Market Report: Silver strong

Jan 21, 2022·Alasdair Macleod

Our headline chart shows how, after the first week in the New Year, the silver price has rallied strongly, up by nearly 10%. This week gold rose $18 from last Friday’s close to trade at $1835 in Europe this morning, and silver by $1.50 to trade at $24.45 at the same time. Most of the rise was on Wednesday, with yesterday and today seeing some price consolidation.

Gold’s Open Interest on Comex is rising strongly and on preliminary figures for yesterday stands at 561,759 contracts. This is shown in our next chart.

The days of containment for the Swaps’ short positions appear long gone with a rising trend established from last June. This is important, because the bullion bank trading desks, who make up about 70% of the Swaps, want to contain their short positions for two basic reasons: first, the introduction of the Basel 3 net stable funding ratio discourages banks from running uneven positions; and secondly, with soaring price inflation demand for physical metal will as well.

It is noticeable that the exchange for physical figures rose sharply this week as gold rallied, indicating that the Swaps are hedging their Comex shorts from London. These numbers should be watched carefully for signs of the distress that caused an ESF blow-up in 2020, when the bullion price soared from $1450 to $2075. They may indicate shorts being taken out in London to cover on Comex, giving the appearance of offsetting longs.

This should remind us that the London forward market, which provides little more than out-of-date vaulting statistics, is far larger than Comex, and that we must not get too hung up on Comex numbers which can be manipulated from London.

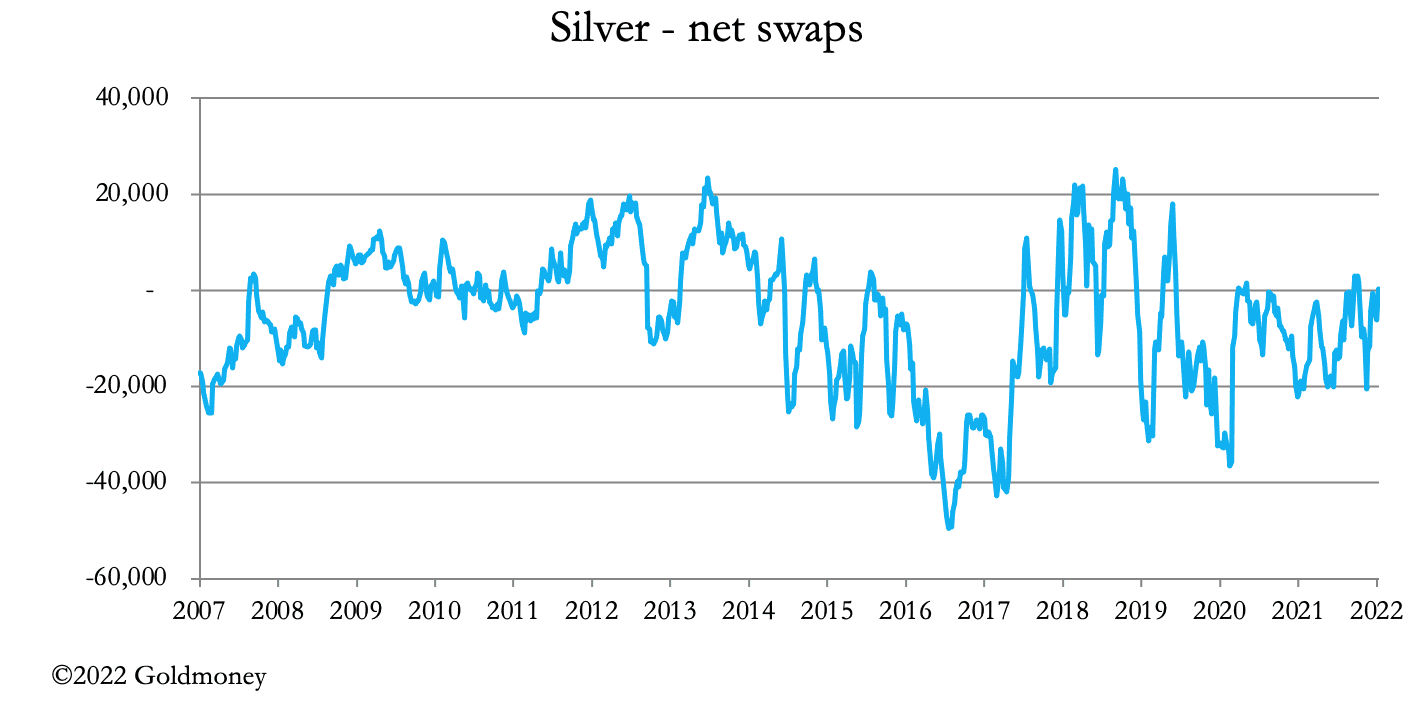

While the Swaps are being squeezed in gold, their position is different in silver, as our next chart shows.

At net long 225 contracts on 11 January, the Swaps’ behaviour is very different from gold, where they are desperate to contain short positions by capping both the gold price and Open Interest. In silver, the problem is to avoid being short in the first place, marking prices up to deter buyers. This is the most likely explanation for silver’s dramatic outperformance over the last fortnight.

There is very little physical stock available in reasonable quantities, making short derivative positions doubly dangerous. And we can’t be sure that a significant price markup will alleviate this condition because of soaring industrial demand on the back of environmental energy replacement factors. Bearing in mind that lithium and uranium prices soared last year when silver fell 12%, the potential for the silver price to rise is significant if investment demand does little more than stabilise.

Economic conditions show consumer price inflation not only being persistent but continuing to rise. To this pain we can add growing evidence of a global economic slowdown after post-covid lockdowns led to a brief recovery. China, which is facing a property crisis, even lowered its loan prime rates yesterday, in a move which other central banks would love to copy.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.