Market Report: Options expiry passes…Q2 next

Jun 25, 2021·Alasdair Macleod

After the sharp falls of last week, gold and silver trended sideways to slightly up this week in tight trading ranges and light turnover. By morning trading in the European time zone today, gold had recovered $20 from last Friday’s close to $1783, and silver by 43 cents to $26.21.

Yesterday saw options expiration on Comex, with only 3,917 July gold calls exercised and 82,954 abandoned. In the puts, 33,145 were abandoned and 24,285 were exercised. While profits and losses on individual contracts vary considerably, these statistics illustrate the scale of net profits gathered by option writers, in the main being bullion banks. It also explains the money to be made by the establishment when it gets prices down to a level which maximises the net returns from abandoned calls and exercised puts.

Undoubtedly, this has been a significant factor behind the sudden drop in the gold price from the $1900 level on 11 June, ahead of yesterday’s expiry date. Now that the exercise date has passed, it is tempting to think that selling pressure has been removed. But there is still the accounting date of end-June, when first half trading points are struck, and the trading book is marked to market. And we know that the Swaps on Comex, who are all subject to this exercise, are net short of roughly $30bn in gold futures contracts at current prices. This is shown in our next chart.

Clearly, subject to any offsets in the London forward market, first half-year trading profits for the bullion banks would be maximised with a lower gold price. We should therefore expect to see the downward pressure on the gold price to continue until next Wednesday, after when these factors cease to be relevant.

Clearly, subject to any offsets in the London forward market, first half-year trading profits for the bullion banks would be maximised with a lower gold price. We should therefore expect to see the downward pressure on the gold price to continue until next Wednesday, after when these factors cease to be relevant. By any measure, that will leave precious metals commencing the second half in an oversold position with the potential to rally strongly. Furthermore, European and American banks will start complying with Basel 3, which from a funding viewpoint penalises open derivative positions, including gold and silver contracts. Bank treasurers can be expected to encourage bullion dealers to reduce open positions as much as possible, which is likely to reduce liquidity in paper markets.

The situation in London appears less urgent with the new Basel regulations applying to all banks operating in the UK from next January. But European and US banks operating in London will comply with Basel 3 from 1 July anyway. In any event, there is little evidence that London is net long of gold and silver, with physical liquidity still fairly tight, so Comex open positions are likely to drive prices.

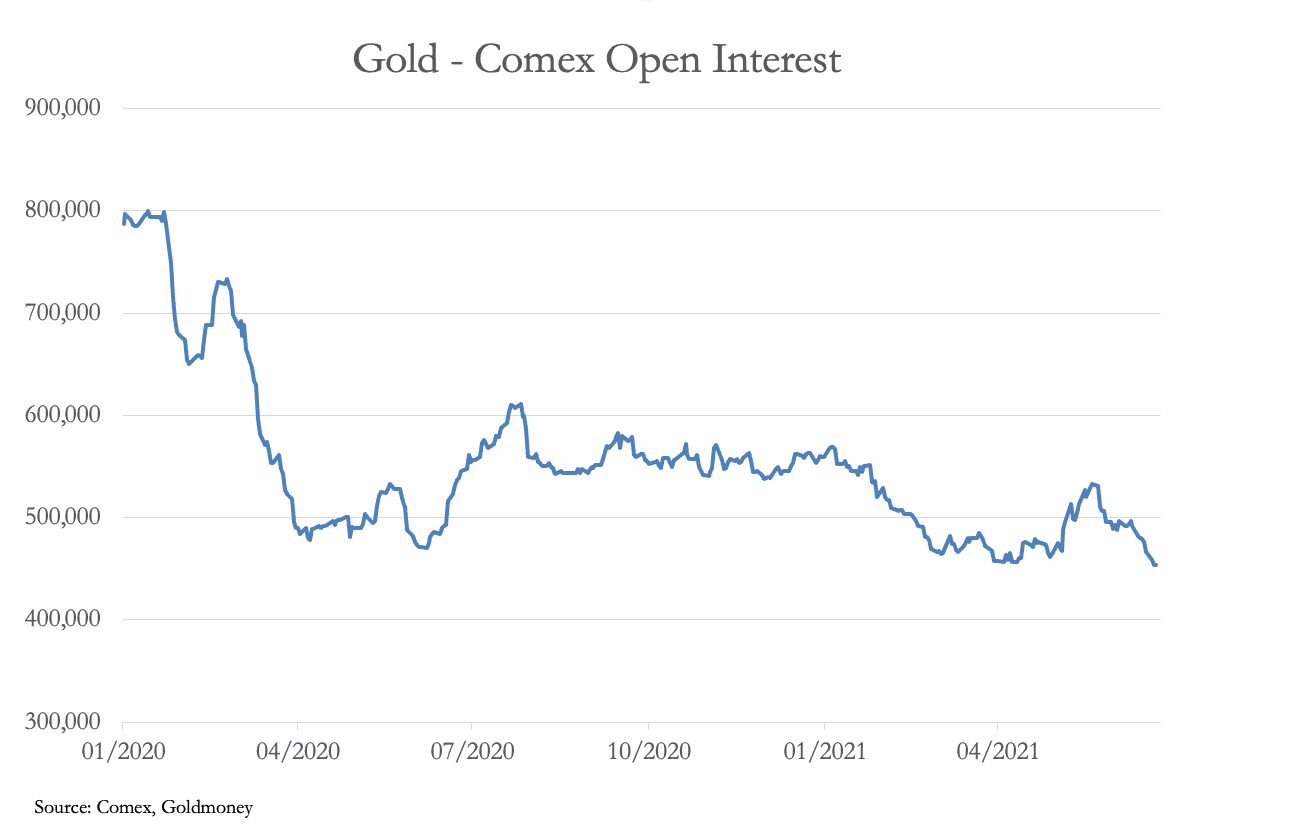

Comex open interest has declined significantly from the record levels of nearly 800,000 contracts at the start of 2020, which is our last chart.

At a preliminary 452,432 contracts yesterday, this is the lowest it has been since the beginning of 2020. And the increase in the dollar’s trade weighted index this week will have probably shaken out any Managed Money stale bulls.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.