Start of a recovery?

Mar 3, 2023·Alasdair Macleod

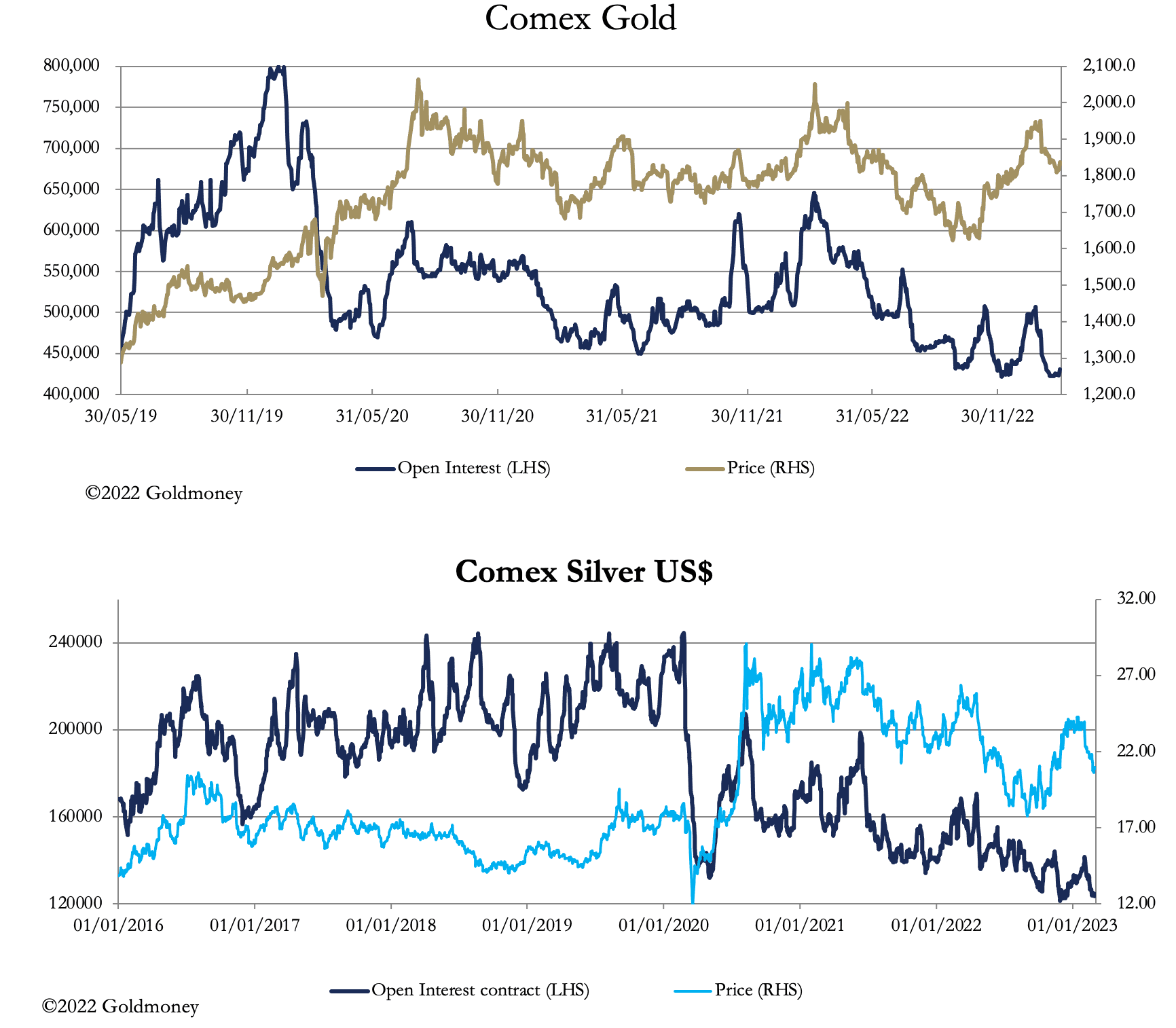

After declining recently, gold and silver steadied this week in oversold conditions. This morning in European trade gold was $1847, up $37 from last Friday’s close, and silver was $21.10, up 50 cents. Turnover on Comex has been low in both contracts.

We still lack Commitment of Traders Reports following the ransomware attack on ION, one of the software providers used to submit data. The last report was for 31 January. There is no way of knowing how many traders own systems have been breached by the Russian ransomware attacker through ION. But if the attack has not only accessed data but trading systems, there is no knowing how much damage there is to paper markets and disruption yet to be caused.

With respect to gold and silver, all we know is that physical is still being stood for delivery. 5.9 tonnes of gold are stood for delivery so far this week, bringing the total to 94.5 tonnes this year. And in silver, the figures are 399.4 tonnes this week, and 1,370.3 tonnes respectively. Note that silver deliveries this week have been particularly heavy in a market where there is little physical available.

Furthermore, according to the World Gold Council, central banks added a further 31 tonnes to their gold in January. And other reports are of significant premiums on the Shanghai Gold Exchange over the paper gold price on Comex.

The next chart shows how oversold these two contracts have become.

If we had COT figures, they would probably show the Managed Money category net short in both contracts, setting them up for a decent bear squeeze.

But in the background, there are big-picture changes in progress. Bond yields are on the rise again, disappointing those looking for a policy pivot from the Fed. The next chart is of the 1-year UST bond.

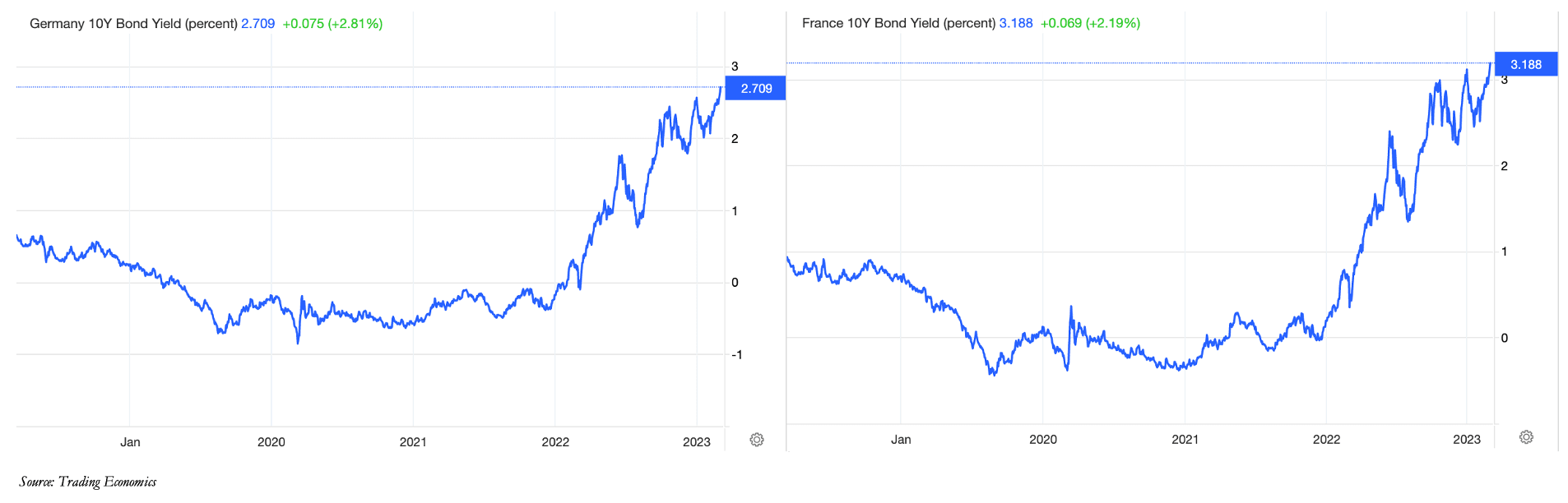

And this is not the only bond market saying goodbye to a pivot and lower interest rates. The next chart is of the two major European 10-year bonds — Germany and France.

That these bond yields are now hitting new highs is significant. Spanish bond yields are also hitting new highs, and the 0.5% cap on Japan’s 10-year JGB has been breached for the last three trading sessions.

Many traders would see higher bond yields as bad fo gold, which is probably why the Managed Money category has sold out of gold and silver. But interestingly, this trend is beginning to be challenged with gold prices rising this week with bond yields.

Doubtless, there will come a point where the interest rate differential narrative will give way to an understanding that the higher bond yields and interest rates rise, the more destabilising they will become. Today, Credit Suisse’s share price hit new lows (CHF2.66) on news that they are being forced to offer higher interest rates to stop a run on deposits.

The message is clear: rising interest rates and bond yields are beginning to threaten a banking crisis. Gold is the safe haven.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.