PMs ready for next move

Aug 22, 2025·Alasdair MacleodQuiet conditions in precious metals belie explosive upside potential, given a government bond market crisis developing in all major currencies.

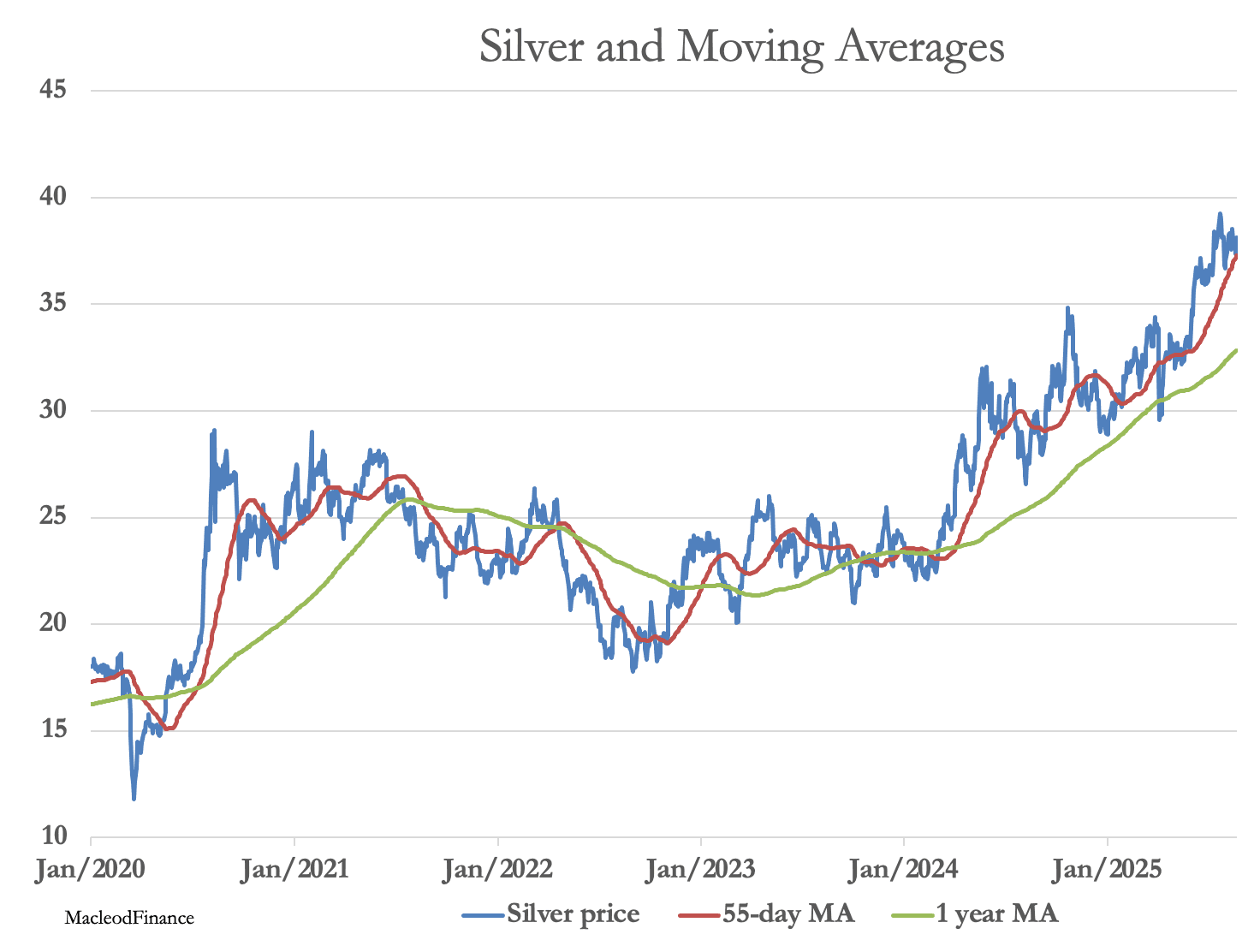

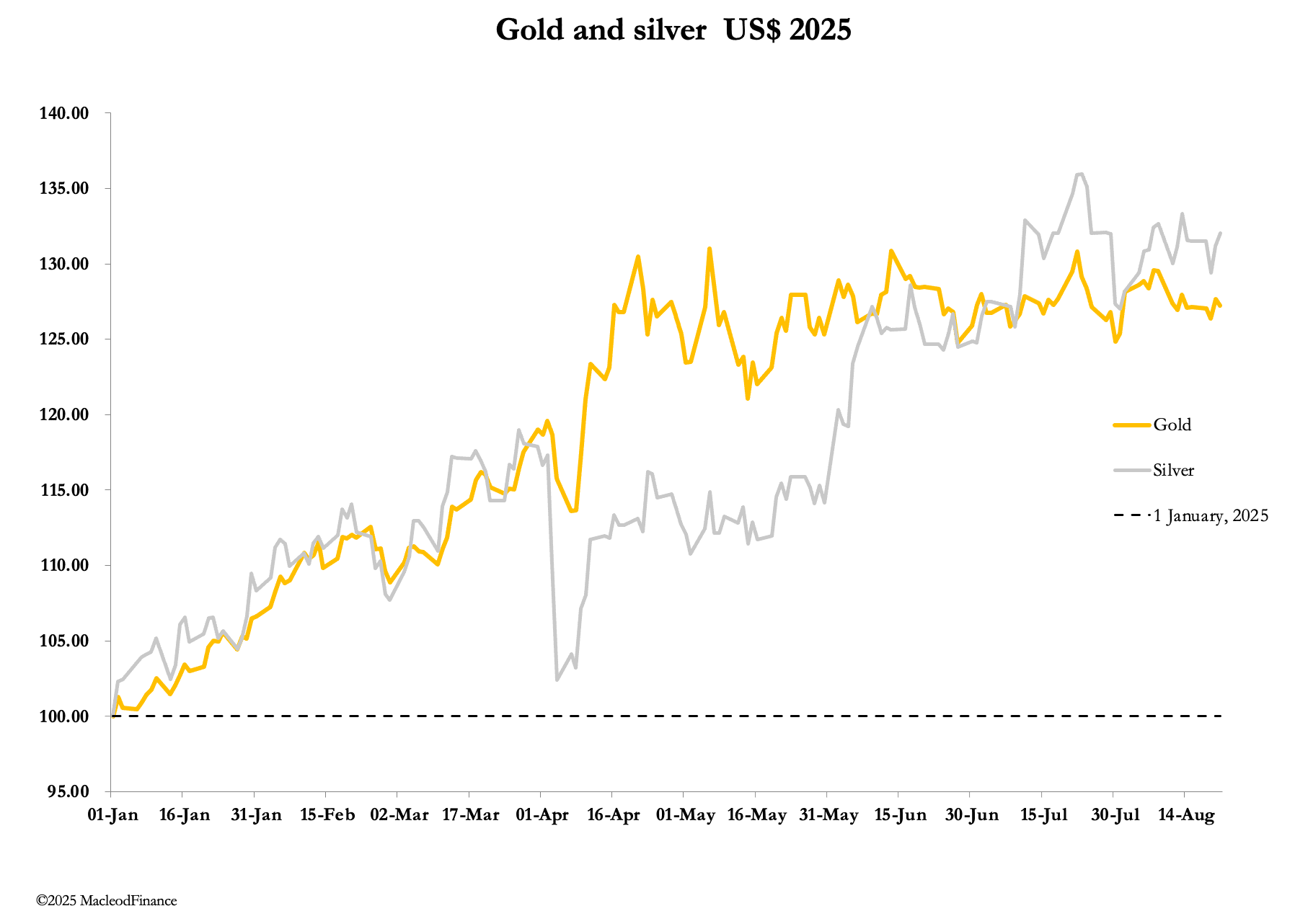

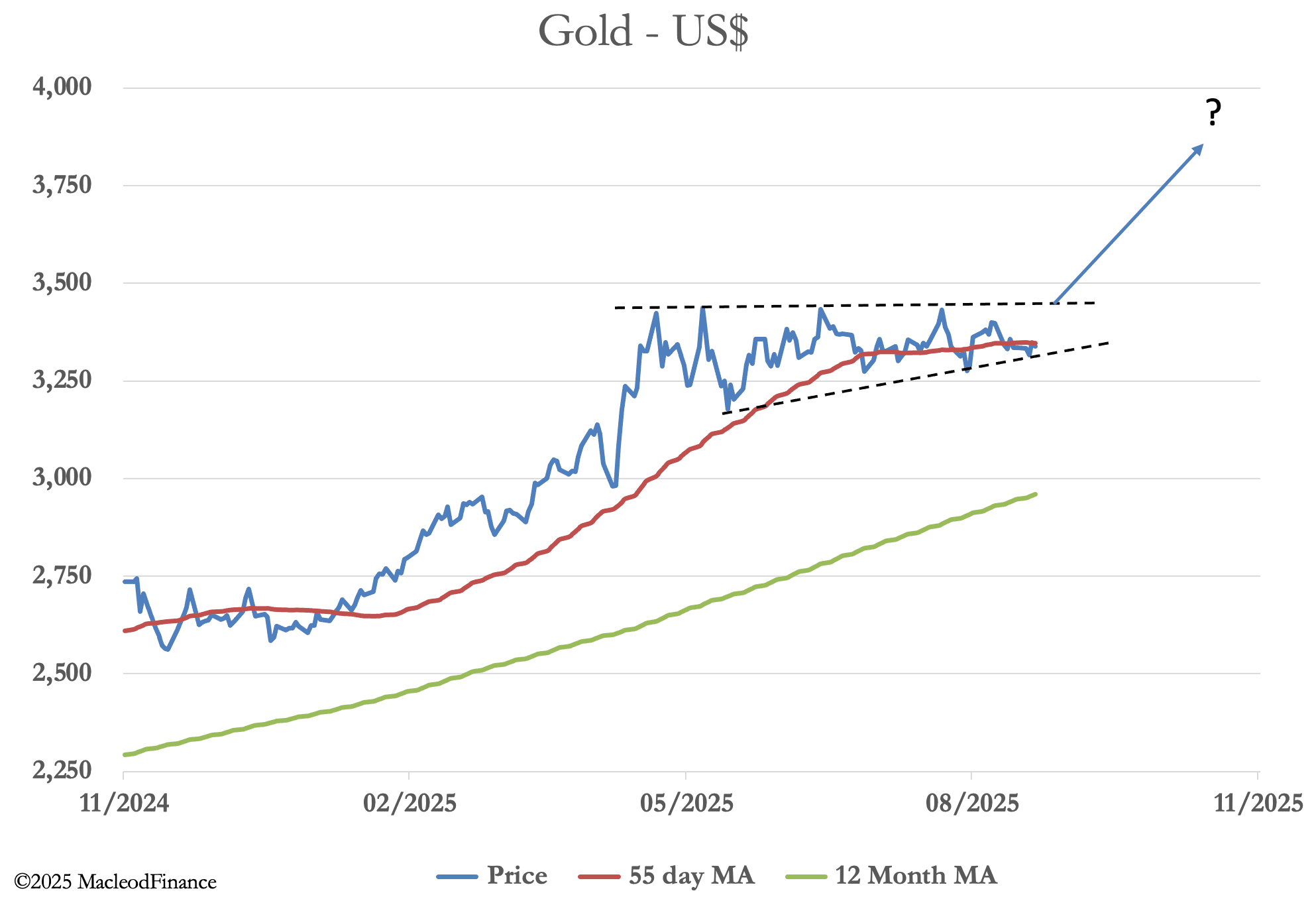

In quiet trading, the current consolidation phase in precious metals extended this week. This morning in Europe, gold at $3330 was down $6 from last Friday’s close, and silver at $38.00 was barely changed. Gold has now been trending sideways for four months, half of 2025 to date while silver has outperformed with the gold/silver ratio falling from 105 to 87.

A notable feature in these otherwise unremarkable conditions has been stand for deliveries on Comex. Since the end of July, a whopping 102.8 tonnes of gold have been stood for delivery, taking the total so far this year to 873.6 tonnes. In silver, over the same periods, 267.5 tonnes and 8,665 tonnes have stood for delivery respectively.

Those in the know are hoarding physical at the expense of paper. But in the very short-term, so far as prices are concerned, the last trade for September options is next Tuesday with calls expiring, providing a strong incentive for market makers to mark gold and silver lower.

This short-term stuff will prove to be irrelevant. We are in the eye of a financial hurricane, and this is set to change.

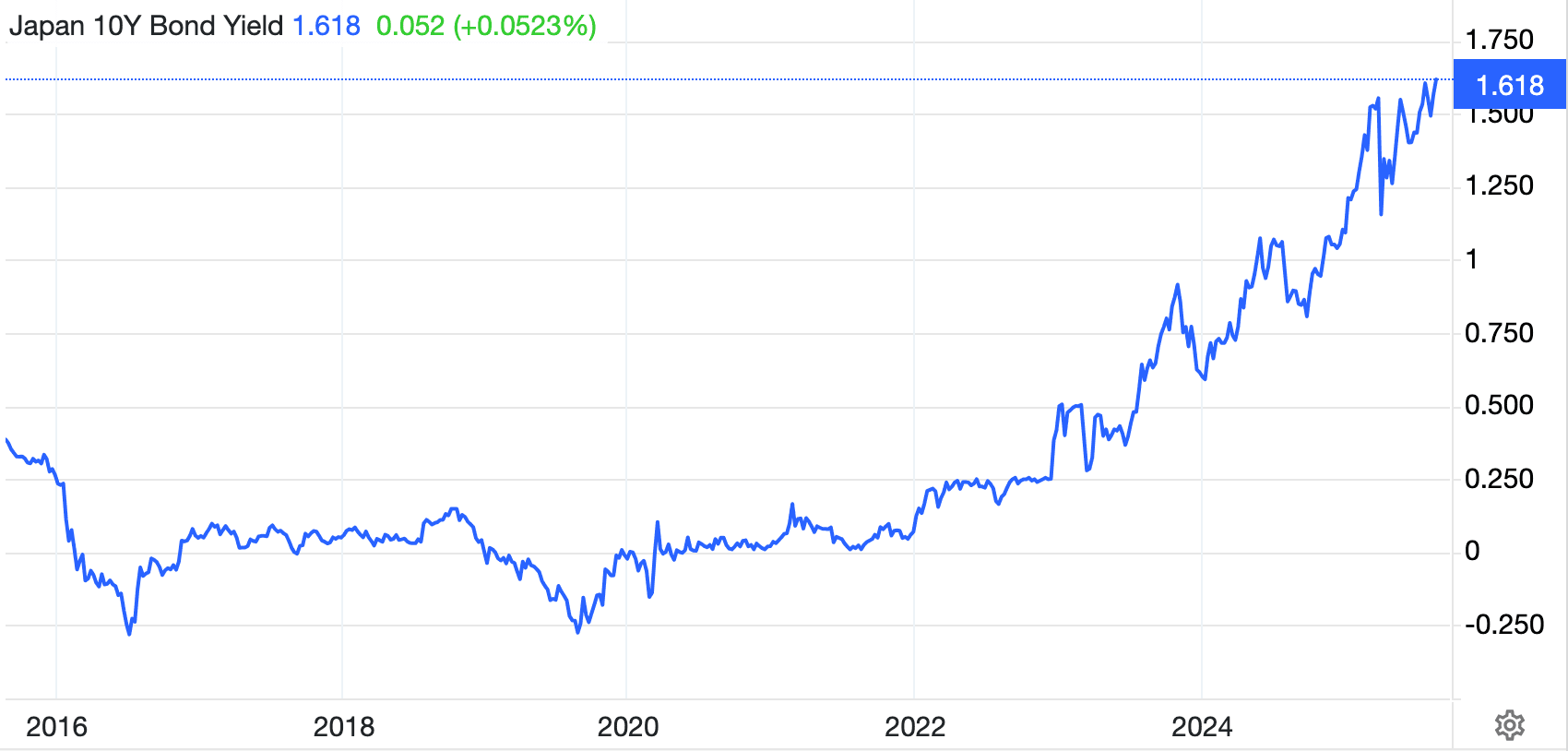

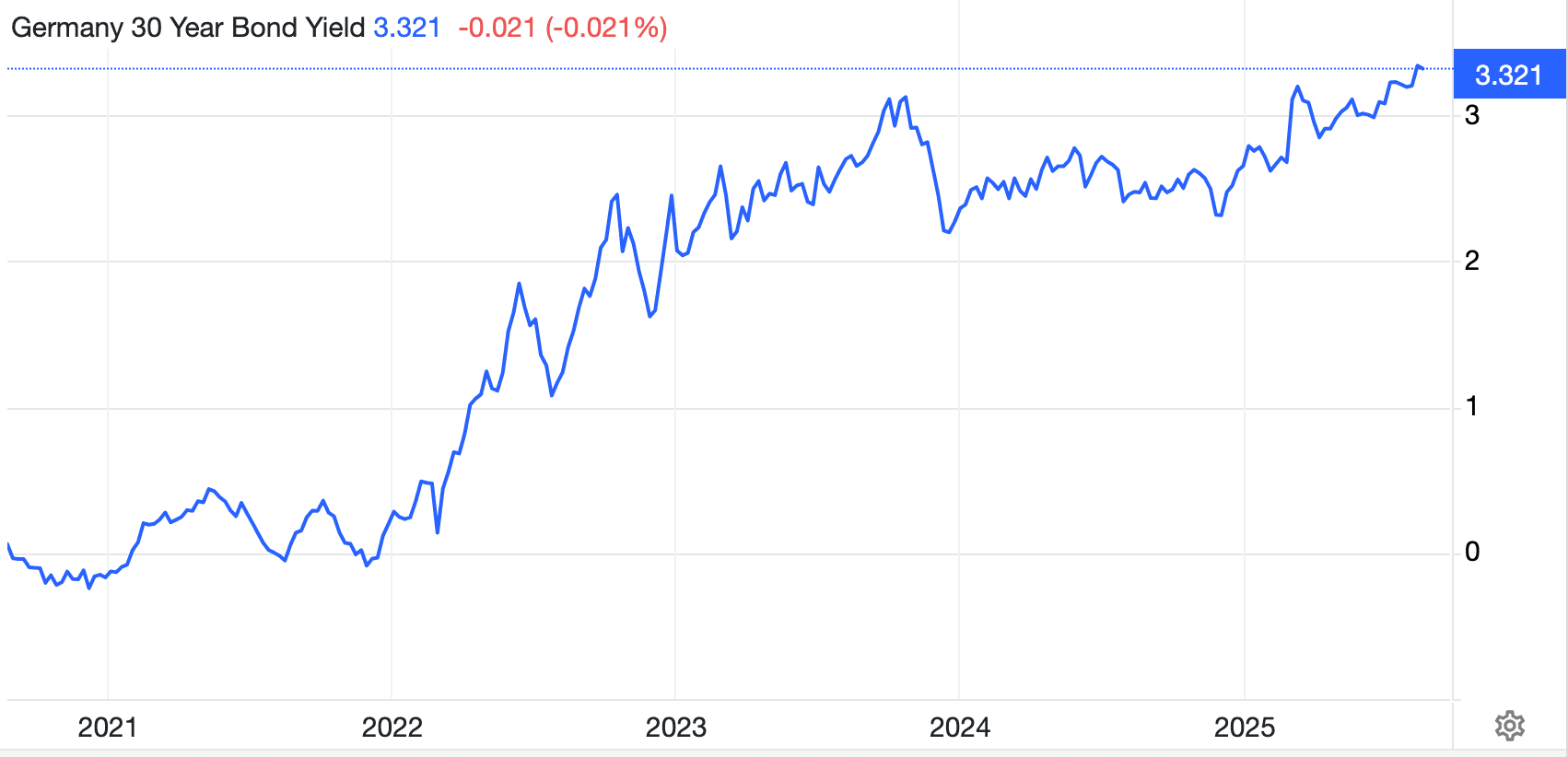

With trading in gold and silver quiet, we turn our attention to a developing bond market crisis, and how it impacts gold and silver. Long maturity yields are rising as evidence mounts of a buyers’ strike on a global scale. The only reasons that yields have not gone even higher is because governments have restricted supply by funding in short maturities, and markets are still in a summer torpor with investment managers away from their desks.

When they return in the coming weeks, they will find that CPI inflation is rising, economies are stagnating, and the government deficits which require funding are turning out to be larger than expected.

Japan’s 10-year bond yield is higher than it has been since 2008 and appears to be going higher still:

The 30-year JGB yield is double that. Germany’s 30-year bund tells a similar story:

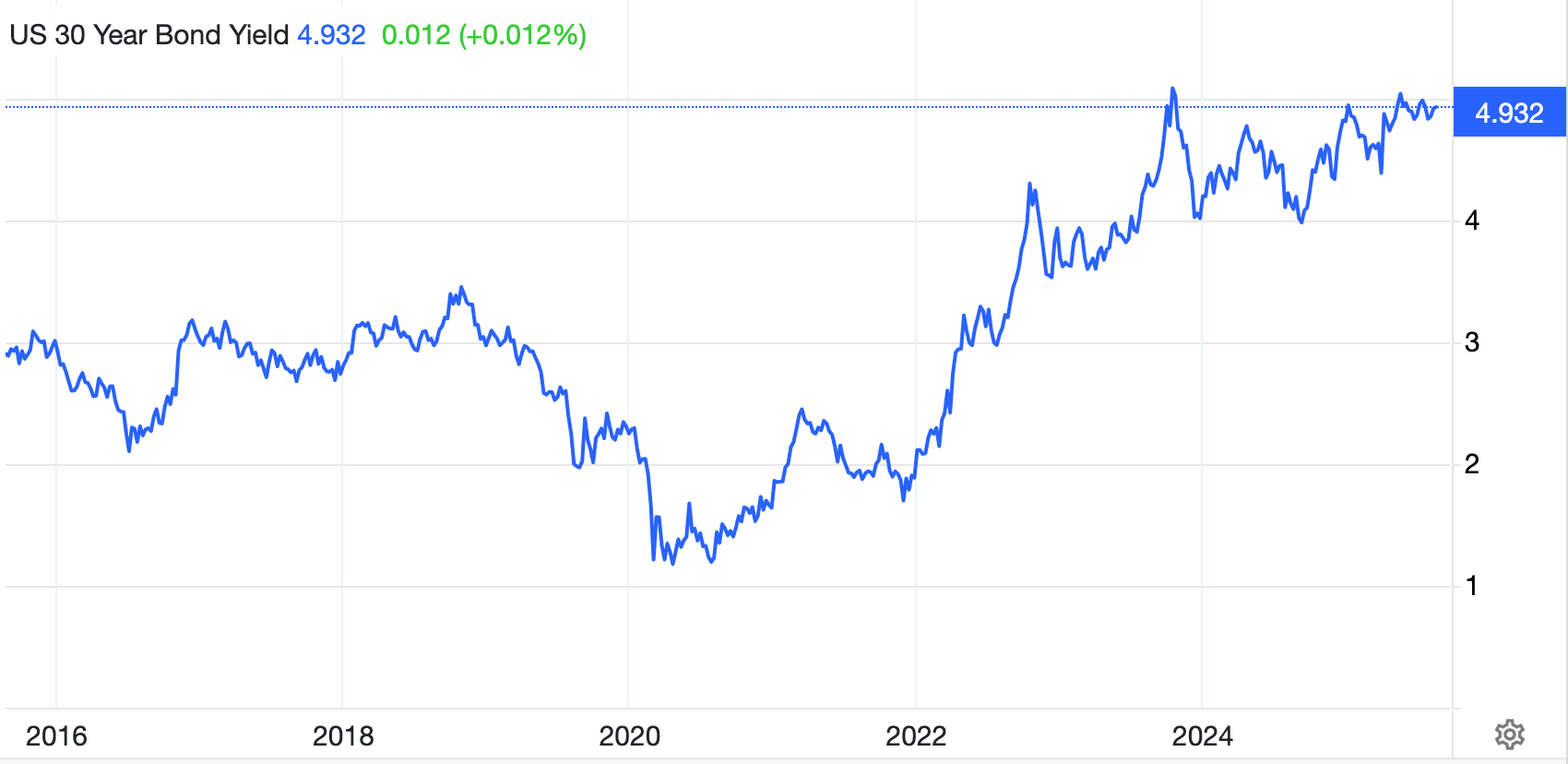

Uk’s long gilt yield is similarly bearish, while the US long bond yield is left slightly behind but look set to break out at any moment:

It is a global phenomenon common to the largest four currencies. Rising yields at the long end of the curve are now dragging benchmark 10-year yields higher. And when the long bond yield rises above 5.1%, it is likely to trigger a crisis not just back down the yield curve, but for equity valuations and those of other financial assets as well.

So where would that leave gold and silver? Clearly, a debt crisis popping the equity bubble has major implications for fiat currencies.

Until recently, traders believed that higher interest rates and bond yields were bad for gold, but that myth ignored the experience of the 1970s and has been blown out of the water by gold correlating with higher bond yields. The reason is simple: higher bond yields reflect a decline in confidence in the issuer and/or an expectation of a fall in the currency’s purchasing power and the value of associated credit. It is the fundamental reason why central banks are selling fiat for gold.

The risk to government bond values is tied to a rapid deterioration in government finances. Stagnating economies combined with high debt to GDP metrics are leading them into debt traps, which can only be negated by massive cuts in government spending. There is no evidence that the necessary cuts are forthcoming. Keynesians believing in credit stimulation completely wrong-footed.

Therefore, gold whose purchasing power is relatively consistent over the centuries appears to rise as currencies decline. But after its 4-month consolidation, gold is now close to breaking out on the upside as credit risk in currencies increases, as the technical chart below illustrates.

And silver leads the way. If silver was a stock, we would say it is undergoing a radical rerating.