Market Report: Futures and physical disconnected

Mar 12, 2021·Alasdair Macleod

Gold and silver rallied this week from very oversold levels, before declining from mid-week highs. In European trade this morning, gold was at $1704, having touched $1740 early on Thursday morning for a net gain of only $6 from last Friday’s close. On the same timescale, silver peaked at $26.44 before slipping to $25.55 for a net gain of 20 cents.

Open interest on Comex has declined to relatively low levels for both metals. That of gold is the next chart.

Open interest matters because bullion banks and miners hedging output take the short side, and low open interest means their combined short position is low. Therefore, their ability to drive prices lower by scaring hedge funds into selling is less than when open interest is high. The chart shows that the price decline since August has coincided with a decline in open interest to the sort of level where further resistance to falling open interest, and therefore the price, can be expected.

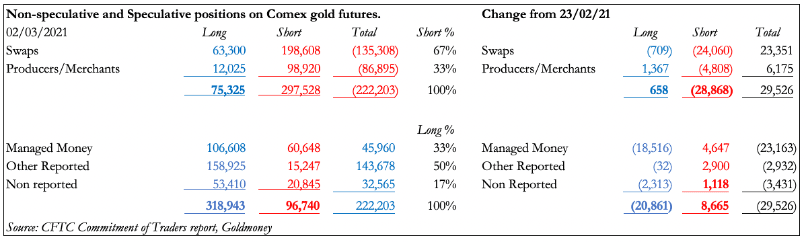

The splits between the Comex categories at the last available data point, 2 March, are shown in the table below.

Two things stand out. First, the swaps reduced their net shorts from the previous week by 23,351 contracts to 135,308, down by a massive 80,155 contracts since 5 January. Secondly, the managed money category (hedge funds) reduced their net longs by almost the same amount — 23,163 contracts. And at net 45,960 contracts long this is tantamount to being moderately oversold with 110,000 net long contracts being the neutral position.

Open interest on 2 March was 467,008, which is only slightly less that today’s 468,453. While there is likely to be some shift in the net longs between categories, there is resistance evident to further falls in open interest.

Anecdotal evidence confirms there is very little physical gold and silver available for delivery. I even had an email from a regular customer of the Perth Mint who reported that all sales of gold and silver have been suspended until further notice. There are similar shortages in all the major trading centres. So how is it that the price keeps falling?

There is only one answer. The price we see on our screens are paper prices, which give or take a few bucks are faithfully tied to Comex futures. They are not prices for deliverable gold: if you want that, then you must join the queue. Therefore, paper and physical prices have become disconnected with the physical price somewhat higher. This is why we see a steady dribble of futures standing for delivery. Between Monday and Thursday, 2,567 contracts were turned into nearly 8 tonnes of gold, and 733 silver contracts into 114 tonnes of silver.

Last trading date for April gold options is 25 March. Gold’s active April contract is running off the board with the last dealing date in eleven trading days’ time. The price disconnection should lead to a jump in standing for delivery. It seems to be the only way to obtain physical.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.