along with all other high-spending states, is caught in a debt trap of its own making. The folly of post-Keynesian economic and monetary policies, designed to justify governments’ economic existence, will be fully exposed. And as bond yields and the dollar head towards an Argentinian adjustment, the days of the dollar and dollar-denominated debt will be numbered.

[i] See https://www.fgmr.com/heading-toward-the-tipping-point/

[ii] See http://www.chapwoodindex.com/

[iii] For example, see https://www.goldmoney.com/research/goldmoney-insights/trump-s-trade-tantrum-triggers-slump

[iv] The amounts in the table are derived from US Treasury TIC data. Changes in foreign holdings are derived from Annual Reports at https://www.treasury.gov/resource-center/data-chart-center/tic/Pages/fpis.aspx. These reports are to June, three months prior to the fiscal year-end. This difference is ignored for the sake of clarity.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.