Market Report: Waiting for Godot…

Dec 11, 2020·Alasdair Macleod

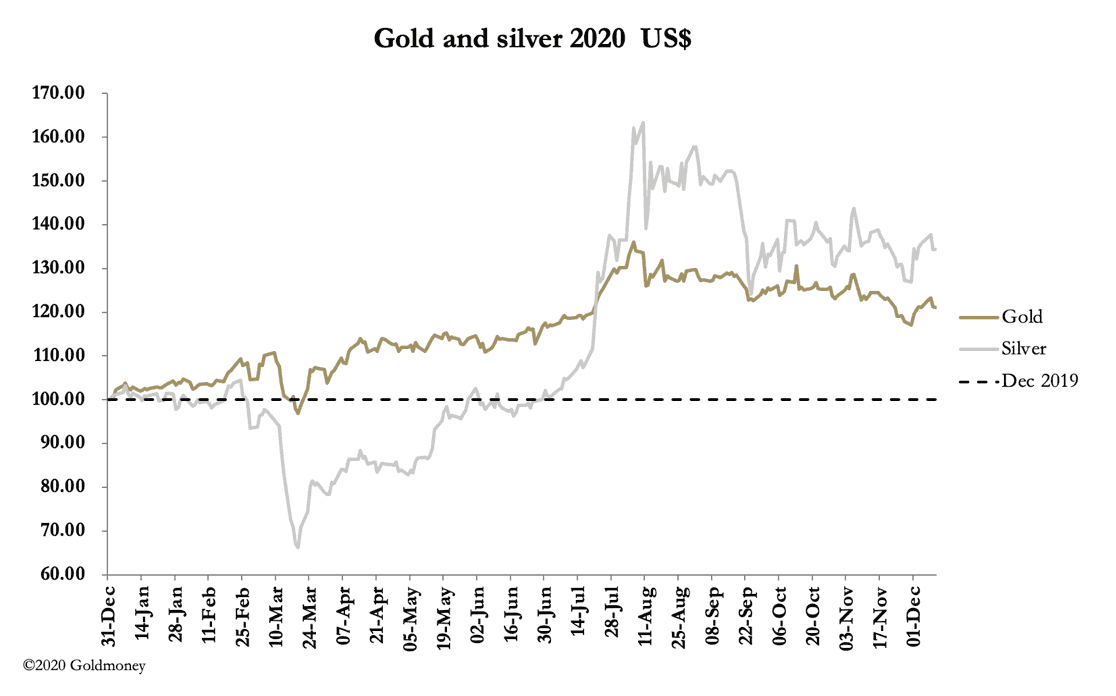

This week, gold and silver rallied on Monday and Tuesday before drifting lower subsequently and ending up little changed on the week. In morning trade in Europe today, gold traded at $1835, down $3 from last Friday’s close, while on the same timescale silver lost 30 cents at $23.86. Volumes on Comex were low.

It is as if markets are waiting for something which might not happen, hence the reference to Samuel Becket’s play in our headline. While the covid situation continues to deteriorate, we await a second US stimulus package, and perhaps, for the year-end to pass. The chattering classes talk about inflation watchers selling their gold ETFs for cryptocurrencies. But there is no evidence that that activity goes beyond a few trend-chasing speculators. And even then, bitcoin has fallen from $19375 last Friday to $17752 this morning — hardly a sensible switch.

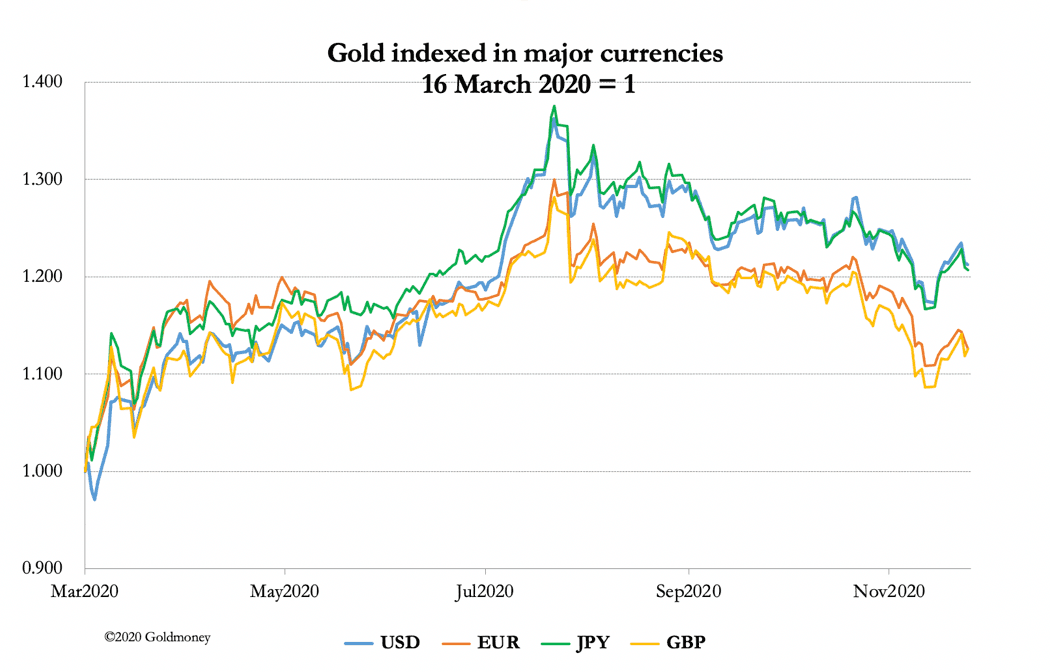

The fact of the matter is gold is up only 21% in dollars, and in euros and sterling, even less as our next chart shows.

The chart is indexed to the day the Fed cut its fund rate to zero, and the following Monday the Fed announced limitless QE. Those events marked a turning point for nearly all financial assets with the exception of fixed interest bonds. Put another way, the purchasing power of the dollar in these instruments has declined. Leading the charge against the dollar should be gold. The fact that gold has lagged is explained by actors in financial markets not understanding that it is fiat-driven price inflation driving prices higher. Indeed, commentators are focusing not on the dollar’s purchasing power but on specific factors for, say, copper, lumber or cryptocurrencies.

The truth is therefore yet to be discovered and short-term speculators, in euros or sterling for example, have seen gold rise only 12% since they were promised infinite inflation back in March.

Yesterday, the ECB announced a further €500bn of QE extension to its pandemic emergency purchase programme, meaning it will keep all government bond yields suppressed. Spanish and Italian debt yields quickly fell to zero, despite the obvious credit risks.

The ECB is now visibly struggling to keep the Eurozone and its currency from sliding into a monetary, economic and banking crisis, while the political class is making things worse with their self-harming over Brexit. Le crunch is around the corner. Just wait for German savers and investors to wake up to the implications; demand from them for under-priced bullion is likely to increase substantially.

Making things worse for the EU, and for everyone else, is a global logistical foul-up, with containers out of place everywhere. China has none, they aren’t clearing through European and American ports, and perishable contents are rotting on quaysides. It seems likely that food prices will soar ahead of Christmas and beyond, fed by a combination of covid-19, a logistical container crisis and monetary inflation.

These conditions suggest that there will be a growing realisation that precious metals are under-priced and should be bought as the most secure hedge against rapidly deteriorating outcomes in 2021.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.