Market Report: Books are balanced, time to party

Dec 22, 2017·Alasdair MacleodAt least, that’s how the bullion bank traders must be thinking. Ahead of the Fed’s quarter-point rise in the Fed funds rate, they spooked the longs out of their positions to close their shorts, profitably. Nice bonuses all round.

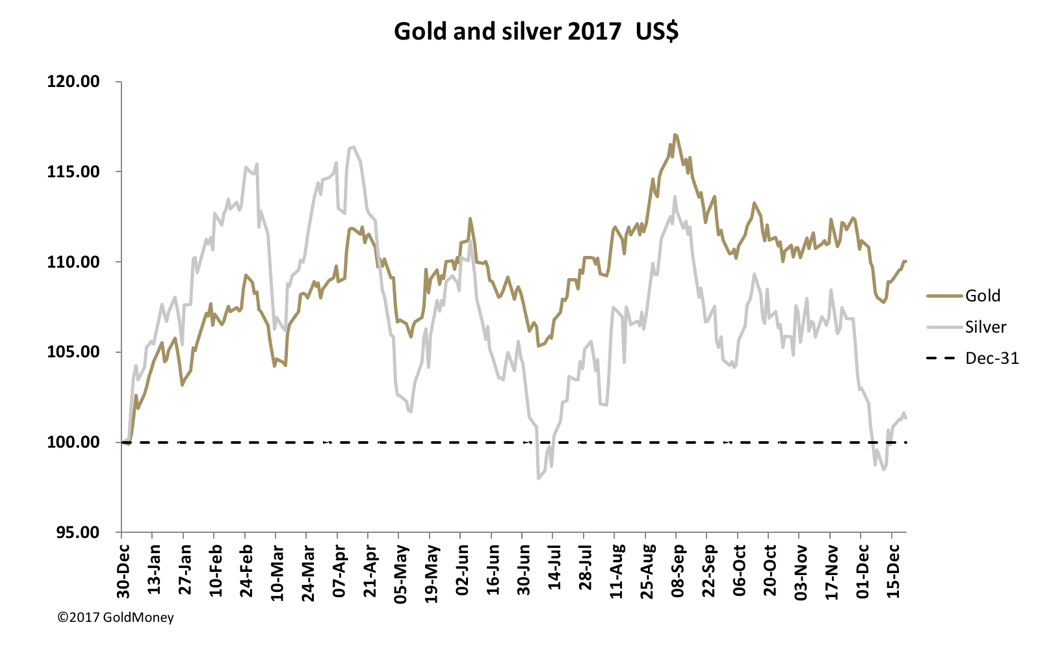

This is the third time in succession this year-end ploy has worked. Our headline chart tells us that silver has been extremely profitable for the bullion banks, gold less so perhaps, but given the trading opportunities taken during the year, it has been pretty good on balance.

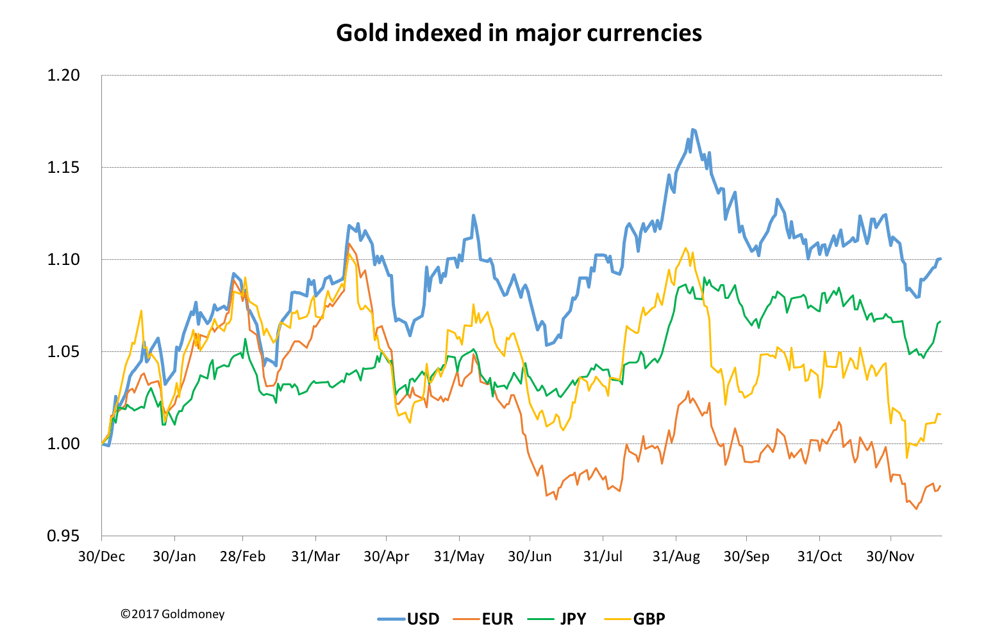

This week, gold rose $12 from last Friday’s close by early morning trade in Europe this morning (Friday) to $1268, and silver 12 cents to $16.20. Pre-Christmas trade has been subdued. Over the year, the dollar price of gold is up 10.4% from January 1, and silver is up a miserly 1.26%. However, this is mostly down to dollar weakness, with gold performing not nearly so well measured against other currencies, as our next chart shows.

In Japanese yen, gold is up 5.9%, in sterling 1.6%, and in euros down 2.3%. For the retail investment market, it has been a boring year, and it’s hardly surprising that the punters have had more excitement in cryptocurrencies. In Chinese yuan, gold is up barely 1% and in Indian rupees its lost 0.7%, yet physical demand from these countries continues apace. Holders of silver bullion in these currencies are faced with net losses.

Our third chart shows how the swap dealers on Comex have closed their net gold positions.

On 12 December, the swaps (as proxy for the bullion banks) in aggregate were net long 12,278 gold contracts (the red line), and it’s quite likely their books are level on other OTC derivative markets, or perhaps even net long as well. This is necessary for their trading strategy going into 2018, when shortages of physical bullion, and/or weakness in the dollar, might begin to drive the price. In silver, swaps are net long 8,877 contracts.

For the bullion banks trading on Comex ,it has been a good jobbing market. They are now in a position to run prices up, probably quite rapidly to avoid getting too short. In silver, the managed money category is net short, and outright shorts are over 50,000 contracts, representing one third of annual mine output. In gold, money managers are still net long 76,226 contracts, so the potential for a bear squeeze is not so marked as it is in silver.

The physical market must have drained significant quantities of bullion away from Western vaults. Shanghai Gold Exchange withdrawals this year (as proxy for public demand) will total over 2,000 tonnes, and Indian demand looks like being a further 1,000 tonnes. Other Asian countries are also keen importers. Global supply is about 3,300 tonnes, so even allowing for scrap supply in China, deep storage gold in the West is being sold and supplied to Asia.

This has been going on for the last five years, at least, and cannot go on for ever. Perhaps renewed weakness in the dollar, coupled with rising commodity prices driven by China, might throw this supply/demand equation into sharp relief in 2018.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.