Market Report: Small year-end rally

Dec 23, 2021·Alasdair Macleod

In the run up to Christmas, turnover in gold and silver contracts on Comex slowed to a crawl. Having ticked back slightly on Monday and Tuesday, on balance both metals rallied this week, with gold up $7 from last Friday’s close to trade at $1805 in European trade this morning (Thursday). Silver gained a net 50 cents at $22.83 over the same timescale.

For speculating bulls, 2021 was a disappointment. Gold is down 5%, and silver 13.5% since 1 January. But it should be viewed as a consolidation of gains in 2020.

The stories dominating precious metals this year have been inflation and the introduction of Basel 3’s net stable funding ratio regulations. Inflation in the form of producer and consumer prices evolved from the Fed’s transient description to something more serious. But the Fed, the ECB and the Bank of England are still officially denying it is a long-term problem, claiming it will just take longer to get back towards their 2% annual target.

Basel 3’s NSFR regulations have caused significant confusion for investors. Initially it was difficult for them to understand the bank-speak involved, and then they hoped that bullion banks would simply withdraw from London’s OTC derivatives and Comex’s futures. But banks cannot just withdraw from these markets, when in aggregate they are net short. It takes time.

Silver underperformed gold this year, which was in accordance with their long-established price relationship. But the fall, being 13.5% against 5% for gold, was excessive on historic price evidence, which shows silver’s relative price volatility over the long term to average about 1.8 times. But there is no doubt that silver suffered particularly from the aftermath of an ill-fated attempt to persuade small traders on the Robinhood platform to create a physical squeeze on the establishment. That ran the price up to $30 on 1 February, when the bullion banks simply crushed these amateur speculators in their time-honoured way.

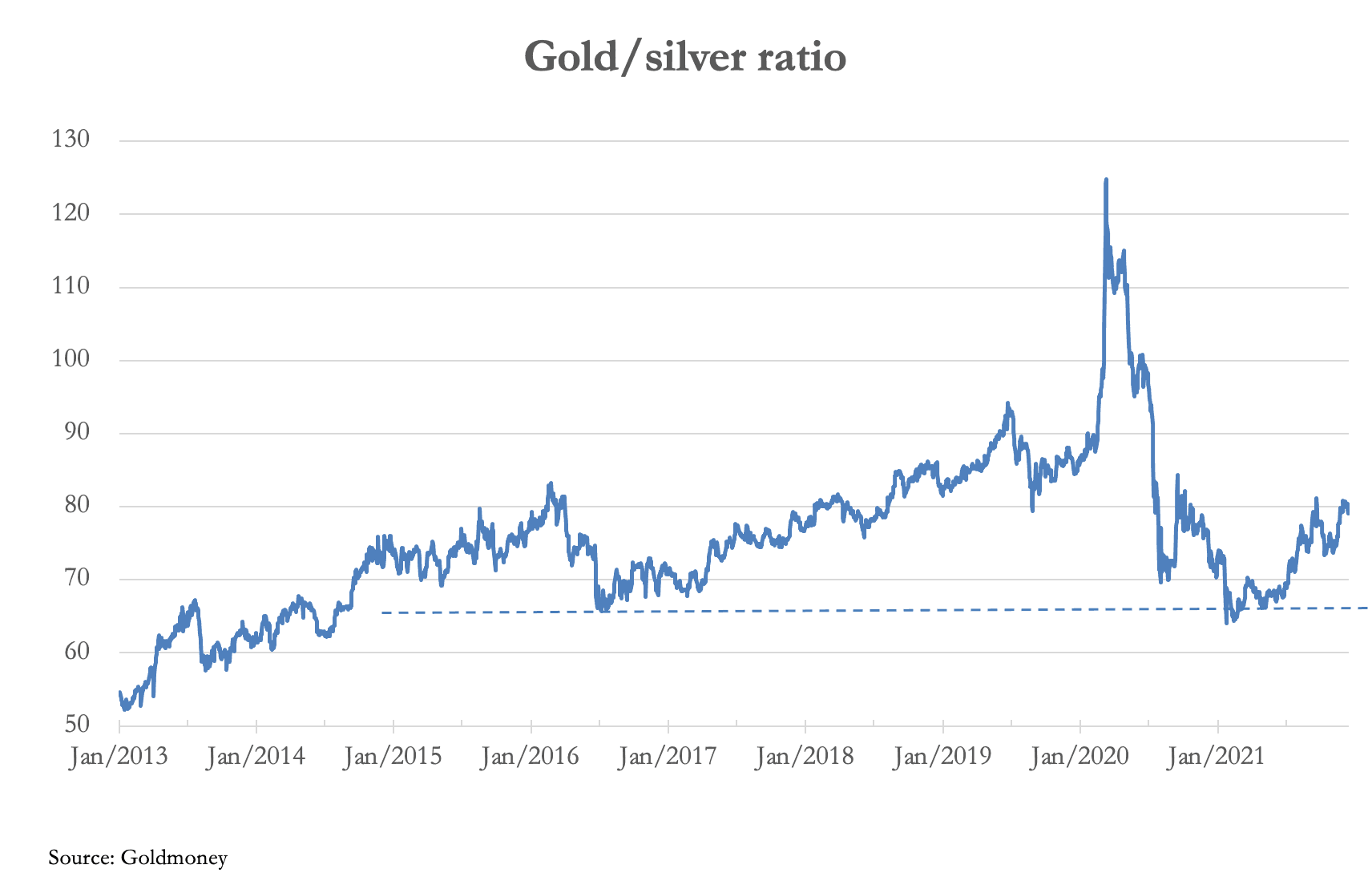

Our next chart is of the gold/silver ratio.

At 79, this ratio has increased from 72 at the start of the year, going some way to correcting the substantial fall from the March 2020 peak. But the price is still double the low seen on 18 March 2020.

There can be little doubt that the silver price suffers from its relationship with derivatives, which are about 20 times the annual offtake into investment. But supply and demand for physical metal are likely to change next year, with increasing investment in environmentally friendly, non-fossil fuel energy. While silver fell 13.5%, lithium carbonate rose 520%, and uranium oxide by 54%. Copper is up 25%. Silver was the anomaly. As the most conductive metal silver’s industrial future appears under-rated, with its monetary qualities thrown in for nothing.

This is where inflation comes in. Clearly, rising consumer prices are not transient, and given the massive expansion of fiat currency supply over the last two years, there is more to come. 2022 is bound to see more price inflation, and gold and silver prices are yet to reflect it. And with its industrial connotations, silver could be the star performer.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.