Market Report: Q1 gold demand 1,290 tonnes - WGC

May 13, 2016·Alasdair Macleod

Yesterday, the World Gold Council released its estimate of gold demand for the first quarter of 2016, which compared with supply estimated at 1,081 tonnes.

While the WGC collects its figures assiduously, the demand figures are only those that are known from trade associations, central banks, and ETFs. Drilling down into the figures, according to the WGC, Chinese demand for the quarter totalled 241.3 tonnes, whereas according to the Shanghai Gold Exchange, it delivered 516 tonnes to the public from its vaults. The substantial difference cannot be satisfactorily identified as far as the WGC is concerned, but this illustrates the difficulties in tracking down accurate figures.

One category that is easy to identify is ETF demand for physical metal, and this increased to 364 tonnes, the highest net inflow since 2009. There can be little doubt this is down to two factors: the improved technical position with the establishment of a new bull phase, and negative interest rates in both the euro and the yen. But while this has spurred demand for securitised gold, there is no such increase recorded in demand for bars and coin. That cannot be right. Physical demand must be considerably higher than the WGC figures reflect.

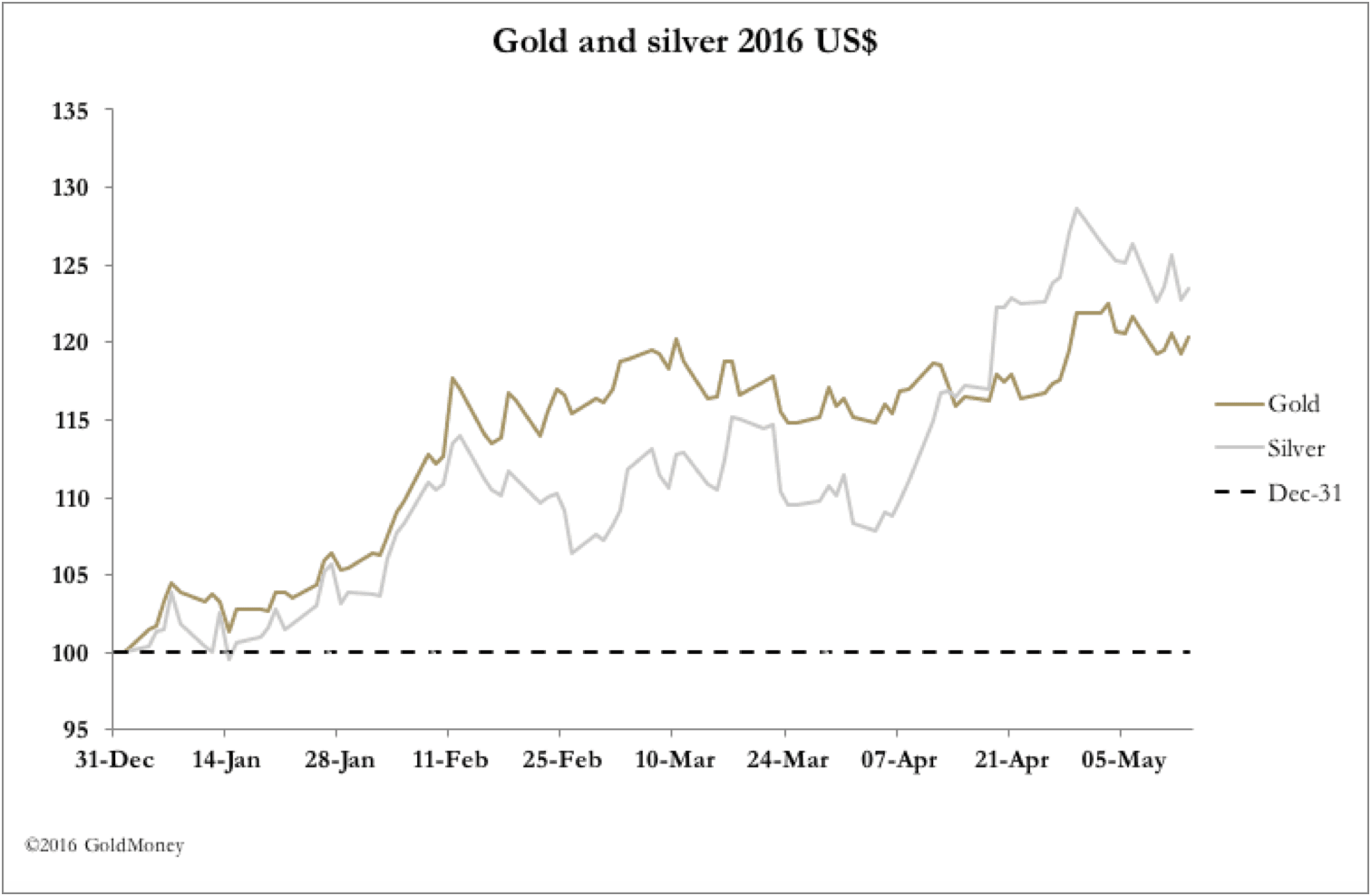

On futures markets the gold price fell on Monday from last Friday’s close of $1287, hitting a low point of $1257 on Tuesday. A rally took the price back up to $1280 at one stage yesterday, before slipping back to $1263 last night. However, in early trade this morning gold and silver opened higher at $1274 and $17.09 respectively in early European trade.

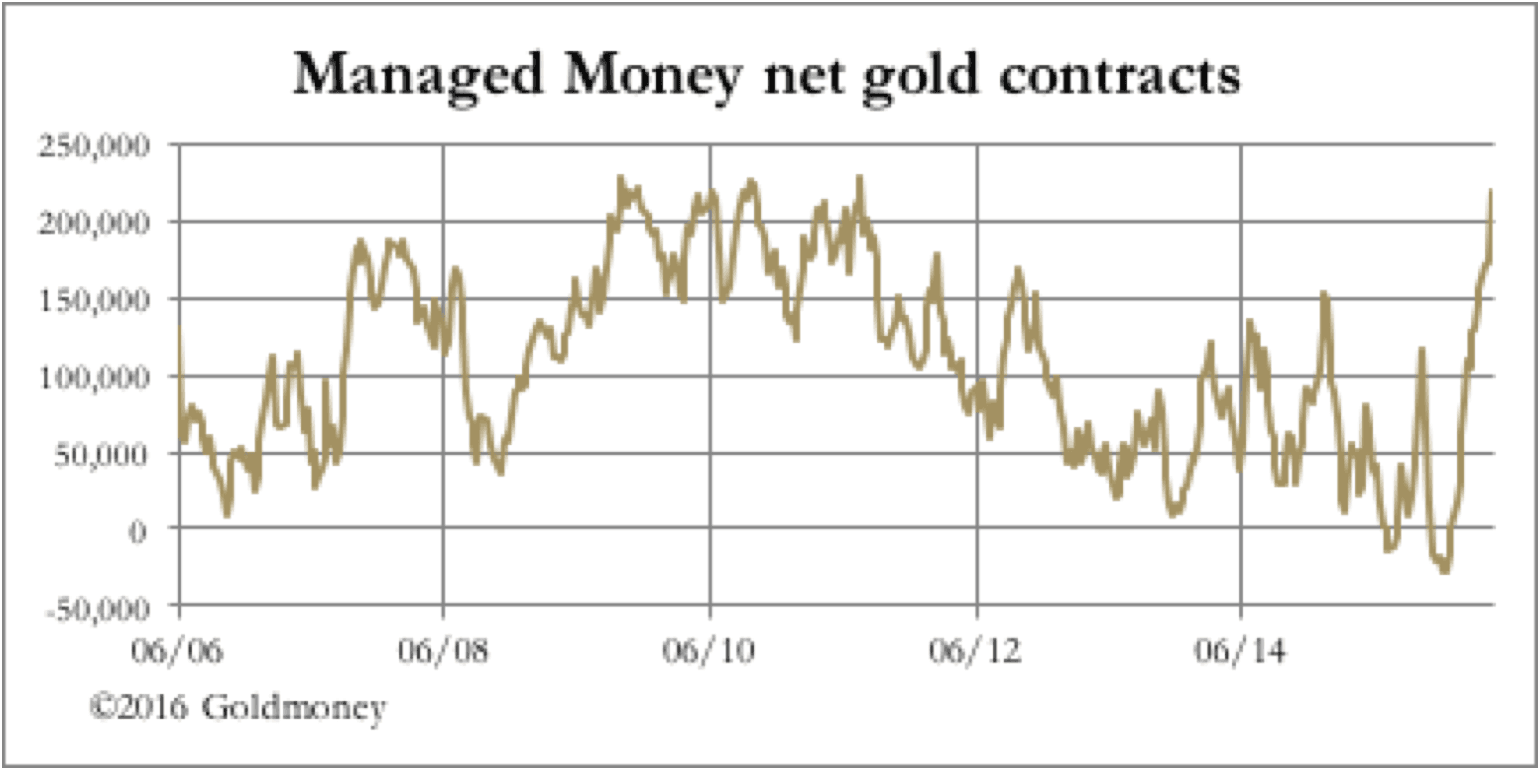

Gold had become very overbought, with the Managed Money category noticeably long, as the next chart shows.

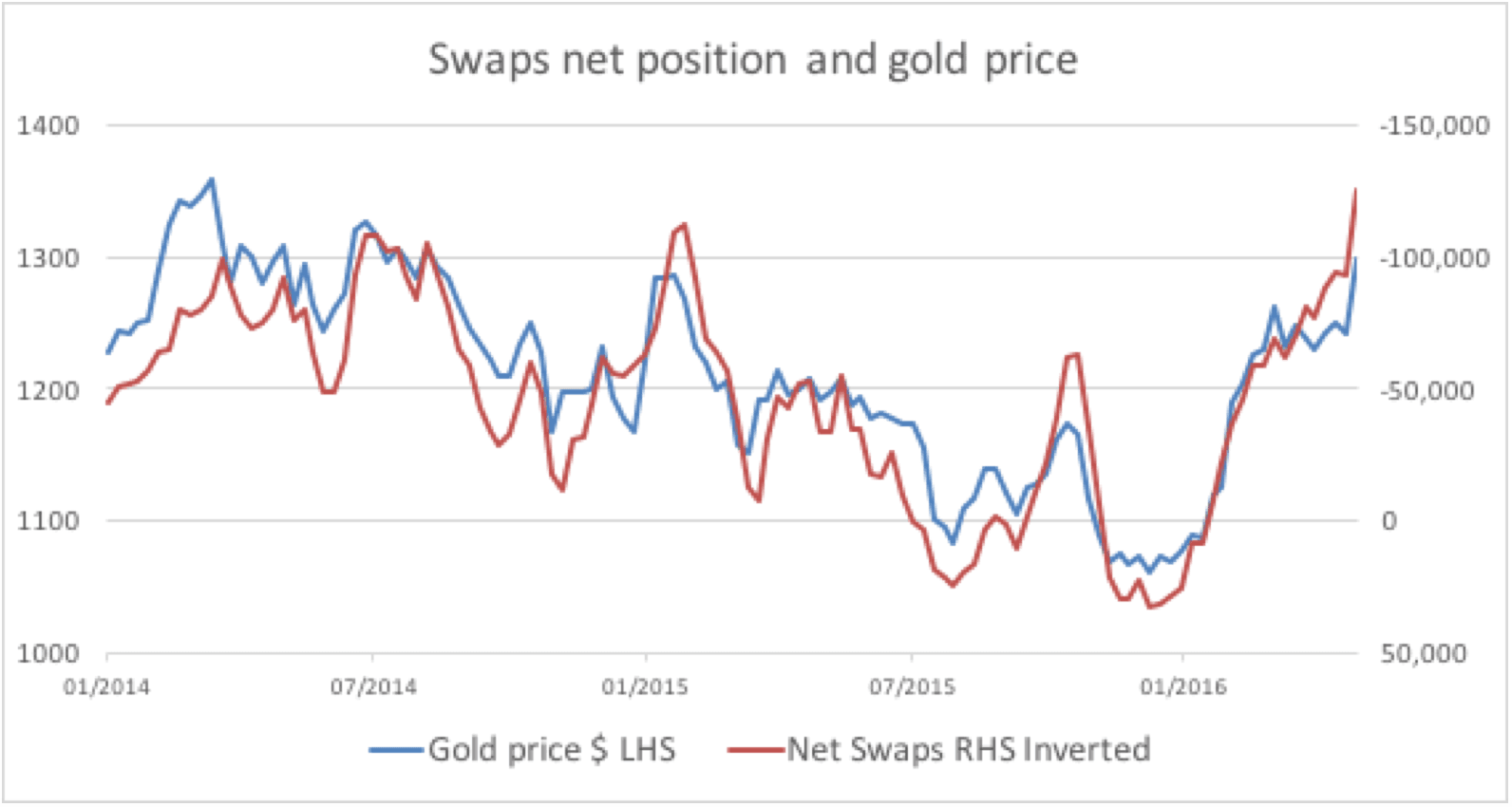

Net contracts stood at a positive 218,895 contracts, within 10,000 contracts of the all-time high. Meanwhile, Open Interest is also very high at 585,890 contracts, and the swaps (mostly second-line bullion banks) are record short at -124,993. The correlation of the swaps net position with the gold price has been almost perfect for the last two years. This is shown in our next chart.

At some point this correlation must cease. Either the swaps will be forced to turn net buyers, or they will conquer the speculators (mainly hedge funds). If it was as simple as that the hedge funds will be wiped out. But hedge funds usually see gold as one side of a trade, with the risk exposure to the gold price partly or wholly hedged. That is why they are called hedge funds.

The involvement of hedge funds is therefore part of a bigger macro picture, linking trades to wider risk-on/risk-off positioning. There is little doubt that the hedge fund community is betting on greater risk in the future, with notable fund managers short of bonds and equities. It is reminiscent of the film, The Big Short, where some big bets were placed against asset-backed securities and collateralised debt obligations. It has become an argument of right or wrong, rather than overbought/oversold.

Meanwhile, in Europe the volcano that is the Italian banking crisis is in danger of erupting, which could play into the risk-on crowd.

The views and opinions expressed in the article are those of the author and do not necessarily reflect those of GoldMoney, unless expressly stated. Please note that neither GoldMoney nor any of its representatives provide financial, legal, tax, investment or other advice. Such advice should be sought form an independent regulated person or body who is suitably qualified to do so. Any information provided in this article is provided solely as general market commentary and does not constitute advice. GoldMoney will not accept liability for any loss or damage, which may arise directly or indirectly from your use of or reliance on such information.