Rebutting Matt O'Brien's and the Washington Post's Misguided Attack on Gold

Apr 1, 2016·Stefan WielerRebutting Matt Obriens and the Washington Post's Misguided Attack on Gold

It is our mission to rebut any mainstream article that spreads misinformation about gold and/or shows a gross misunderstanding of monetary history. In Matt O’Brien’s “Wonkblog” in the Washington Post on February 23, 2016, titled “This might be Ted Cruz’s worst idea“, he does both. The ‘worst idea’ in this case refers to the Texas Senator’s view that it would be to the benefit of the US economy to return to a gold standard. One of O’Brien’s main arguments against the gold standard, aside from his claim that apparently nobody on the “University of Chicago's ideologically diverse expert panel” thinks it a good idea, is that he believes goods and services priced in gold are more volatile than goods priced in US dollars and, behold, sometimes prices can even decline substantially.

source: Washington Post

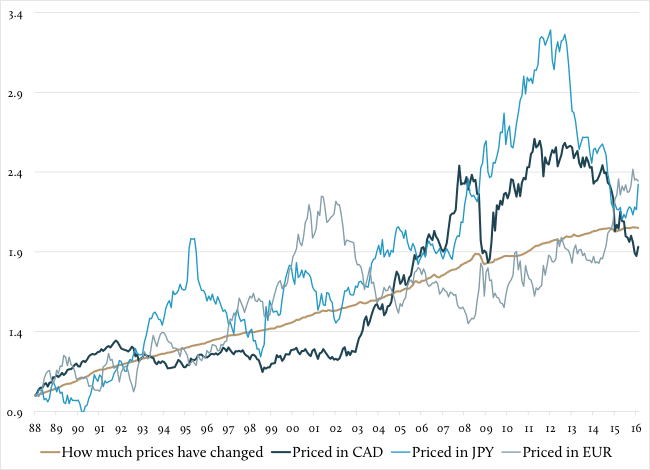

Obviously what O’Brien completely omits is that under a gold standard, the dollar and gold are one and the same. With the same argument, O’Brien could have shown that prices for US goods and services have been even more volatile when measured in euros, Canadian dollars or Japanese yen, and then conclude that euros, Canadian dollars and yen are much too volatile to be used as money (see Figure 1). Needless to say, more than 500 million people use those currencies every day. If gold would have been the official currency of the United States since 1988, the price chart would have looked just as smooth, with the difference that it would not be pointing up but it would be simply a flat horizontal line, pretty much the way it was before 1971.

This is a simple point not hard to understand. Anyone who has spent a little bit of time studying currencies, gold and economic principles in general understands it.

US goods measured in foreign currency are much more volatile than in USD (or gold for that matter). It doesn’t mean much, which is why normally nobody would bother showing such a chart.

source: Bloomberg, GoldMoney

source: Bloomberg, GoldMoney

Let us ignore all that for a moment and assume that for the past 30 years prices for US goods and services under a gold standard would have indeed moved the way in which they did when measured in gold. This reveals another flaw in O’Brien’s tirade against gold. He claims that:

“After all, it's not like the price of gold matters to a middle-class family. It has nothing to do with the price of food or housing or education or anything else that anyone who isn't preparing for the end of the world would need.”

That is simply just plain wrong. O’Brien tries to prove his point of view in his chart shown above that supposedly represents how prices changed since 1988 (a completely arbitrary starting point) and how they would have changed under a gold standard. As source he quotes the St. Louis Fed’s FRED database, but it doesn’t say what the data actually show. One can only assume the creator of the chart used the CPI deflator and overlaid it with the gold price. The problem is, that doesn’t really reflect – to use Matt O’Brien’s own words – “what matters to a middle class family.” This is because the CPI (and not gold) seems to have actually quite little if not exactly “nothing to do with the price of food, or housing or education or anything else to anyone”. So let’s look at how prices for goods and services that are of particular relevance for the middle class would have changed in gold. And we shall use O’Brien’s arbitrary starting point of 1988 (and not the end of the gold standard in 1971 which would have made sense or simply the end of the 20th century or anything else more intuitive than 1988. 1988 could well be coincidentally most likely the mathematically best starting point to support his flawed argument).

Let’s start with energy. O’Brien doesn’t specifically mention energy even though it certainly matters for a middle class family. According to the US Energy Information Agency (EIA), 3.2 billion barrels of gasoline were consumed each year in the United States on average during the past five years. At an average price of USD3.30/gal, this equates to roughly USD1,400 per person (including every child and retiree). But that is only half the bill, as total US crude oil consumption is roughly seven billion barrels per year. This doesn’t mean that an average household of four outright spends USD10,000 on fuel, because a lot of fuel is consumed by company cars, trucks and other commercial vehicles and machines. But in the end, those commercial costs drive the costs of products and services consumed as well. Add bus tickets and airfares and the houses in the northeast that rely on heating oil in the winter and you understand that crude oil costs account for a large share of consumer expenditures, both directly and indirectly. Overall, the US has spent roughly 6% of its GDP on crude oil over the past five years. It clearly matters for the average middle-class family. The chart below shows retail gasoline prices including taxes. As one can see, gasoline prices tend to be somewhat less volatile when priced in gold. This becomes even more evident if the time horizon is extended back to the end of the gold standard in 1971. (For those who are interested in finding out why, you can read our gold price framework report here.)

Prices for petroleum products are somewhat less volatile when measured in gold

source: Bloomberg, Energy Information Administration, GoldMoney

source: Bloomberg, Energy Information Administration, GoldMoney

But maybe oil is the outlier, and O’Brien is right when it comes to other important consumption goods? Well let’s look at food then, because every middle class family needs food. The Economist magazine publishes the price of a BigMac Burger for different countries in their BigMac index. The idea is to compare the purchasing power of different countries’ currencies. But this also a great tool to compare how food prices have changed over time. After all the Big Mac is a staple, served the same anywhere in the US, a commodity that really didn’t change much since 1988, which makes it perfect for our comparison. This chart looks a bit different. Prices do rise a bit when measured in gold between 1995-2000, but are nowhere near as volatile as O’Brien’s chart suggests. Then prices come down and eventually they end up slightly below where they started in 1988.

This is nothing but a continuation of a trend that has been present in human history for hundreds of years. It shows that society is able to push the boundaries of scarcity with technological progress. Think of how many calories per day the average American was able to purchase in 1800, in 1900, and how that has improved until 1950. It is a good thing that the average American no longer has to spend half of his daily income for food as it was in the past. Does it make sense to be afraid that expectations of declining food prices will lead to lower aggregate demand because people will push the purchase of food to a future date? Of course not. Is it a problem when the average American has to spend a larger share of his disposable income for food? It certainly is. The price of a BigMac has increased by 101% in dollar terms since 1988. In comparison, the median household income has only increased by 97%. It might not look like much, but this runs completely contrary to the upward trend in prosperity consumers enjoyed over the previous 200 years, during most of which the US dollar was pegged to gold (or silver).

Even as the Price for a BigMac has risen faster than pretax household disposable income, the price for a BigMac measured in gold is slightly below the price in 1988

source: The Economist BigMac Index, Bloomberg, GoldMoney

source: The Economist BigMac Index, Bloomberg, GoldMoney

Falling prices (ie deflation) are the boogeyman of today’s mainstream economic doctrines. The conventional wisdom is that it was deflation that pushed the US economy from a normal recession into the great depression in the early 1930s. If consumers expect the price for a good to be lower in the future, so the argument goes, they will delay the purchase, which in turn will lower aggregate demand, deepen the recession and possibly turn in into a prolonged depression. Hence, price deflation has to be avoided at all costs. While this might make some sense, consumers don’t always behave the way economist believe they should. Take the iPhone for example. One can be sure that a year from now there is a new model, and the current model will sell for half the price. Yet people can’t seem to get enough of the newest one. Indeed, falling prices for computers and most electronic goods have been the norm for years and yet sales continue to rise.

Fact is, falling prices are for most people a good thing. After decades of stagnating real wage growth, lower prices are welcomed by the majority of US consumers. And despite the claims of mainstream economists that there is strong link between deflation and depression, historical data seems to prove otherwise. In a 2004 research report for the National Bureau of Economics, UCLA’s Andrew Atkeson and Patrick Kehoe from the Research Department of the Federal Reserve Bank of Minneapolis analyzed economic data over a period of more than 100 years for 17 countries and found that “the only episode in which we find evidence of a link between deflation and depression is the Great Depression (1929—34). But in the rest of the data for 17 countries and more than 100 years, there is virtually no evidence of such a link.” It seems deflation doesn’t automatically lead to a recession or even a depression, and even in regards to the great depression, Austrian School economists would argue that Keynesian economists confuse cause and effect, that deflation was primarily the result of the recession, rather than the other way round.

O’Brien also brings up housing as an important part of the costs for a middle class family and we are happy to cover that as well. Housing differs from a consumer good in the sense that you don’t buy a house every day. You start saving for a house and save over a very long time period until you have saved enough to make the purchase, or at least the down payment. Hence volatility in prices month-to-month are less of a concern. What really matters is how long you have to save to buy the house (or pay it off if you finance it). Inflation is a real problem however. If you put USD1,000 aside and 20 years later the purchasing power of that USD1,000 is cut in half, it will become a Sisyphean task to save enough money to buy a house.

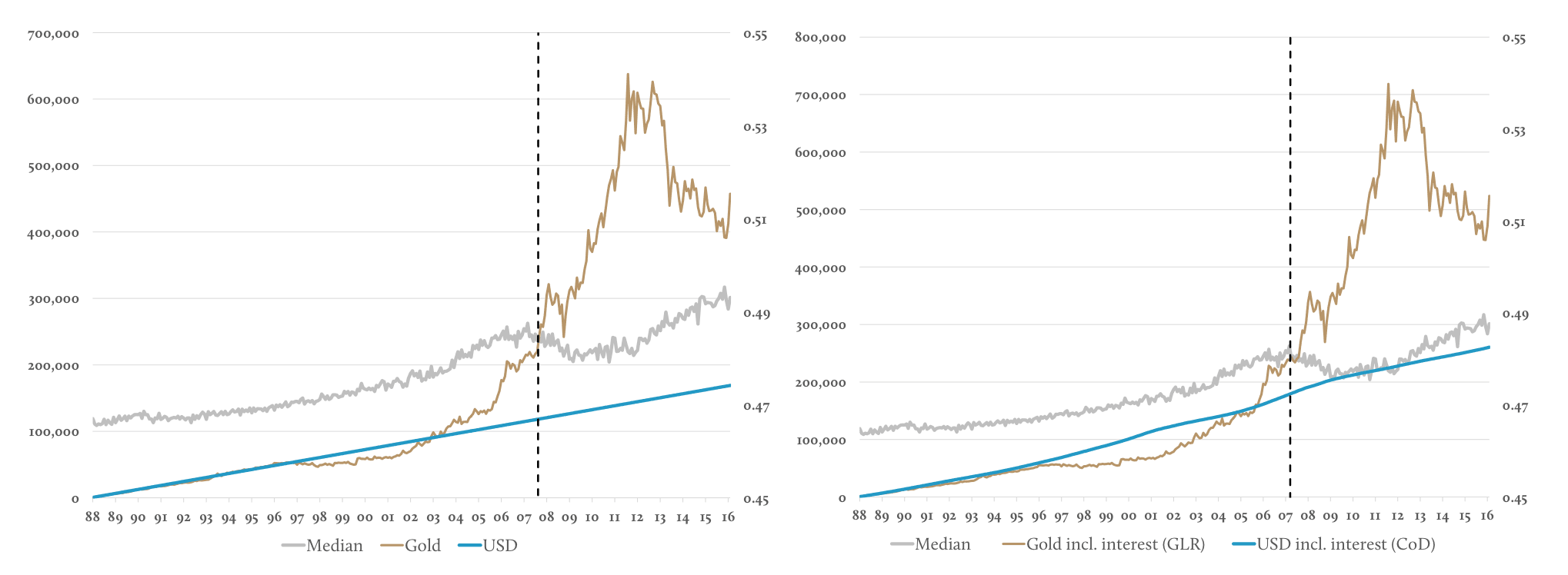

Imagine a young worker had just entered the workforce in 1988. His dream is to buy a house one day. For that he puts USD250 aside at the end of every month. He thinks he can get a mortgage and the bank will lend him 50% of the value of the house when the time comes. He has now two choices: he can save in US dollars, or he can save in gold. The below chart shows how long he has to save to achieve his goal. If the had decided to make his savings in gold in 1988, it would have taken him a bit under 20 years to accumulate enough wealth. But had he decided to save in US dollars, house prices would have risen too fast for him to ever reach his goal. By 2007 (the time he was able to buy the house was he smart enough to save in gold), property prices had risen 102% in US dollar terms according to data from the US census bureau. That means the first USD250 he saved in 1988 had lost 50% of its purchasing power. In contrast, the average house in 1988 cost about 10kg of gold and by the time our house buyer was able to afford the house in 2007, it had risen to only 10.6kg. Hence the first gram he put aside in 1988 still bought him roughly the same amount of house.

Now these calculation above ignore bank interest and you will argue that he would have been stupid to save his dollars by storing them under his mattress. Surely the interest earned from his money would have been enough to offset the loss in purchasing power? Think again. We used the 12 month deposit rate and even though in theory there was a brief moment where he actually would have been able to purchase the house, it would have been a bold move right into the crashing housing market, and it was probably not that easy to get a mortgage at the time.

As house prices rise fast, saving for a home becomes a Sisyphean task. Saving in gold has proven to be much more efficient

source: US Census Bureau, Bloomberg, GoldMoney

source: US Census Bureau, Bloomberg, GoldMoney

The Gold Standard as it existed prior to 1971 certainly had its flaws. But nothing of what Matt O’Brien wants to make us believe is one of them. The main flaw in the gold "standard" to which O'Brien and the ”ideologically diverse panel of economists” refer was that it was fractionalized via a central bank rather than being fully-reserved. People must remember that even though gold as base money is superior to fiat, the gold standard of the 1920's was still flawed as the gold was held as base money by the Central Bank and the Commercial Banks were able to extend or fractionalize that base money as commercially circulating money at a factor of 6-8 times. Therefore, instead of actually owning and using gold, citizens owned a fraction of a base of gold depending on the ebbs and flow, booms and busts in the economy and business cycle. As we know, a particularly large bust took place in 1929-1932 and the US banking system, being only fractionally reserved, became subject to a bank run and many banks thus failed.

Before the central bank model was introduced in the US in 1914, the commercial banks themselves were also generally only fractionally-reserved. That was a recipe for occasional financial instability, known at the time as “Panics”. That stands in sharp contrast to the gold standard we promote at GoldMoney Inc.: one that is fully reserved and decentralized as there is no central controlling entity extending or contracting credit against the gold. Rather, in our gold standard framework, decentralized actors such as ourselves would use their fully reserved gold to engage in commerce, trade, and productive activities. Extending credit would be left to other institutions inclined to take such risk and, of course, subject themselves to the risk of default or failure. But under this framework the failure of credit institutions would not threaten the broader financial system, the money itself—gold—or the economy more generally. There would be no such thing as “Too Big To Fail”, as it were.

Together with our sister company BitGold, we allow everybody to own physical gold stored under their own name and use it for transactions, down to 0.03cts. It’s our customers’ gold. It’s not a promise of future delivery, ownership in an obscure financial vehicle that owns gold or some sort of token that represents gold. It’s your gold, which nobody can encumber or debase.

The gold standard was an effective way to combine the proven superiority of gold as base money with the utility of paper currency for transactions (e.g. small denominations, ease of exchange, efficiency etc.). To transact in actual gold coin, especially for smaller transactions, was simply not practical at the time. But technology now enables us to overcome all of that and to use gold not only as a monetary reserve for circulating currency but as actual, transactional money. In 2016, gold is now as easy and efficient to use for transactions as the dollar or other major currencies are. In fact, it is actually more efficient: In what other currency can you transfer one dollar of value within seconds from any point on the planet to another with no costs occurring or no need to create or extend credit?

The technology now exists to save, transfer, remit, redeem and otherwise conduct one’s personal business and financial activities in gold. Hence, whether governments decide to go back to a formal gold standard or not someday, people already have the choice. So what do you say Mr O’Brien? Why not join our 800,000+ and rapidly growing gold client base, now spread over 100 countries? Something tells us that they are substantially more “ideologically diverse” than that panel of “experts” who are telling them that they are wrong.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of GoldMoney, unless expressly stated. The article is for general information purposes only and does not constitute either GoldMoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, GoldMoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. GoldMoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.