Market Report: Dollar powers ahead

Nov 27, 2015·Alasdair Macleod

Gold and silver prices continued to drift along close to recently established lows this week, showing some support at current levels.

Whether or not there is further weakness to come appears to be a reflection of dollar strength, and it should be noted that the dollar has recently broken into new high ground on a trade-weighted index of other currencies. This is shown in the next chart.

An obvious driver for the dollar is the prospect of the first rise in USD interest rates since the Lehman failure, at a time when other major central banks are contemplating further easing. This is affecting currency relationships as the chart shows, though it is quite likely that current dollar strength will reverse itself unexpectedly.

This analysis overrides action in the gold and silver futures markets, where yet again the hedge funds have been taken to the cleaners. The too-big-to-fail bullion banks are always happy to go short against poor quality buyers, before marking prices down and triggering stops. The stops when triggered reduce the number of outstanding contracts, as can be seen in the next chart, which is of Open Interest on Comex.

An analysis of the price and open Interest relationship confirms. In early September, hedge funds had large short positions, which they closed and reversed over the rest of the month. In October, with gold rising through the $1140 level, hedge funds accumulated long positions, sold to them by the bullion banks and swap dealers. This is reflected in the increase in Open Interest to 465,000 contracts. Through November, the hedge funds were forced to cut their positions, which is reflected in the drop in Open Interest. The relationship is as solid as that between a casino operator and his regular punters.

The moral is that futures markets absorb demand by creating substitutes for physical, and when the demand abates, it's a signal to bang the price. This rinse-and-repeat continues until demand for physical moves the whole basis of the market, and that can be delayed by leasing for delivery and astute delivery management.

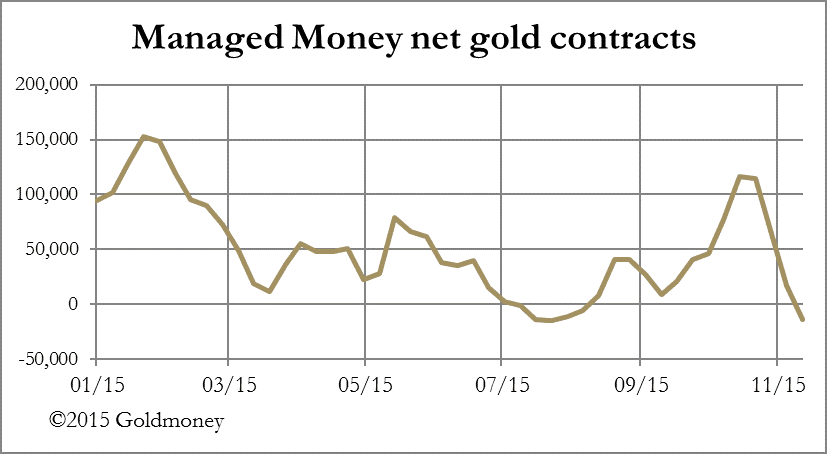

The current position is that the hedge funds are net short of gold contracts for only the second time since 2006 (when disaggregated data first became available) and the swap dealers (mostly bullion banks) are correspondingly net long. This is shown in the next chart.

The conditions therefore exist for the bullion banks to sell down their net longs on rising prices, for the start of a new rinse-and-repeat wash cycle. On this basis, if on no other, gold seems set for a decent rally before window-dressing becomes a factor for the year end.

For what it's worth, the performance of silver appears to be showing further resistance to going lower. This can be taken as a bullish confirmation. All we need now is to see the dollar crack.

Next Week

Monday

Japan: Construction Orders, Housing Starts, Capital Spending.

UK: Nationwide House Prices, BoE Mortgage Approvals, Consumer Credit, M4 Money Supply.

US: Chicago PMI, Pending Home Sales.

Tuesday

Japan: Vehicle Sales.

UK: CIPS/Markit Manufacturing PMI.

Eurozone: Unemployment.

US: Final Manufacturing PMI, Construction Spending, ISM manufacturing.

Wednesday

UK: CIPS/Markit Construction PMI.

Eurozone: Flash HICP, PPI.

US: ADP Employment Survey, Non-Farm Productivity, Unit Labour Costs.

Thursday

Eurozone: Composite PMI (Final), Retail Trade, ECB Deposit Rate, Refinancing Rate.

US: Initial Claims, Factory Orders, ISM Non-Manufacturing Index.

Friday

Japan: Consumer Confidence.

US: Non-farm Payrolls, Private Payrolls, trade Balance, Unemployment.

The views and opinions expressed in the article are those of the author and do not necessarily reflect those of GoldMoney, unless expressly stated. Please note that neither GoldMoney nor any of its representatives provide financial, legal, tax, investment or other advice. Such advice should be sought form an independent regulated person or body who is suitably qualified to do so. Any information provided in this article is provided solely as general market commentary and does not constitute advice. GoldMoney will not accept liability for any loss or damage, which may arise directly or indirectly from your use of or reliance on such information.