Market Report: Massive falls in PMs

Oct 7, 2016·Alasdair Macleod

Precious metals suffered a torrid week, with silver particularly hard hit.

Gold fell from last Friday’s close of $1312 to $1250 at the lowest point yesterday, a fall of 4.7%, and silver fell from $19.16 to $17.11, down 10.7%. In early European trade this morning, prices were steadier, but given the extent of the falls it is reasonable to expect a rally on pre-weekend bear closing.

The possibility of these falls, taking gold towards its 200-day moving average, was foreshadowed in last week’s market report, where I listed some technical reasons why the dollar might surge against other major currencies. This is what actually happened this week, with the yen falling by over 3%, the euro by roughly 1%, but the pound by 5%. Indeed, sterling suffered a flash-crash overnight taking it down as much as 6%, before recovering to GBP1.2460 in early European trade this morning.

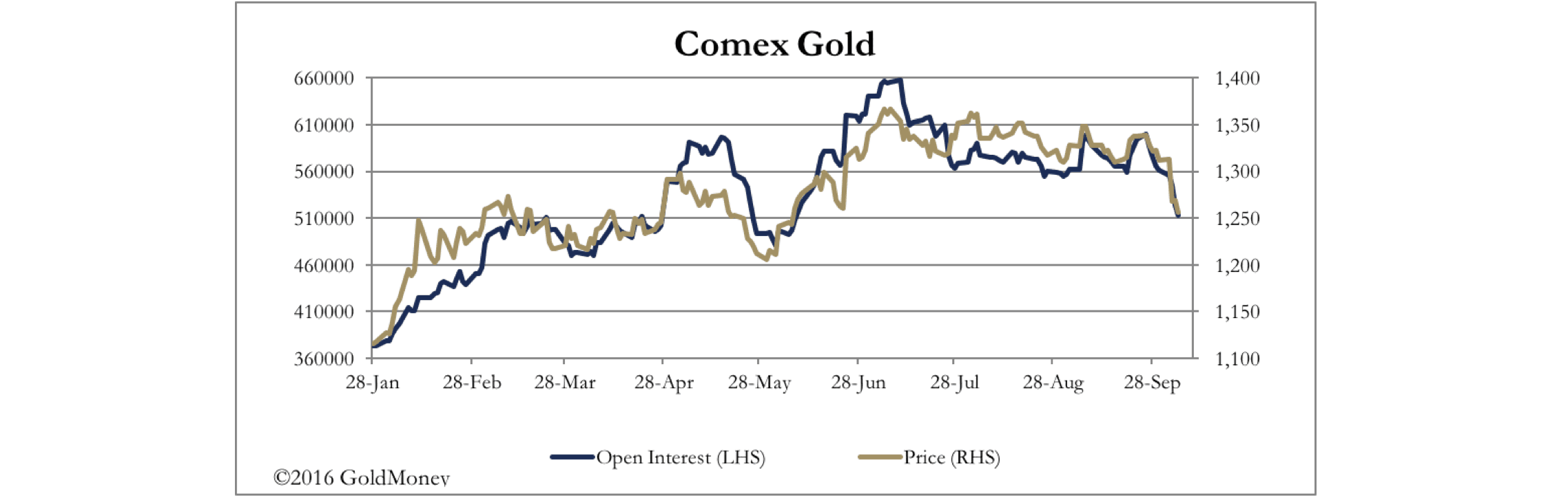

It has all been about currency, and the generally unexpected sudden strength of the dollar. The acute shortage of 3-month dollar money finally triggered a dollar currency squeeze, as I predicted last week. Adding to the currency mayhem has been the opportunity for the bullion banks to reduce their gold shorts on Comex substantially, as shown by the fall in open interest in our second chart.

It is the desire for profits on the short tack that has driven the move, and it has succeeded in scaring the longs into selling. Since early July, the shorts have managed to close positons representing 14,467,500 ounces for a notional profit of over $1.5bn. It’s the old story, wash, rinse, repeat. It has however taken gold back to its 200-day moving average, shown in our next chart.

This tells us that if currency volatility calms down, gold will find support at current levels.

With the dollar being the strongest currency, gold has fared better priced in the other majors, which is shown in our next chart.

This currency mayhem comes at a time when it is obvious that central banks have failed in their monetary policies to achieve any of their economic objectives. Investors, who have been content to go with the central banks’ flows and routinely invest in financial assets are now faced with a quandary. Do they now assume that easy money policies, including QE, will be abandoned, replaced perhaps by a strong dollar/weak euro/weak yen/weak sterling as a new coordinated monetary policy? Supporting this thesis have been rumours that Draghi will taper, Kuroda has lost credibility, and the Fed chairmen of Richmond and Cleveland hinted at dollar interest rate rises, due to the risk of higher inflation next year.

This should be no surprise to regular readers of Goldmoney’s research, which has been pointing out this danger for most of this year. However, I should add that we have also pointed out that the Fed’s room for manoeuvre is severely restricted by the overhang of non-productive debt, and the financial crisis a rise of less than two per cent in the Fed Funds Rate would engender.

In summary, markets are going through a crisis of cherished assumptions, and is faced with having to adjust to central banks raising interest rates, but not by enough to counter the inevitable global stagflation we have argued is the most likely outcome next year.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.