Market Report: PMs and the commodity story

Sep 11, 2020·Alasdair Macleod

In quiet trading, gold and silver drifted sideways this week in a tight trading range. In European morning trade gold edged up $13 on the week to $1945 while silver fell 4 cents to $28.82. Encouraging this torpor was the dollar, whose trade weighted index rose this month by 2%. Undoubtedly, it will have encouraged hedge funds to buy dollars and short gold. In normal times, bullion bank trading desks would have smashed the price to trigger stops and thereby cover their short positions, which are still extremely costly. This is our next chart.

The talk among some technical traders is that gold and silver are likely to consolidate further. And if gold is to test its 55-day moving average, then the price will probably find support at $1900. This is our next chart.

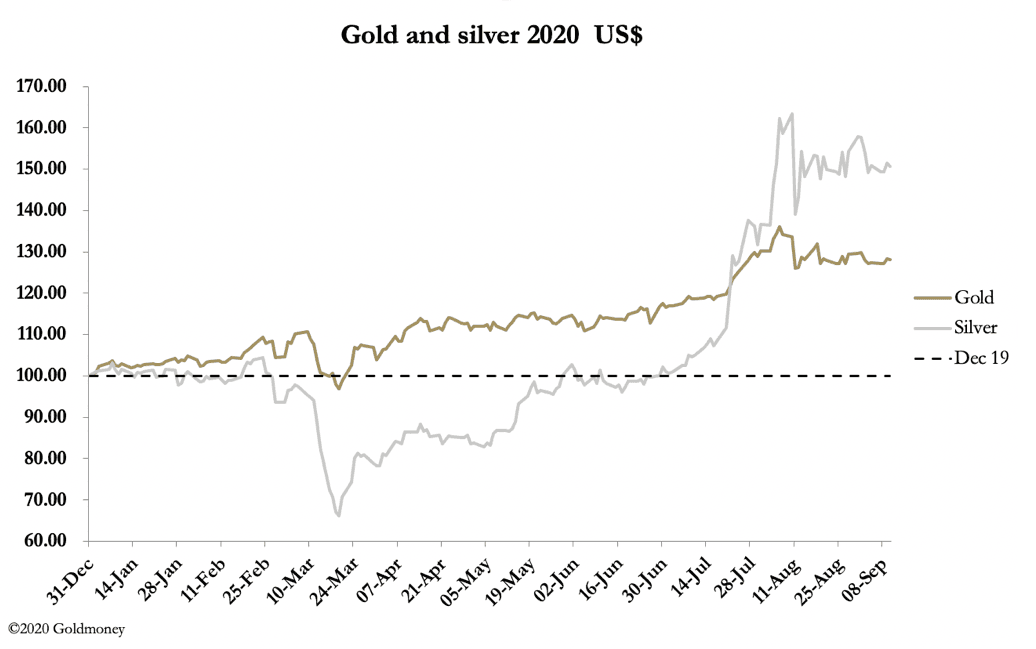

Regular readers will recall the importance of 23 March, when the Fed switched to unlimited monetary inflation only days after cutting its funds rate to zero. Gold rose from $1460 to a high of $2075 on 7 August. At the same time, base metals began to rise, and a wide range of other raw materials from lumber (+250%) to lean hogs (+73%) also rose.

Our next chart puts the relationship between gold and commodities in context: it could be the most important chart of this year.

The pecked line divides 2020 into two. First was the intensifying deflationary sentiment ahead of the Fed’s rate cut to zero on 16 March, and its promise of unlimited inflation in the FOMC statement of 23 March. And secondly, the inflationary period that follows. It was at that point that the S&P500 reversed its fall of 33% and started its dramatic move into new high ground, and the dollar’s TWI peaked, losing about 10%.

Gold took the hint and rose 40%, while commodities turned higher as well, gaining a more moderate 20%. It was initially suppressed by the WTI contract delivery debacle in April. But both gold and commodities are clearly adjusting to a world of accelerating monetary inflation. And here it is worth noting that a contracting global economy is perversely positive for commodities measured in fiat, because their prices reflect fiat losing purchasing power at a time when both supply and demand are being equally reduced. And in the long-term commodity prices are far more stable measured in gold than in fiat money, which tells us that theoretically commodity prices have further to rise.

China has already begun to act on this trend. They are selling dollars to buy and stockpile global commodities in enormous quantities, even selling down their holdings in US Treasuries to do so. So far, commentators have not got the message: it is less about commodities, which are always available, but China is extracting value from her fiat dollars while she can. Commodities, as well as gold and silver, are the only safe haven for China in these inflationary times.

Just ponder, for a moment, upon all the implications.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.