Precious metals squeeze intensifies

Dec 26, 2025·Alasdair MacleodThe squeeze in silver is now creating headlines in the media. If this leads to a wider recognition of why silver continues to rise, it could spark additional ETF demand.

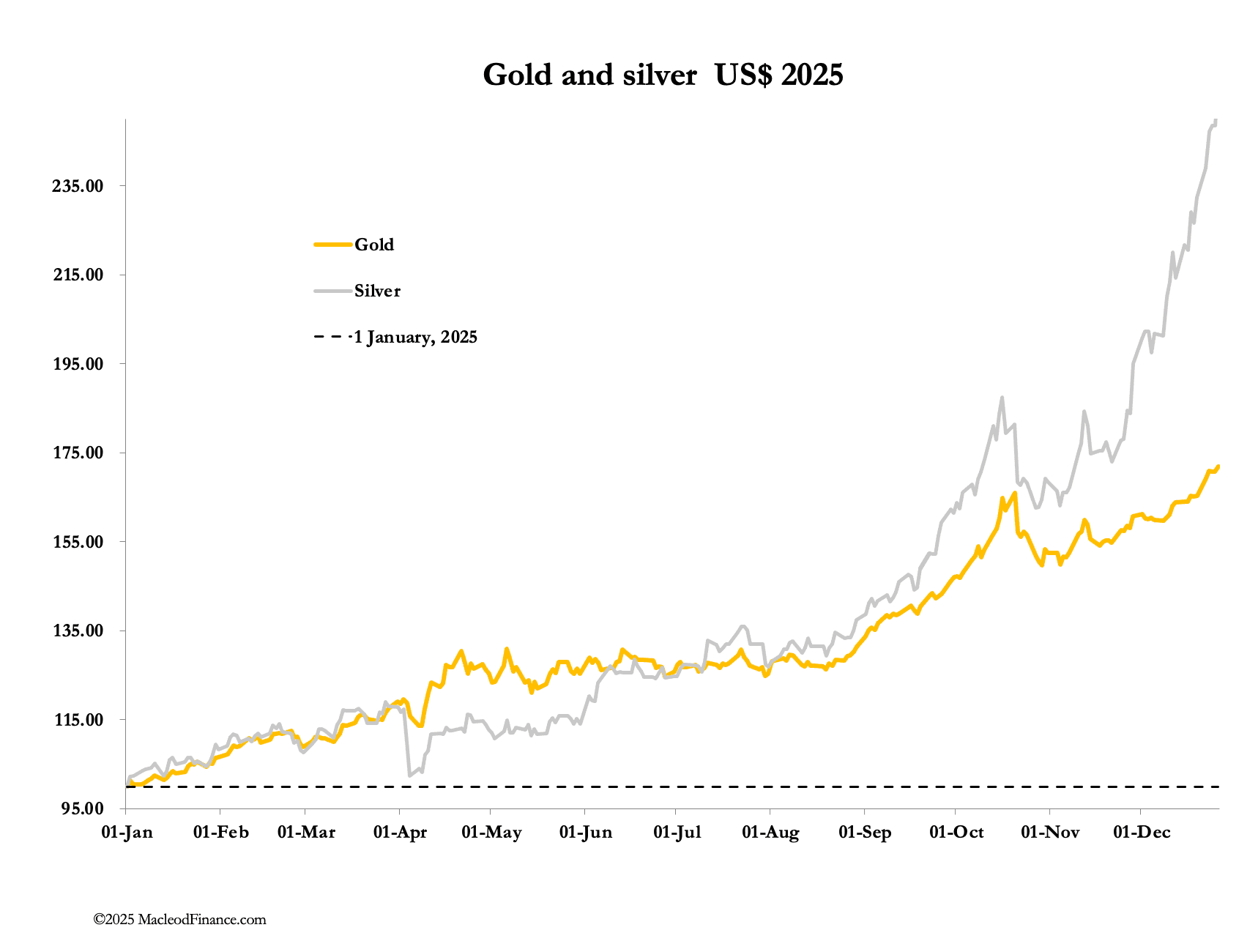

Christmas week has been particularly dramatic for silver and platinum, marginally less so for palladium while gold quietly sails into new unchartered territory. Our headline chart below says it all…

Christmas week appears to have intensified the squeeze on silver and platinum, with dramatic moves higher in Shanghai, silver even challenging the $80 level at one point last night. In European trade this morning, silver was $74.80, up $7.80 from last Friday’s close, and gold at $4518 was up $187 over the same timescale. Predictably in a holiday week with London closed yesterday and today (Boxing Day holiday), Comex volumes were light.

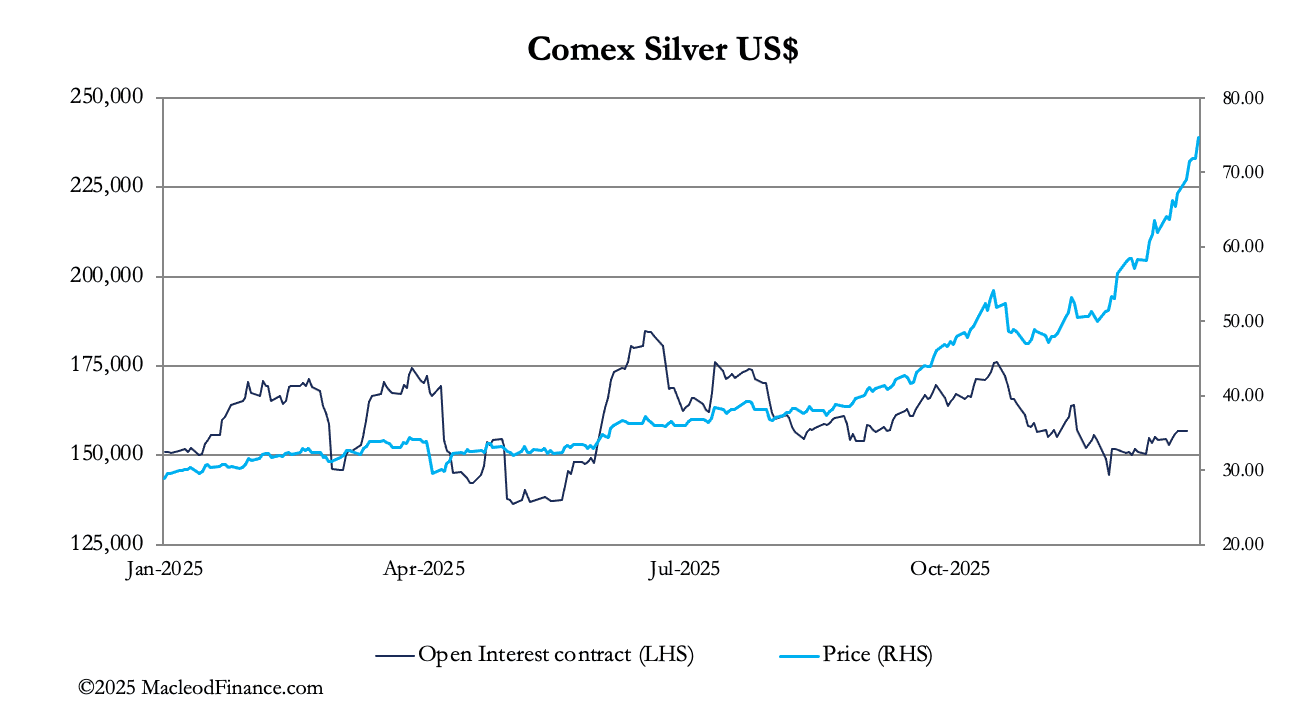

Our favourite chart of silver and Comex open interest illustrates how little speculator participation there is in this rally:

The entire rally from 13 November has seen a decline in open interest while the price rose 50% from $50, evidencing the severity of the squeeze on the shorts. Inevitably, genuine producers are no longer hedging for fear of being called, increasingly throwing the short burden on the bullion banks in the swaps category. At the same time, speculator interest is remarkably subdued, likely to become an additional problem for the shorts if and when they join the party.

The background of gold gently moving into new high ground is an additional problem for silver, because of the signal it sends. Meanwhile, stand-for-deliveries continue apace, totalling 14,808 tonnes of silver this year so far, and 1,237 tonnes of gold. Comex is truly the largest gold and silver source in the world.

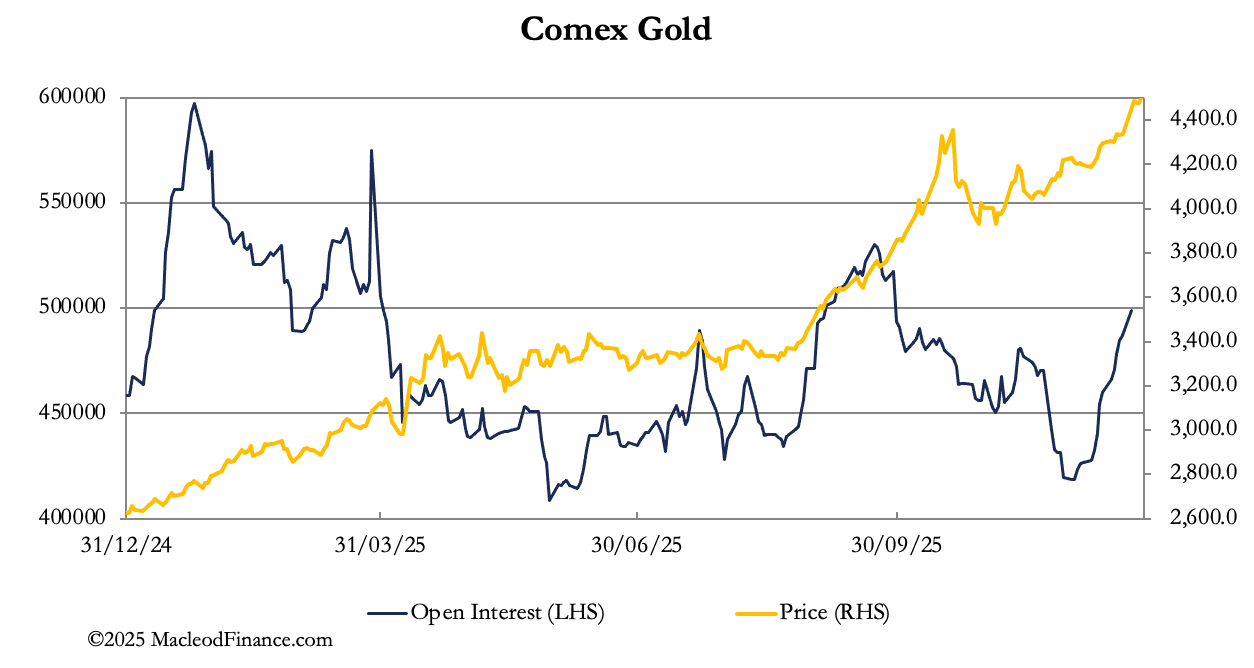

We should concentrate on gold, which is the primary market indicating that the problem is an early stage of a fiat currency crisis. To observers of the debt-cum-credit bubble, the reasons should be obvious. Furthermore, with the exception of the Bank of Japan, G7 central banks are easing interest rates and in the case of the Fed openly moving towards money printing in the form of QE. It stands ready to finance both the government deficit and its debt refinancing totalling over $9 trillion by QE in an attempt to put a lid on bond yields.

Undoubtedly, foreign central banks see this as vindication for doing away with the dollar and will not pause in their acquisition of gold both as reserves and for wealth funds. And this is before we even talk of investor and speculator demand when the consequences of monetary policies become more widely understood by domestic investors. The Comex numbers indicate that open interest is beginning to pick up and will have further to go. This is evident in the chart below:

Thus, the setup for 2026 is emerging. A crisis in paper markets created by undeliverable silver as they move towards a cash basis, and at the same time accelerating monetary inflation in the major currencies leading to currency debasement. Currency debasement means higher prices, and higher prices for all commodity categories and wholesale prices generally will be the unpleasant surprise in 2026.