The end of the bank credit cycle

Jul 8, 2021·Alasdair MacleodThe economic consequences of cyclical expansion and contraction of bank credit are the reason for booms and slumps dating back certainly to the Napoleonic Wars and possibly before. Keynesian remedies, which owe their pedigree to the financial theories of John Law, have never succeeded in taming them.

This article ties Austrian business cycle theory to the cycle of bank credit. It explains how bank credit is created and customer deposits with it through double-entry accounting.

Central bank interest rate suppression has led to the virtual death of bank credit creation for the benefit of non-financial businesses. Instead, banks have grown their balance sheets to finance purely financial activities and speculation to compensate for reduced lending margins.

The cyclical contraction in bank credit is set to be greater than anything we have experienced since the Wall Street Crash of 1929—1932. The authorities’ attempts to defray this reality seems set to undermine the purchasing power of their currencies.

He was initially denied permission, but the following May Letters Patent were issued to him for a private bank, and Law was in business. The conversion to the Royal Bank — effectively operating in the name of the King — came later. There was no question about Law’s intellectual capacity and his ability to convince. And Law was followed two centuries later by a doppelganger Keynes, who unwittingly adopted the core of Law’s theories, and certainly much of his approach to money and economics.

In the wake of Keynes’s quick fixes, the study of the relationship between credit and business cycles become neglected. Rather than enquire into why a periodic slump occurred it was easier to just assume a cause. Keynes effectively declared that the free market fails because it is flawed. His solution was state intervention to correct it. And when economic aid from the state turned out to be only a temporary fix because the economy slumped again, the original assumption was never questioned: it simply prevailed, and the intervention was repeated, and continues to be by his followers today.

Economists, commentators, and investors are all aware that cyclical factors affect both asset values and economic activity. Some investors swear by their favourite cycles. But in the field of economics, cyclical theory has been primarily associated with the Austrian school of economists, principally in Ludwig von Mises’s writings on trade-cycle theory and Friedrich von Hayek’s triangle. Today, these are collectively referred to as Austrian business cycle theory.

Austrian school explanations of booms and busts added significantly to our understanding and the links with fluctuating credit were examined and understood by both Mises and Hayek. And these cyclical failures are still clearly embedded in our economies. To revive this important subject, we must discard neo-Keynesian economic assumptions and return to basics, adapting and augmenting the Austrian school’s findings for modern times.

Hayek used this model to illustrate the effect of interest rates on the rate of savings and the consequences for business calculation, pointing out that capital was released in the form of increased savings by a fall in immediate consumption. It was subsequently explained thus:

“The number of stages of production that can be sustained by the market depends on the time preference of consumers. For instance, a reduction in time-preference increases the supply of loanable funds and reduces the interest rate in the market, other things being constant. This increase in savings allows for extending the triangle by augmenting the financial capital needed to add stages of production. . . The Hayekian triangle offers a simplification of capital theory in order to emphasize particular features such as the effects of market interest rates on how long production takes in an economy.”[i]

There are elements of this statement (which was not Hayek’s) that appear to be on weak ground. For example, the suggestion that a reduction in time preference (in other words, a reduction in interest rates, which in free markets amounts to the same thing without any time lag) increases savings. But surely, a fall in interest rates can be expected to have the opposite effect, diverting savings into consumption. Clearly, for this statement to be correct there must be other factors in play that override an expected supply/demand curve. The explanation is found in bank accounting practices, as will be explained later in this article.

Hayek’s triangle supposed that with increased investment being the consequence of reduced consumer spending, there is a shift in profitability from retail activities towards earlier stages of production. The increase in capital investment from greater savings was directed accordingly. And the reduction in time preference reduced the time penalty incurred for future production. Therefore, more roundabout methods of production became viable.

That manufacturing roundaboutness increased with the capital available was originally proposed by Eugen von Böhm-Bawerk, an earlier economist of the Austrian school, and for a time Austria’s finance minister. The triangle was Hayek’s attempt at explaining the relationship between investment, time and means of production. As an explanation it appears to have begun to be accepted before the economic establishment migrated to Keynesianism following the publication of Keynes’s General Theory, which broadly removed time factors from mainstream economics.

There is much detail to consider behind Hayek’s triangle, but there are contradictions within it to consider as well, and a contradiction in the theory of roundaboutness should be obvious to economists today. It fails to address an obvious fact revealed by modern logistics. Irrespective of changes in savings, by specialising in production improvements can always be expected in the combination of cost, quality and reliability compared with a manufacturer undertaking all the manufacturing processes itself. Therefore, over time the final production of capital goods and consumer durables has increasingly become a process of assembly of pre-manufactured components from diverse sources. This evolutionary process has had little to do with changes in time-preference, and more to do with the advantages of globalisation.[ii] The Hayekian approach also ignores the benefits of scale to a specialist manufacturer making components for a wide range of assembling manufacturers, which would inevitably occur to readers of Adam Smith’s description of a pin manufactory in the first volume of his The Wealth of Nations.

Arguably, a second flaw in this approach is tagging the cycle as one of business activity. Ludwig von Mises described it as a trade cycle. Both descriptions are misleading in the sense that the cycle’s origin lies in bank credit. All economists would have profited by giving greater credence to the practicalities and consequences of bank credit creation in the global banking system that has existed since at least the 1844 Bank Charter Act in English law, and in England from the time of the early goldsmiths in London.

Theorists assume that higher interest rates towards the end of the credit cycle alter the balance between savings and consumption by attracting more savings and less consumption. That is an error. From a banker’s point of view, higher interest rates are the consequence of increasing lending risk and reflects a desire to reduce the supply of credit. And through the process of double entry book-keeping, a reduction to lending exposure is matched by a reduction to the principal source of balance sheet funding, which is the bank’s liability to depositors. Conversely, lower interest rates reflecting lower lending risk are the result of the banking sector’s desire to expand their loan books, and not as commonly supposed is driven by a surfeit of savings.[iii] This is why bank deposits increase early in the credit cycle, and at this point concurs with Hayek’s triangle; except the origin of deposits is not from consumers’ savings but the expansion of bank credit. The process of deposit creation is explained in more detail below.

It is the practicalities of bank accounting that drive the rise and fall in the quantity of deposits. This is the reverse of what the laws of supply and demand with respect to allocation of savings would suggest. The error is to regard interest rates are the price of money, a mistake that even underlies the monetary policies of central banks.

We can sum up the situation with an iron law of banking:

By lending money into existence, banks create deposits. Therefore, an increase or decrease in overall levels of deposit are not at the savers’ behest, but at that of the banks.

Far more constructive to an understanding of business cycles, in my view, is an approach that gets to their origin and without any doubt that is a cycle of bank credit expansion and contraction. Genuine savings do provide businesses with capital, but that is through direct channels, which may or may not be augmented by bank credit. Why changes in the amount of bank credit lead to a cycle of business activity must form the basis of our inquiry.

The form and impact of periodic credit contractions vary from cycle to cycle, and there are the distortions resulting from state interventions as well. But clearly — except to a hard-line Keynesian perhaps — there is an underlying cycle. And in the study of any cycle, we need a starting point. In anticipating that credit is involved, we must first describe an economic model with a constant quantity of money and credit, and the absence of state intervention as a reference point. And we will also assume that the purchasing power of money overall does not vary much because it is fundamentally sound.

The producers evolve themselves into businesses with employees, supplying all the community’s needs and wants as demanded of them. Anything imported, because it either cannot be produced locally, such as raw materials, or is made better elsewhere, can be done so freely on condition that imports are paid for, either covered by exports of the community or by the export of some of the community’s stock of money. In the latter instance, a net export of money will tend to increase its scarcity within the community, thereby reducing domestic production prices relative to those of imported goods. By making exporting more attractive and imports more expensive and a central authority not intervening, a balance between imports and exports is always maintained.

Putting fluctuations in the quantity of money from trade with other communities to one side, the total money received by the producers in investment capital and sales of goods from consumer spending and saving will be unchanged from year to year. What will change continuously is how the flows of money progress, driving up some prices where demand has increased while other prices fall where demand has declined. By their bidding activity for capital funds, entrepreneurs and manufacturers may cause the split between immediate and deferred consumption to fluctuate.

Businesses that fail to achieve adequate profitability or fail entirely, redeploy, or find their resources redeployed for them more profitably. This is Schumpeter’s creative destruction in action. And always, through a process of continual reassessment producers use the means at their disposal to maximise their profits by competing to be the best at satisfying the evolving demands of consumers.

Sound money and the division of labour are together the mainspring of economic progress, the improvement of Man’s condition, and is the basis of free trade between individuals. It was endorsed by classical economists. It requires flexibility in the use of money, its users to set its overall demand and not the state, and it certainly does not need the inflation of credit by a state-sponsored banking system. But that is what we have. Now, we must inject a variation in the quantity of money in the form of bank credit and see how our simple and inherently successful model of a free-market economy based on sound money responds.

In the bank’s books, the loan is obviously an asset for the bank. But at the exact time the loan contract is signed, the same customer’s current account is credited with the full amount of the loan. No other party is involved. Of course, the customer’s bank statement might look different, but that is just presentation. What matters are the bank’s own accounts.

But a bank with so little credit exposure compared with its shareholder’s capital is not very profitable. And given that it has been granted a licence to issue credit, it will almost certainly grow its own balance sheet in the search for profits.

Then its balance sheet might look like this.

Again, it must be emphasised that all customer deposits have been created because of loan agreements. Other depositors might open current and deposit accounts, almost always shifting balances from elsewhere in the banking system. And some with credit balances and no loans might close their accounts, shifting the proceeds to other banks. For the sake of our illustration, we shall ignore these activities, which when they lead to net changes are cleared through wholesale markets or a clearing house and have no direct involvement with the credit creation process.

Having increased its balance sheet to 6,000,000, we should note that lending money to customers at an average of, say, 8% becomes the gross margin, because the balancing current account cost the bank nothing. This is the profitable benefit of creating credit by book entry. The bank in our example is now earning a gross income of 400,000 on its loan book. We can further assume its capital is invested in short-term government treasury and commercial bills discounted to give an average annualised yield of, perhaps, four per cent. The bank’s total income at the end of a year’s trading including earnings on its own capital becomes 440,000; a gross return before expenses of 44% on the bank’s capital of one million.

Shorn of unnecessary expenses, it can be seen that bank lending through credit creation is immensely profitable. Admittedly, not all lending works like this. Banks also encourage deposits upon which they pay interest, in the same manner as the goldsmiths in the 1650s referred to above. But these funds can be loaned for even higher margins, such as to credit card holders with uncleared balances and small borrowers’ overdrafts. But for illustrative purposes we shall stick with our focus on a loan book involving larger borrowers.

Now let us turn to the economic effect. We will assume that a ratio of bank assets to capital of 6:1 is deemed by the banking community to be conservative. In other words, the balance is struck with bankers generally cautious about lending risk, having reduced their balance sheet gearing from higher levels during a preceding business recession. Uppermost in their minds at this point would be the memory of losses from defaulting customers as business conditions turned sour in the recent downturn.

These are the business conditions that promise a return to economic stability. When bankers become increasingly confident that the worst is over, they will begin to cautiously increase their lending again, predominantly to experienced businessmen they have reason to trust. Gradually, backed by bank credit made available to them, these businessmen acquire and reorganise failed and under-performing businesses — evidenced by a pick-up in takeover activity in stock markets usually seen before the economy begins to recover in earnest.

Corporate activity helps drive stockmarkets into recovery, even while unemployment is still high. But gradually, the reorganisation of production by company doctors and the like leads to a pick-up in hiring of skilled labour. The improving environment in financial centres increases professionals’ income, for lawyers, accountants, investment managers and the like. Investment banking becomes immensely profitable from these early-cycle activities, and the spending of those employed in all these specialisations leads to a localised boom for service industries in financial centres, spreading outwards into their commuter belts.

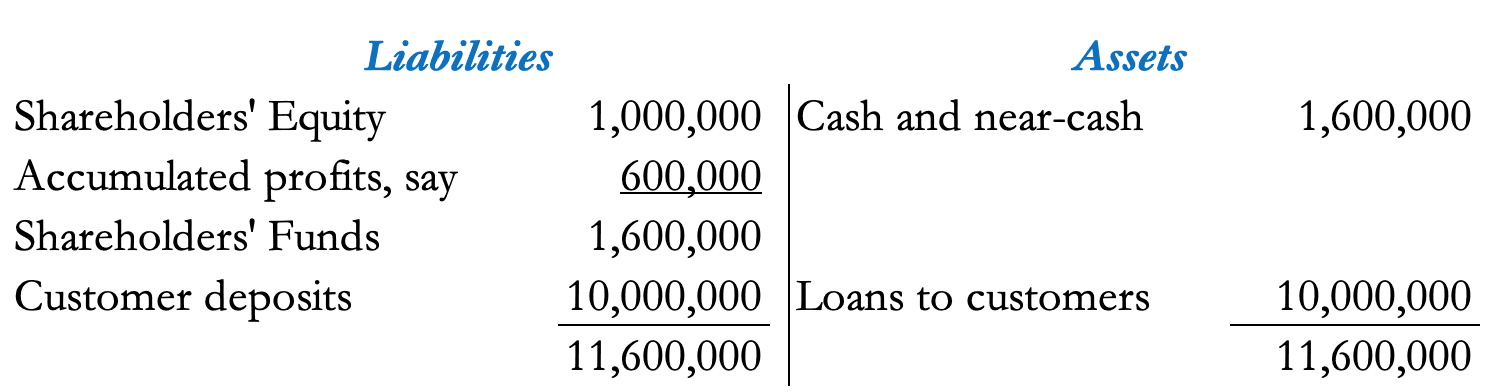

Naturally, the mood infects lending bankers with increasing confidence, realising that their earlier caution is now leading them to miss lending opportunities. They begin to compete with other banks for loan business, focusing on commercial property perhaps, property development and equipment leasing. Competition between banks begins to erode profit margins, and they compensate by expanding their balance sheets even more. Two or three years into the recovery, our sample bank’s balance sheet might look like this:

The bank’s liabilities due to shareholders reflect accumulated profits, net of operating other costs and taxes, after perhaps three years trading into the business recovery. Loan business has doubled. But the asset to equity ratio is now based on the larger figure of shareholders’ funds, leading to a modest increase of balance sheet gearing from 6:1 to 7.25:1.

Competition for loans has led to a reduction in interest charged on new business. Furthermore, our bank is exposed to other banks luring away pre-existing loan business. Therefore, if we assume that the average loan interest rate charged falls from our assumed initial rate of 8% to 5%, then a doubling of customer loans has only generated an extra 100,000 of gross interest income. The bank’s profitability relative to its capital has declined sharply, and with its executives growing increasingly confident of business conditions, the solution is to throw caution to the winds and seek yet more lending business.

Meanwhile, the economic effect of this credit expansion has been to fuel a boom in business conditions, which becomes unsustainable without further credit expansion. In the easing lending conditions, the quality of business borrowers has notably declined. Increasingly, bankers find that conditions in the market for loans have stopped meeting their earlier criteria. Manufacturing costs have begun to rise, there are shortages of skilled labour, and there are growing delays on the delivery of manufacturing and other essential equipment. The cash flows of the weaker borrowers are beginning to reflect the strains.

Initially, these warning signals are ignored in favour of yet more balance sheet gearing. Anyway, a 7.25:1 ratio of balance sheet assets to shareholder funds is still seen as conservative. But with commodity prices and price inflation for consumers now rising, pressure from the foreign exchanges for greater time preference forces the central bank to begin to raise interest rates. Initially, this benefits commercial banks because it puts a floor under loan rates. Commercial banks will continue to increase their asset to equity ratios, further encouraged by recovering lending margins. But in an early warning sign, stock markets begin to weaken under the influence of rising bond yields. A small cloud emerges on the horizon over future loan collateral values.

The economic consequences of the rapid increase in bank credit are embodied in further price increases, from commodities through business services to retail. While full employment guarantees increasing consumer demand, cost pressures reduce manufacturers’ margins. Business failures begin to mount. After eight or nine years of credit expansion, our cohort of bankers suddenly sense the danger of multiple business failures and begin to deny extra credit, beyond what is necessary to prevent existing borrowers from going under. By limiting credit availability, their response leads to a sharp rise in borrowing costs.

Greed for profit rapidly turns into fear of losses. The interest cost of bank borrowing increases for anyone who can get a loan. Banks now desperately want to reduce their balance sheet exposure because balance sheet gearing, of perhaps ten to one at this stage, means that a ten per cent loan write-off across the board renders equity in the bank worthless. The suddenness of the imperative to contain lending risk explains why when it comes the crash is both sudden and indiscriminate.

As mentioned earlier, expanding bank credit to finance production is only one activity pursued by modern banks. But at the core of all activities is financing through the creation of bank credit. A second definition of a banker to the one earlier in this article is that he is “a trader who buys money, or money and debts, by creating other debts”.[iv] Consequently, when conditions turn sour a banker tries to unwind his position as rapidly as possible, having no interest in the fate of the bank’s borrowers beyond what can be recovered from them.

A cycle of bank credit is a more relevant description of the origin of periodic booms and slumps than describing them as a trade or business cycle, which implies that the origin is in the behaviour of banking customers rather than the banking system. And trying to fit a cycle of interest rate changes into a cycle of production as Hayek attempted to do requires a deeper understanding of bank accounting than economists normally possess.

The question inevitably arises as to where we might be in the current credit cycle. The last crisis phase can be easily pinpointed to the Lehman collapse in August 2008. Compared with previous cycles, this one’s expansionary phase is now longer than most, assuming it is still running.

Identifying the next credit crisis in retrospect will be obvious. But identifying the end of the expansionary phase has become complicated by other factors. The increasing financialisation of the major economies together with a growing involvement of nearly all governments in their basic economies have altered the emphasis of bank lending away from the business lending of old. Today, the major banks are as likely to create credit to finance their own trading activities. And the proportion of bank credit that goes to finance portfolios of government and other securities has also increased. But even allowing for these factors, the FRED chart below shows that commercial lending peaked in May last year after initial covid-related distortions. Adjusted by the increase of credit in the economy (money M2 has increased by 36% during the time covered in the chart) the contraction of bank lending in the economic context is even greater than the chart suggests.

A further important factor has been increasing intervention in asset markets by central banks. The Fed, the Bank of Japan, the European Central Bank, and the Bank of England all invest directly or indirectly through quantitative easing and like measures to ensure financial assets maintain and increase in value. For now, at least, this has removed the risk of falling collateral values which is traditionally associated with a collapse in bank lending. And by nailing interest rates at the zero bound, the evidence of higher interest rates emerging due to pressure from banks to curtail their lending has been supressed.

Consequently, evidence of the end of the cycle of bank credit is barely noticeable, not only to observers but to bankers as well. But bank lending probably ran into an end of cycle crisis in September 2019, when the repo market blew up — eleven years after the Lehman failure. That being the case, the cycle’s duration would have been similar to earlier ones.

The ending of it, if that was what the repo crisis indicated, was not evidenced by bankers calling time on lending. Rather, it appears that larger banks active in financial markets collectively ran out of balance sheet capacity. Bankers had also behaved differently ahead of the Lehman crisis, failing to anticipate the events that led to the whole banking system needing to be rescued, instead of precipitating the collapse by their own actions. Something has changed their end-of-cycle behaviour, which is our final topic.

This has not entirely stopped the process of credit creation for non-financial businesses. But creditworthy borrowers have access to capital markets as well, and with central banks suppressing bond yields through quantitative easing, for banks the risks of lending to business customers are significantly greater than the interest rate compensation. This leaves banks lending to businesses that don’t have access to capital markets, which they are generally reluctant to do.

In effect, while monetary policy is implemented to stimulate the economy, it is strangling bank lending. The implications should not be dismissed lightly, because most money in circulation owes its origin to credit owed to depositors and its maintenance depends on banks not contracting their balance sheets.

Nowhere is this problem more evident than in the Eurozone, where in some jurisdictions lending to businesses appears to have almost ceased.[v] In common with banks elsewhere, Eurozone banks have turned to other activities, notably expanding credit to finance burgeoning state debt. And to maintain nominal profits in a negative interest rate environment, they have expanded the ratio between assets and equity to record levels.

The usual top-of-lending-cycle balance sheet gearing between assets and equity is in the region of ten, perhaps twelve times — enough to precipitate a major lending contraction in earlier times. Yet here we see major banks (the Eurozone’s globally important banks — the G-SIBs) with ratios of up to thirty times. The reason they have become so high is a combination of regulatory bias determining risk weightings in favour of sovereign debt, the interest rate environment imposed by the ECB and funding of speculation in securities markets replacing conventional bank lending. While the European Banking Authority takes the view these banks are solvent, their shareholders appear to believe otherwise, evidenced by their market capitalisation being below book values in all cases, illustrated by the column on shareholder leverage.

Clearly, bank lending to businesses in all major jurisdictions is being restricted by central bank interest rate policies. The focus of bank credit creation has shifted from providing finance to businesses, to low-margin financing of ever-increasing government deficits as well as financial speculation. In the case of the Eurozone, statist debt levels for Spain, Italy, Portugal, and even France have now spun out of control, accelerated by Covid and the availability of bank credit to buy their bonds.

There are two identifiable systemic threats emerging. The first is that the expansion of central bank money will be needed to replace bank credit when it ceases to expand and reverses — and history says that at some point it will. And the second threat is associated with monetary inflation, which is the effect on fiat currencies’ purchasing power. For the moment, the timing of the former is up in the air. But we can already see how rising prices, which are the evidence of the falling purchasing power of fiat currencies, are going to drive interest rates higher. Higher interest rates mean falling bond prices and the end of the stock market bubble. They also mean accumulating losses on bonds bought by the banks, and the loss of collateral value held against loans to business customers and stock market speculators.

For the moment, central banks are united in denying the interest rate threat. But increasingly, market actors are beginning to understand its reality. When they act, we are likely to see a market crash on the lines of John Law’s Mississippi bubble. The global unwinding of credit will then become a panic impossible to stop. We will almost certainly see interest rates rising to reflect the banks’ struggle to reduce their balance sheets to more normal levels relative to their shareholders’ capital.

Finally, we should take note that the monetary authorities will have no option but to attempt to replace contracting bank credit with their own form of credit — promises to pay nothing but folding paper in the form of fiat currency. The quantities required will almost certainly be proportionately far greater than the open cheques written by central banks to save the financial system following Lehman. This time, with G-SIB balance sheets to equity ratios on my estimation in the EU arithmetically averaging 20.5, the UK’s at 16.8, Japan’s 21.4, China’s 13.6, and the US at 11.2 times, the contraction of bank credit back to levels more normal for the beginning of a bank credit cycle will almost certainly be more financially violent than anything seen since the Wall Street Crash of 1929—1932.

The evaporation of collateral values will almost certainly be seen by policy planners as central to the collapse in bank credit, so central bankers’ instincts will be to accelerate their support for bonds and equity prices, while maintaining the availability of cheap mortgage finance to stop property prices imploding. Expect official interest rate rises to be reluctant and less than required to stabilise currencies. Expect the Fed’s QE to escalate from $120bn a month and other major central banks to act similarly.

Earlier it was noted that the vast bulk of money in circulation has its origin in bank credit. The task of replacing it with central bank fiat currency seems set to destroy the purchasing power of the currencies, which coincidently was what happened to John Law’s livres 301 years ago. Courtesy of his successor in stimulus policies, Lord Keynes, the same outcome faces economies today on a global scale. It is increasingly impossible to see any other outcome from the development of the current situation.

[i] As quoted from in McClure, James E, David Chandler Thomas, and Lee C. Spector. “A Retrospective Look at the Hayek Story: Roundaboutness, Sticky Consumption, and Sequestered Capital” Journal of the History of Economic Thought

[ii] We should not discard Hayek’s triangle entirely. Empirical evidence clearly shows that global manufacturing prospers more and is in greater depth in nations where savings ratios are high than in ones where they are low. The availability of capital is not the only factor, but an important element of this trend.

[iii] Higher interest rates have, of course, attracted deposits, particularly of specie in the days of the gold standard. But this effect today is minimal with relatively little cash, unlikely to be surrendered, and certainly small in quantity compared with the effect on deposits of banks reducing their balance sheets.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.

This article ties Austrian business cycle theory to the cycle of bank credit. It explains how bank credit is created and customer deposits with it through double-entry accounting.

Central bank interest rate suppression has led to the virtual death of bank credit creation for the benefit of non-financial businesses. Instead, banks have grown their balance sheets to finance purely financial activities and speculation to compensate for reduced lending margins.

The cyclical contraction in bank credit is set to be greater than anything we have experienced since the Wall Street Crash of 1929—1932. The authorities’ attempts to defray this reality seems set to undermine the purchasing power of their currencies.

Introduction — the alure of monetary expansion

History is peppered with individuals who see a short-cut to an objective in all fields of human activity. Aesop even had a fable for it: the hare and the tortoise. The field of applied economics is no exception. Before modern times the poster-boy example was John Law, who in October 1715 presented a scheme for a bank “in the name of and for the account of the King” to the Council of Finances at the chateau de Vincennes. Law was inventing the central bank. He had convinced the duc d’Orleans, the Prince Regent, that there was an easy solution to the infant king’s debts inherited from his profligate father, Louis IV —the spendthrift Sun King. He would issue livres for specie and capitalise his bank on Royal debt, bought at a discount but valued at face. The economy would be stimulated, and he would reduce the interest burden on the billets d’état.He was initially denied permission, but the following May Letters Patent were issued to him for a private bank, and Law was in business. The conversion to the Royal Bank — effectively operating in the name of the King — came later. There was no question about Law’s intellectual capacity and his ability to convince. And Law was followed two centuries later by a doppelganger Keynes, who unwittingly adopted the core of Law’s theories, and certainly much of his approach to money and economics.

In the wake of Keynes’s quick fixes, the study of the relationship between credit and business cycles become neglected. Rather than enquire into why a periodic slump occurred it was easier to just assume a cause. Keynes effectively declared that the free market fails because it is flawed. His solution was state intervention to correct it. And when economic aid from the state turned out to be only a temporary fix because the economy slumped again, the original assumption was never questioned: it simply prevailed, and the intervention was repeated, and continues to be by his followers today.

Economists, commentators, and investors are all aware that cyclical factors affect both asset values and economic activity. Some investors swear by their favourite cycles. But in the field of economics, cyclical theory has been primarily associated with the Austrian school of economists, principally in Ludwig von Mises’s writings on trade-cycle theory and Friedrich von Hayek’s triangle. Today, these are collectively referred to as Austrian business cycle theory.

Austrian school explanations of booms and busts added significantly to our understanding and the links with fluctuating credit were examined and understood by both Mises and Hayek. And these cyclical failures are still clearly embedded in our economies. To revive this important subject, we must discard neo-Keynesian economic assumptions and return to basics, adapting and augmenting the Austrian school’s findings for modern times.

Hayek’s take on the business cycle

Hayek was famous for his description of the mechanism by which the regular business cycle occurred. He resorted to using a triangle to illustrate to his students at the London School of Economics the relationships between consumer spending, saving and the consequence for capital investment from changes in interest rates.Hayek used this model to illustrate the effect of interest rates on the rate of savings and the consequences for business calculation, pointing out that capital was released in the form of increased savings by a fall in immediate consumption. It was subsequently explained thus:

“The number of stages of production that can be sustained by the market depends on the time preference of consumers. For instance, a reduction in time-preference increases the supply of loanable funds and reduces the interest rate in the market, other things being constant. This increase in savings allows for extending the triangle by augmenting the financial capital needed to add stages of production. . . The Hayekian triangle offers a simplification of capital theory in order to emphasize particular features such as the effects of market interest rates on how long production takes in an economy.”[i]

There are elements of this statement (which was not Hayek’s) that appear to be on weak ground. For example, the suggestion that a reduction in time preference (in other words, a reduction in interest rates, which in free markets amounts to the same thing without any time lag) increases savings. But surely, a fall in interest rates can be expected to have the opposite effect, diverting savings into consumption. Clearly, for this statement to be correct there must be other factors in play that override an expected supply/demand curve. The explanation is found in bank accounting practices, as will be explained later in this article.

Hayek’s triangle supposed that with increased investment being the consequence of reduced consumer spending, there is a shift in profitability from retail activities towards earlier stages of production. The increase in capital investment from greater savings was directed accordingly. And the reduction in time preference reduced the time penalty incurred for future production. Therefore, more roundabout methods of production became viable.

That manufacturing roundaboutness increased with the capital available was originally proposed by Eugen von Böhm-Bawerk, an earlier economist of the Austrian school, and for a time Austria’s finance minister. The triangle was Hayek’s attempt at explaining the relationship between investment, time and means of production. As an explanation it appears to have begun to be accepted before the economic establishment migrated to Keynesianism following the publication of Keynes’s General Theory, which broadly removed time factors from mainstream economics.

There is much detail to consider behind Hayek’s triangle, but there are contradictions within it to consider as well, and a contradiction in the theory of roundaboutness should be obvious to economists today. It fails to address an obvious fact revealed by modern logistics. Irrespective of changes in savings, by specialising in production improvements can always be expected in the combination of cost, quality and reliability compared with a manufacturer undertaking all the manufacturing processes itself. Therefore, over time the final production of capital goods and consumer durables has increasingly become a process of assembly of pre-manufactured components from diverse sources. This evolutionary process has had little to do with changes in time-preference, and more to do with the advantages of globalisation.[ii] The Hayekian approach also ignores the benefits of scale to a specialist manufacturer making components for a wide range of assembling manufacturers, which would inevitably occur to readers of Adam Smith’s description of a pin manufactory in the first volume of his The Wealth of Nations.

Arguably, a second flaw in this approach is tagging the cycle as one of business activity. Ludwig von Mises described it as a trade cycle. Both descriptions are misleading in the sense that the cycle’s origin lies in bank credit. All economists would have profited by giving greater credence to the practicalities and consequences of bank credit creation in the global banking system that has existed since at least the 1844 Bank Charter Act in English law, and in England from the time of the early goldsmiths in London.

The roots and practicalities of modern banking practice

During the English civil war (1642—1651) goldsmiths took in deposits, paying 6% on the basis that these deposits became debts owed to depositors and therefore the goldsmiths’ own property to deploy and use as they saw fit to generate the promised return. It was from this practice that deposited savings became a bank’s debts owed to depositors (in Roman and English banking law a mutuum as opposed to a depositum), and their role in the expansion of bank credit became firmly established. As can be seen from the Latin, the term bank deposit for customer credit balances is plainly wrong.Theorists assume that higher interest rates towards the end of the credit cycle alter the balance between savings and consumption by attracting more savings and less consumption. That is an error. From a banker’s point of view, higher interest rates are the consequence of increasing lending risk and reflects a desire to reduce the supply of credit. And through the process of double entry book-keeping, a reduction to lending exposure is matched by a reduction to the principal source of balance sheet funding, which is the bank’s liability to depositors. Conversely, lower interest rates reflecting lower lending risk are the result of the banking sector’s desire to expand their loan books, and not as commonly supposed is driven by a surfeit of savings.[iii] This is why bank deposits increase early in the credit cycle, and at this point concurs with Hayek’s triangle; except the origin of deposits is not from consumers’ savings but the expansion of bank credit. The process of deposit creation is explained in more detail below.

It is the practicalities of bank accounting that drive the rise and fall in the quantity of deposits. This is the reverse of what the laws of supply and demand with respect to allocation of savings would suggest. The error is to regard interest rates are the price of money, a mistake that even underlies the monetary policies of central banks.

We can sum up the situation with an iron law of banking:

By lending money into existence, banks create deposits. Therefore, an increase or decrease in overall levels of deposit are not at the savers’ behest, but at that of the banks.

Far more constructive to an understanding of business cycles, in my view, is an approach that gets to their origin and without any doubt that is a cycle of bank credit expansion and contraction. Genuine savings do provide businesses with capital, but that is through direct channels, which may or may not be augmented by bank credit. Why changes in the amount of bank credit lead to a cycle of business activity must form the basis of our inquiry.

The form and impact of periodic credit contractions vary from cycle to cycle, and there are the distortions resulting from state interventions as well. But clearly — except to a hard-line Keynesian perhaps — there is an underlying cycle. And in the study of any cycle, we need a starting point. In anticipating that credit is involved, we must first describe an economic model with a constant quantity of money and credit, and the absence of state intervention as a reference point. And we will also assume that the purchasing power of money overall does not vary much because it is fundamentally sound.

The sound money model economy

In this economy, the community within it acts as both consumers and savers, and through the division of labour the producers among them provide the income for everyone. We must describe it this way to include those who do not produce, such as children, those that rely on others for their sustenance and well-being such as the elderly and infirm, and those whose work is not economically recognised, such as home-workers.The producers evolve themselves into businesses with employees, supplying all the community’s needs and wants as demanded of them. Anything imported, because it either cannot be produced locally, such as raw materials, or is made better elsewhere, can be done so freely on condition that imports are paid for, either covered by exports of the community or by the export of some of the community’s stock of money. In the latter instance, a net export of money will tend to increase its scarcity within the community, thereby reducing domestic production prices relative to those of imported goods. By making exporting more attractive and imports more expensive and a central authority not intervening, a balance between imports and exports is always maintained.

Putting fluctuations in the quantity of money from trade with other communities to one side, the total money received by the producers in investment capital and sales of goods from consumer spending and saving will be unchanged from year to year. What will change continuously is how the flows of money progress, driving up some prices where demand has increased while other prices fall where demand has declined. By their bidding activity for capital funds, entrepreneurs and manufacturers may cause the split between immediate and deferred consumption to fluctuate.

Businesses that fail to achieve adequate profitability or fail entirely, redeploy, or find their resources redeployed for them more profitably. This is Schumpeter’s creative destruction in action. And always, through a process of continual reassessment producers use the means at their disposal to maximise their profits by competing to be the best at satisfying the evolving demands of consumers.

Sound money and the division of labour are together the mainspring of economic progress, the improvement of Man’s condition, and is the basis of free trade between individuals. It was endorsed by classical economists. It requires flexibility in the use of money, its users to set its overall demand and not the state, and it certainly does not need the inflation of credit by a state-sponsored banking system. But that is what we have. Now, we must inject a variation in the quantity of money in the form of bank credit and see how our simple and inherently successful model of a free-market economy based on sound money responds.

How bank credit is expanded

A commercial bank commences business with its own capital and a licence to lend. A representative bank’s balance sheet following its establishment and before trading might look like this.Now let us assume the bank agrees with a customer a loan for 100,000. Does the bank lend its own money? Most probably not — in which case its balance sheet now looks like this.

In the bank’s books, the loan is obviously an asset for the bank. But at the exact time the loan contract is signed, the same customer’s current account is credited with the full amount of the loan. No other party is involved. Of course, the customer’s bank statement might look different, but that is just presentation. What matters are the bank’s own accounts.

But a bank with so little credit exposure compared with its shareholder’s capital is not very profitable. And given that it has been granted a licence to issue credit, it will almost certainly grow its own balance sheet in the search for profits.

Then its balance sheet might look like this.

Again, it must be emphasised that all customer deposits have been created because of loan agreements. Other depositors might open current and deposit accounts, almost always shifting balances from elsewhere in the banking system. And some with credit balances and no loans might close their accounts, shifting the proceeds to other banks. For the sake of our illustration, we shall ignore these activities, which when they lead to net changes are cleared through wholesale markets or a clearing house and have no direct involvement with the credit creation process.

Having increased its balance sheet to 6,000,000, we should note that lending money to customers at an average of, say, 8% becomes the gross margin, because the balancing current account cost the bank nothing. This is the profitable benefit of creating credit by book entry. The bank in our example is now earning a gross income of 400,000 on its loan book. We can further assume its capital is invested in short-term government treasury and commercial bills discounted to give an average annualised yield of, perhaps, four per cent. The bank’s total income at the end of a year’s trading including earnings on its own capital becomes 440,000; a gross return before expenses of 44% on the bank’s capital of one million.

Shorn of unnecessary expenses, it can be seen that bank lending through credit creation is immensely profitable. Admittedly, not all lending works like this. Banks also encourage deposits upon which they pay interest, in the same manner as the goldsmiths in the 1650s referred to above. But these funds can be loaned for even higher margins, such as to credit card holders with uncleared balances and small borrowers’ overdrafts. But for illustrative purposes we shall stick with our focus on a loan book involving larger borrowers.

Business consequences of bank lending

A bank balance sheet ratio of assets to capital of 6:1 is generally regarded as conservative. It will now be obvious that the bulk of money and finance in an economy is bank credit. In the Anglo-Saxon economies of the US and UK this is certainly true due to their low rate of consumer savings, which are funnelled into corporates through new issue markets without bank intermediation beyond off-balance sheet arranging for fees. We can also appreciate that if bankers increasingly view the economy as stable and lending risk as being relatively low, they will grow their balance sheets, gearing up their interest income.Now let us turn to the economic effect. We will assume that a ratio of bank assets to capital of 6:1 is deemed by the banking community to be conservative. In other words, the balance is struck with bankers generally cautious about lending risk, having reduced their balance sheet gearing from higher levels during a preceding business recession. Uppermost in their minds at this point would be the memory of losses from defaulting customers as business conditions turned sour in the recent downturn.

These are the business conditions that promise a return to economic stability. When bankers become increasingly confident that the worst is over, they will begin to cautiously increase their lending again, predominantly to experienced businessmen they have reason to trust. Gradually, backed by bank credit made available to them, these businessmen acquire and reorganise failed and under-performing businesses — evidenced by a pick-up in takeover activity in stock markets usually seen before the economy begins to recover in earnest.

Corporate activity helps drive stockmarkets into recovery, even while unemployment is still high. But gradually, the reorganisation of production by company doctors and the like leads to a pick-up in hiring of skilled labour. The improving environment in financial centres increases professionals’ income, for lawyers, accountants, investment managers and the like. Investment banking becomes immensely profitable from these early-cycle activities, and the spending of those employed in all these specialisations leads to a localised boom for service industries in financial centres, spreading outwards into their commuter belts.

Naturally, the mood infects lending bankers with increasing confidence, realising that their earlier caution is now leading them to miss lending opportunities. They begin to compete with other banks for loan business, focusing on commercial property perhaps, property development and equipment leasing. Competition between banks begins to erode profit margins, and they compensate by expanding their balance sheets even more. Two or three years into the recovery, our sample bank’s balance sheet might look like this:

The bank’s liabilities due to shareholders reflect accumulated profits, net of operating other costs and taxes, after perhaps three years trading into the business recovery. Loan business has doubled. But the asset to equity ratio is now based on the larger figure of shareholders’ funds, leading to a modest increase of balance sheet gearing from 6:1 to 7.25:1.

Competition for loans has led to a reduction in interest charged on new business. Furthermore, our bank is exposed to other banks luring away pre-existing loan business. Therefore, if we assume that the average loan interest rate charged falls from our assumed initial rate of 8% to 5%, then a doubling of customer loans has only generated an extra 100,000 of gross interest income. The bank’s profitability relative to its capital has declined sharply, and with its executives growing increasingly confident of business conditions, the solution is to throw caution to the winds and seek yet more lending business.

Meanwhile, the economic effect of this credit expansion has been to fuel a boom in business conditions, which becomes unsustainable without further credit expansion. In the easing lending conditions, the quality of business borrowers has notably declined. Increasingly, bankers find that conditions in the market for loans have stopped meeting their earlier criteria. Manufacturing costs have begun to rise, there are shortages of skilled labour, and there are growing delays on the delivery of manufacturing and other essential equipment. The cash flows of the weaker borrowers are beginning to reflect the strains.

Initially, these warning signals are ignored in favour of yet more balance sheet gearing. Anyway, a 7.25:1 ratio of balance sheet assets to shareholder funds is still seen as conservative. But with commodity prices and price inflation for consumers now rising, pressure from the foreign exchanges for greater time preference forces the central bank to begin to raise interest rates. Initially, this benefits commercial banks because it puts a floor under loan rates. Commercial banks will continue to increase their asset to equity ratios, further encouraged by recovering lending margins. But in an early warning sign, stock markets begin to weaken under the influence of rising bond yields. A small cloud emerges on the horizon over future loan collateral values.

The economic consequences of the rapid increase in bank credit are embodied in further price increases, from commodities through business services to retail. While full employment guarantees increasing consumer demand, cost pressures reduce manufacturers’ margins. Business failures begin to mount. After eight or nine years of credit expansion, our cohort of bankers suddenly sense the danger of multiple business failures and begin to deny extra credit, beyond what is necessary to prevent existing borrowers from going under. By limiting credit availability, their response leads to a sharp rise in borrowing costs.

Greed for profit rapidly turns into fear of losses. The interest cost of bank borrowing increases for anyone who can get a loan. Banks now desperately want to reduce their balance sheet exposure because balance sheet gearing, of perhaps ten to one at this stage, means that a ten per cent loan write-off across the board renders equity in the bank worthless. The suddenness of the imperative to contain lending risk explains why when it comes the crash is both sudden and indiscriminate.

As mentioned earlier, expanding bank credit to finance production is only one activity pursued by modern banks. But at the core of all activities is financing through the creation of bank credit. A second definition of a banker to the one earlier in this article is that he is “a trader who buys money, or money and debts, by creating other debts”.[iv] Consequently, when conditions turn sour a banker tries to unwind his position as rapidly as possible, having no interest in the fate of the bank’s borrowers beyond what can be recovered from them.

Further implications the credit cycle

We have now seen the true role of banks in the economy as creators of credit. The licence granted to them by the state allows them to issue credit where none had existed before. Initially, it stimulates economic activity and is welcomed. The negative consequences only become apparent later, in the form of a fall in the expanded currency’s purchasing power, initially on the foreign exchanges, in markets for industrial commodities and raw materials, and then in the domestic economy. The seeds for the subsequent downturn having been sown by the earlier expansion of credit, it duly occurs driven by credit contraction. Since the end of the Napoleonic wars, this cycle of credit expansion and contraction has had a regular periodicity of about ten years.A cycle of bank credit is a more relevant description of the origin of periodic booms and slumps than describing them as a trade or business cycle, which implies that the origin is in the behaviour of banking customers rather than the banking system. And trying to fit a cycle of interest rate changes into a cycle of production as Hayek attempted to do requires a deeper understanding of bank accounting than economists normally possess.

The question inevitably arises as to where we might be in the current credit cycle. The last crisis phase can be easily pinpointed to the Lehman collapse in August 2008. Compared with previous cycles, this one’s expansionary phase is now longer than most, assuming it is still running.

Identifying the next credit crisis in retrospect will be obvious. But identifying the end of the expansionary phase has become complicated by other factors. The increasing financialisation of the major economies together with a growing involvement of nearly all governments in their basic economies have altered the emphasis of bank lending away from the business lending of old. Today, the major banks are as likely to create credit to finance their own trading activities. And the proportion of bank credit that goes to finance portfolios of government and other securities has also increased. But even allowing for these factors, the FRED chart below shows that commercial lending peaked in May last year after initial covid-related distortions. Adjusted by the increase of credit in the economy (money M2 has increased by 36% during the time covered in the chart) the contraction of bank lending in the economic context is even greater than the chart suggests.

A further important factor has been increasing intervention in asset markets by central banks. The Fed, the Bank of Japan, the European Central Bank, and the Bank of England all invest directly or indirectly through quantitative easing and like measures to ensure financial assets maintain and increase in value. For now, at least, this has removed the risk of falling collateral values which is traditionally associated with a collapse in bank lending. And by nailing interest rates at the zero bound, the evidence of higher interest rates emerging due to pressure from banks to curtail their lending has been supressed.

Consequently, evidence of the end of the cycle of bank credit is barely noticeable, not only to observers but to bankers as well. But bank lending probably ran into an end of cycle crisis in September 2019, when the repo market blew up — eleven years after the Lehman failure. That being the case, the cycle’s duration would have been similar to earlier ones.

The ending of it, if that was what the repo crisis indicated, was not evidenced by bankers calling time on lending. Rather, it appears that larger banks active in financial markets collectively ran out of balance sheet capacity. Bankers had also behaved differently ahead of the Lehman crisis, failing to anticipate the events that led to the whole banking system needing to be rescued, instead of precipitating the collapse by their own actions. Something has changed their end-of-cycle behaviour, which is our final topic.

The consequences of monetary policies for banks and currencies

In our illustrations of the accounting mechanism whereby bank credit is produced, banks through competition with each other set borrowing costs for businesses. One can argue that so long as official rates are not too far removed from market rates the supply and demand for credit allows this process to continue. But in recent decades, central banks have gradually reduced official interest rates to zero and even into negative values.This has not entirely stopped the process of credit creation for non-financial businesses. But creditworthy borrowers have access to capital markets as well, and with central banks suppressing bond yields through quantitative easing, for banks the risks of lending to business customers are significantly greater than the interest rate compensation. This leaves banks lending to businesses that don’t have access to capital markets, which they are generally reluctant to do.

In effect, while monetary policy is implemented to stimulate the economy, it is strangling bank lending. The implications should not be dismissed lightly, because most money in circulation owes its origin to credit owed to depositors and its maintenance depends on banks not contracting their balance sheets.

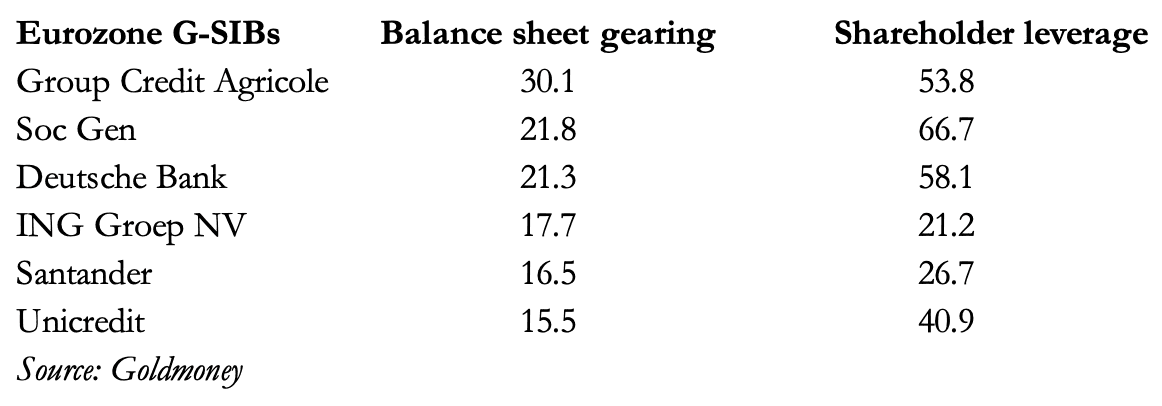

Nowhere is this problem more evident than in the Eurozone, where in some jurisdictions lending to businesses appears to have almost ceased.[v] In common with banks elsewhere, Eurozone banks have turned to other activities, notably expanding credit to finance burgeoning state debt. And to maintain nominal profits in a negative interest rate environment, they have expanded the ratio between assets and equity to record levels.

The usual top-of-lending-cycle balance sheet gearing between assets and equity is in the region of ten, perhaps twelve times — enough to precipitate a major lending contraction in earlier times. Yet here we see major banks (the Eurozone’s globally important banks — the G-SIBs) with ratios of up to thirty times. The reason they have become so high is a combination of regulatory bias determining risk weightings in favour of sovereign debt, the interest rate environment imposed by the ECB and funding of speculation in securities markets replacing conventional bank lending. While the European Banking Authority takes the view these banks are solvent, their shareholders appear to believe otherwise, evidenced by their market capitalisation being below book values in all cases, illustrated by the column on shareholder leverage.

Clearly, bank lending to businesses in all major jurisdictions is being restricted by central bank interest rate policies. The focus of bank credit creation has shifted from providing finance to businesses, to low-margin financing of ever-increasing government deficits as well as financial speculation. In the case of the Eurozone, statist debt levels for Spain, Italy, Portugal, and even France have now spun out of control, accelerated by Covid and the availability of bank credit to buy their bonds.

There are two identifiable systemic threats emerging. The first is that the expansion of central bank money will be needed to replace bank credit when it ceases to expand and reverses — and history says that at some point it will. And the second threat is associated with monetary inflation, which is the effect on fiat currencies’ purchasing power. For the moment, the timing of the former is up in the air. But we can already see how rising prices, which are the evidence of the falling purchasing power of fiat currencies, are going to drive interest rates higher. Higher interest rates mean falling bond prices and the end of the stock market bubble. They also mean accumulating losses on bonds bought by the banks, and the loss of collateral value held against loans to business customers and stock market speculators.

For the moment, central banks are united in denying the interest rate threat. But increasingly, market actors are beginning to understand its reality. When they act, we are likely to see a market crash on the lines of John Law’s Mississippi bubble. The global unwinding of credit will then become a panic impossible to stop. We will almost certainly see interest rates rising to reflect the banks’ struggle to reduce their balance sheets to more normal levels relative to their shareholders’ capital.

Finally, we should take note that the monetary authorities will have no option but to attempt to replace contracting bank credit with their own form of credit — promises to pay nothing but folding paper in the form of fiat currency. The quantities required will almost certainly be proportionately far greater than the open cheques written by central banks to save the financial system following Lehman. This time, with G-SIB balance sheets to equity ratios on my estimation in the EU arithmetically averaging 20.5, the UK’s at 16.8, Japan’s 21.4, China’s 13.6, and the US at 11.2 times, the contraction of bank credit back to levels more normal for the beginning of a bank credit cycle will almost certainly be more financially violent than anything seen since the Wall Street Crash of 1929—1932.

The evaporation of collateral values will almost certainly be seen by policy planners as central to the collapse in bank credit, so central bankers’ instincts will be to accelerate their support for bonds and equity prices, while maintaining the availability of cheap mortgage finance to stop property prices imploding. Expect official interest rate rises to be reluctant and less than required to stabilise currencies. Expect the Fed’s QE to escalate from $120bn a month and other major central banks to act similarly.

Earlier it was noted that the vast bulk of money in circulation has its origin in bank credit. The task of replacing it with central bank fiat currency seems set to destroy the purchasing power of the currencies, which coincidently was what happened to John Law’s livres 301 years ago. Courtesy of his successor in stimulus policies, Lord Keynes, the same outcome faces economies today on a global scale. It is increasingly impossible to see any other outcome from the development of the current situation.

[i] As quoted from in McClure, James E, David Chandler Thomas, and Lee C. Spector. “A Retrospective Look at the Hayek Story: Roundaboutness, Sticky Consumption, and Sequestered Capital” Journal of the History of Economic Thought

[ii] We should not discard Hayek’s triangle entirely. Empirical evidence clearly shows that global manufacturing prospers more and is in greater depth in nations where savings ratios are high than in ones where they are low. The availability of capital is not the only factor, but an important element of this trend.

[iii] Higher interest rates have, of course, attracted deposits, particularly of specie in the days of the gold standard. But this effect today is minimal with relatively little cash, unlikely to be surrendered, and certainly small in quantity compared with the effect on deposits of banks reducing their balance sheets.

[iv] See page 148, The Elements of Banking by Henry Dunning Macleod, published by Longmans in 1877.

[v] Evidence for lack of bank credit expansion for the benefit of businesses is reflected in low expectations for GDP growth in a number of EU jurisdictions, particularly amongst the PIGS.

[v] Evidence for lack of bank credit expansion for the benefit of businesses is reflected in low expectations for GDP growth in a number of EU jurisdictions, particularly amongst the PIGS.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.