Malthusian dogma and circumlocution

Oct 27, 2022·Alasdair MacleodThe Cato Institute recently published a new book, Superabundance, which tries to prove that Malthus, the nineteenth century clergyman and economist, was wrong with respect to his theory of population. Malthus believed that population growth was exponential, while the growth of food supplies and other commodities was linear. These conditions, he held, were bound to lead to famine, wars, and eventually for populations to decline and die off.

Malthus wrote his essay on the subject in 1798. For over two centuries of massive population expansion and profligate use of natural resources, his prophecies have failed to materialise.

You would think that a new book on the subject would be superfluous, but the authors appear to be at least partly motivated by the climate change debate, arguing that the same psychology of fear of the future applies.

However, there are areas of significant doubt in this book. There is a contradiction between the initial section on human psychology, and the data-based approach to ascertaining changes in the abundance of commodities over time.

This article raises and addresses these issues, and proposes a far simpler and more convincing approach, rejecting the use of adjusting fiat currencies to determine prices and using real, legal money — which is gold.

[Superabundance: The Story of Population Growth, Innovation, and Human Flourishing on an Infinitely Bountiful Planet, by Marian Tupy and Gale Pooley — Published by the Cato Institute]

Introduction

The objective of this article is to illustrate common analytical errors committed by economists and historians of all stripes. The easiest target for such an exercise is socialist establishment figures. But the problem with incorrect analysis extends even to free marketeers. All too often you witness those sympathetic with a reduction in government intervention in the economy lauding statistical and macroeconomic analysis, oblivious to the pitfalls and contradictions. It is this approach which needs to be challenged, and free market think tanks, such as the Cato Institute should be made aware of the errors in this approach.

The heart of the problem is that deductive reasoning has been discarded in favour of an evidence-based approach. The issue with evidence is two-fold. The first is its veracity: how often do we see analysts sitting back and considering whether statistics emanating from government agencies are accurate? And the second is the error of projecting statistical trends mathematically in an environment determined entirely by unmathematical human action.

The evidence-based approach is very much associated with modern economists, both Keynesian and monetarist. But there has been a longer trend towards it driven by the evolution of mathematics and the natural sciences. Human sciences are not natural sciences, yet even economists sympathetic to free markets continue to make the mistake of treating economics as a natural science.

To stimulate an awareness of this problem, in this article I review Superabundance, a new book by Gale Pooley and Marion Tupy, published by the Cato Institute, which seeks to prove that Thomas Malthus, who argued that populations would grow beyond the ability of the planet to sustain them, was wrong. If a publisher is going to publish a book on this rather tired subject, it would pass the editorial process easily if one of the authors was a senior fellow in your own think-tank, and the other a university professor who has taught economics and statistics. Both authors qualify: Tupy is the man from Cato, and Pooley the university professor.

Apart from the many tables of data listed as appendices — but who reads appendices, let alone data in tables — it is a deceptively easy read. It is written and organised in a way that makes it simple for the lay reader to follow, and it lulls the reader into thinking he, or she, comes away from the book understanding the philosophical and psychological reasons backed up by the data, why Malthus’s pessimism was wrong, the story endures, and is reflected in other aspects of human thinking where pessimism dominates.

But who would really be interested in the writings of a nineteenth century cleric, whose economic theories have become little more than an historical oddity? It soon becomes evident that the book was probably inspired by today’s obsession with climate change, nudging the reader to accept that climate change doom-mongering theories are basically a modern equivalent of Malthusian pessimism. It makes a determined effort not to challenge the climate change question head on, presumably because the authors know that they must not fall into the trap of being branded climate change deniers.

Instead, by claiming that humans are naturally scared about the future, and that psychology is a large part of modern attitudes to subjects like climate change, the book becomes relevant to a wider readership. And by way of confirmation, we find that Tupy features in YouTube videos, pointing out that the support for climate change theories is being driven by the same apocalyptic arguments promoted by Malthus.

Like Malthus’s predictions, the climate debate might be resolved in time. It is also possible that it will never be resolved if the planet heats up for reasons other than those stated by climate change apologists. Thiers is a difficult case to dislodge.

If I have a criticism of the philosophical and psychological arguments in this book as distinct from its analytical approach, it is the authors’ overreliance on quotes from philosophers and economists, ancient and modern, supplanting analysis of their own. There is no way for the reader to assess whether the quotes are selected to give the argument a bias or not. Are they a substitute for reasoning?

I raise this because, citing experts, the authors claim that “in spite of many improvements, we have evolved to focus on the negative”. I’m not convinced that this is true. Undoubtedly, for the media good news doesn’t sell copy and bad news does. But this is not to say that individuals focus on the negative. In my experience as a stockbroker, I found that humans behave differently. It has always been easier to persuade investors to buy stocks than to sell them. And, other things being equal, I find that the masses respond to economic analysis that suggests hope. But when the argument is negative the readership wanes. Instead of a propensity towards gloom, I find that people would rather dismiss it.

I fully admit the niche of gloomsters does exist. But whether they are climate activists or in a woke community, they are a hyperactive minority. Furthermore, in their psychological analysis, I find Pooley and Tupy’s arguments far from convincing generally. A far better book on this subject is one quoted in Superabundance: that is Population Bombed! By Pierre Desrochers and Joanna Szurmak (published by The Global Warming Policy Foundation), whose subtitle is “Exploding the link between Overpopulation and Climate Change”. Their book forensically examines the psychology behind the climate change movement, without resorting to tables of data. That is what this book should have done.

Fontenelle’s error

The authors cite a long-forgotten French mathematician, who over four-hundred years ago called an end to the deductive reasoning of the ancient philosophers. They write that Bernard le Bovier de Fontenelle argued that deductive reasoning had run its course and was superseded by experimentation. Experimentation presumably means an approach to science based on data.

I cannot easily find this reference, but it is probably taken out of context, partly because economics was yet to be invented as a branch of science. As a mathematician at the turn of the seventeenth and eighteenth centuries, Fontenelle was contemporary with Sir Isaac Newton, who besides his discoveries in physics laid the foundation for differential and integral calculus. It would have been an exciting time for Fontenelle, with new boundaries in his vocation being opened up, and with religious and philosophical assumptions being increasingly challenged scientifically. Mathematics was providing answers which undermined existing beliefs, so who knew what the limitations of this developing science would be.

But it was a mistake to dismiss deductive reasoning in the human, as opposed to the natural sciences. While Superabundance is about a Malthusian concept, when you start dealing with price relationships you enter the territory of economics proper and more specifically catallactics. The validity of the authors’ approach hangs on whether catallactics is a human or natural science; whether it is correct to take a mathematical approach to this branch of philosophy, or to accept it is statistically unquantifiable.

With respect to the volumes of currency and credit and their purchasing power, this is a fundamental question to be addressed in any judgement of price relationships over time. I do not claim that quantitative information lacks cognitive value. The quantity theories of the monetarists under certain circumstances can have predictive value, but they resolve only a part of the price puzzle. In order to understand the limitations of monetarism the analyst must resort to a priori, or deductive reasoning. Without deductive reasoning, catallactic relationships which always depend on human actions cannot be properly explained.

The real-world examples why this matters are numerous, but I shall give one which I researched in recent years. In 2015 I gave myself the task of resolving Gibson’s paradox. Put simply, Gibson observed that interest rates and the general price level were positively correlated. In other words, rising interest rates accompanies rising prices, and vice-versa, not as commonly understood today.

The statistical evidence clearly demonstrated that this was the case. Keynes even wrote that the observed correlation was “one of the most completely established empirical facts in the field of quantitative economics”. Unfortunately, Keynes and others were unable to explain the phenomenon, and consequently, monetary policies today ignore it.

We should be in no doubt that if in the search for an explanation, deductive reasoning had been properly pursued and the phenomenon explained, central banks would not be raising interest rates today to control inflation but would let the markets determine them instead.

Therefore, it is an error to merely dismiss deductive reasoning as the authors seem to do — they should know better. Looking at his biography, one of the authors, Gale Pooley, appears to be an economist with free market instincts. Marian Tupy is closely associated with the Cato institute, a free-market think-tank. This raises the question, that if they are advocates of free markets, what is the basis of their thinking if they dismiss reasoned argument in favour of dodgy numbers?

If privately they do understand that the statistical approach is wrong, they still seem impelled towards attempting the unachievable: to give meaning to their argument by statistical method. Even though the entire economic establishment pursues statistical method, the approach must be discouraged, because free market arguments which are based on human action must be coherent.

The problems with the data

Quoting Fontenelle, Superabundance dismisses the deductive knowledge “of the Ancients” in favour of experimentation. This leads to a conflict in the authors’ approach: Part 1 of the book argues the case from a psychological point of view, psychology being a human, and not a natural science. The authors then proceed to argue the case based on data, which, of course, is the feedstock for mathematics and the natural sciences. Clearly, they are then in thrall with Fontenelle’s experimentation approach, but they cannot have it both ways.

The authors attempt to show that far from depleting the world’s resources, the rapid population growth since Malthus’s day has failed to do so, based on how the prices for goods have changed over time. If it can be shown that prices generally have fallen relatively between times T1 and T2, then that indicates supply has increased relative to demand. And since the population has increased, demand itself must have increased, so supply has increased even faster.

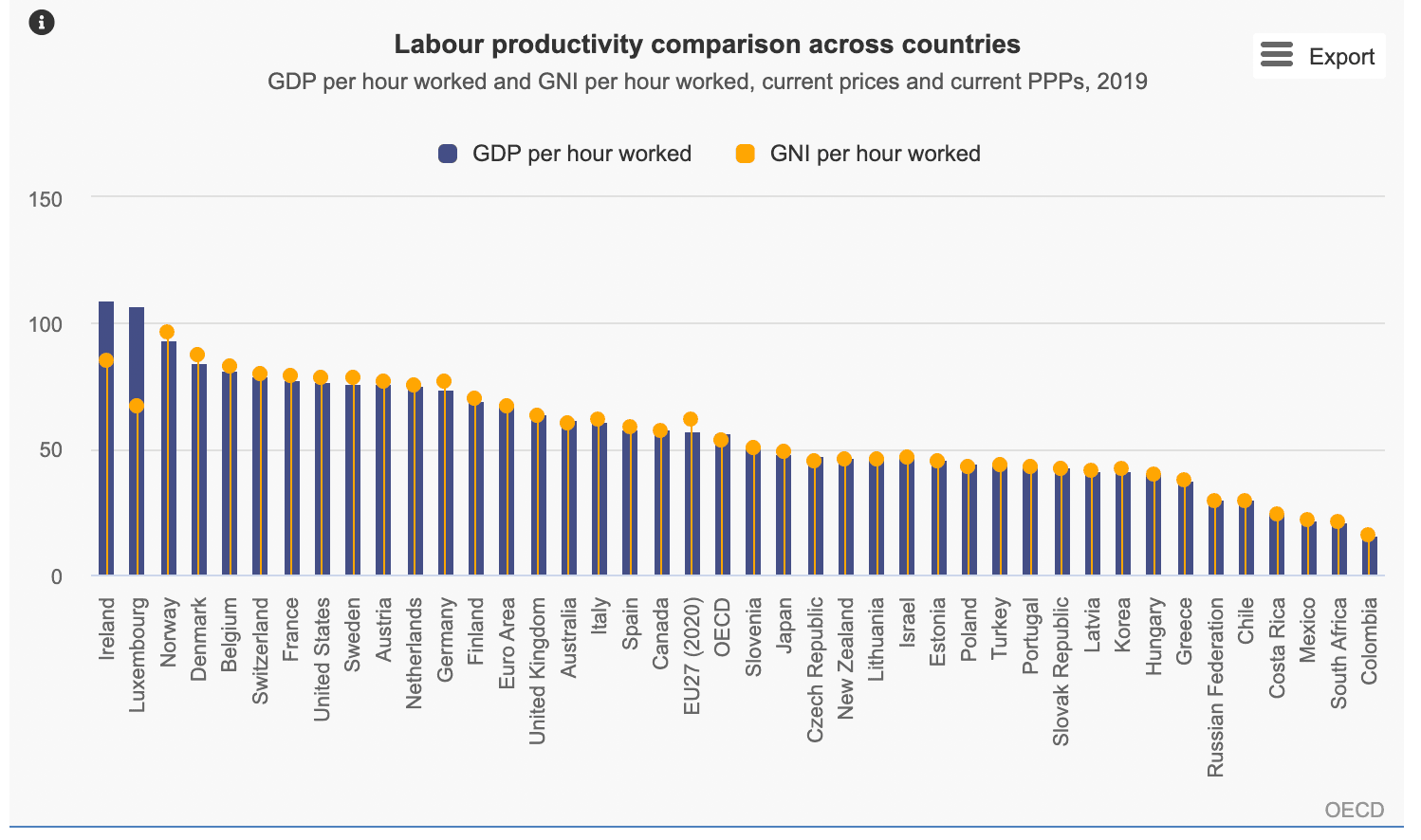

However, it is not just a simple comparison between prices at data points T1 and T2. The authors attempt to get round these problems by comparing wages and what they will buy between data points. And they then attempt to get round the problem of changes in currencies’ purchasing power by relating wages to GDP for the year in question. Appendix 2 lists the average nominal GDP per hour worked in 28 countries for each year between 1960—2018. Appendix 3 extends that to 42 countries.

The OECD data for the 42 countries in Appendix 3 for 2019, upon which the book’s data is based, is shown below.

GDP per hour worked is the same thing as the OECD’s productivity statistic. There is considerable variation between countries. But the OECD does not allow for unemployment, the numbers only including those in recorded, paid employment.

There are huge variations. Ireland, for example, is a service-based economy — tourism, financial services etc. and Luxembourg is similar. The purchase of skills involves far less raw materials than the purchase of goods. The purchase of goods is overwhelmingly the case in the poorer countries. We also know that the advanced economies as a whole, which make up well over 80% of global GDP, have seen shifts in consumer spending increasingly into services and away from commodity-based products. This trend alone casts doubt over the statistical case presented against Malthusian theory.

There is a further productivity issue. The OECD database shows that in France, for example, the average GDP per hour worked in 2019 was 77.6 on a purchasing power parity basis, in Germany 74.2, and in Britain, 64.3. But when you allow for the very high employment taxes in France, the lower employment taxes in Germany, and the even lower employment taxes in the UK, as well as the corporation tax rates in these three countries, the French employee has to produce more GDP per hour worked to justify his input. Adjusted for these factors, employing a British worker turns out to be the most profitable of the three. And anyone who goes to France will be aware that the rural economy is predominantly an untaxed cash economy, with farmers and others collecting agricultural subsidies. It’s called the French way of life and is not reflected in labour statistics.

We can begin to see serious flaws in the GDP per hour worked statistic. And the more you examine these productivity statistics, the more you realise they hardly even approximate to the truth.

Appendix 4 splits hourly income into unskilled and blue-collar compensation, going all the way back to 1850. These figures can be little more than guesswork because the assumption that government statistics were actually collected or could be derived is implausible.

So far, the earnings per hour argument is looking rather tattered.

We now move on to the spending side. The unknown after-tax portion of wages not spent on services is spent on physical goods. Appendix 6 pares down 50 commodities and raw materials into 37, based on World Bank data. Prices are taken for 1980 and 2018 for each commodity, the price increases are then compared with the GDP per hour number derived for the two dates. Since the change in the time-price value of wages is greater than the change in the commodity price, the table tells us that there is a positive compound annual percentage growth rate in “personal resource abundance”. These figures are derived for every commodity on the list to give an average.

The basic fault behind these calculations is that no consumer buys raw commodities, let alone in market-traded quantities A consumer pays for finished goods, the commodity portion being a minor element of the price when all the stages of production, margins between suppliers, wholesalers’ profits, and those of the retailers are considered. Nor can we possibly compute the changes in these variable factors over time.

Appendix 14 lists foodstuffs between 1912 (Bureau of Labor Statistics) and 2019 (Walmart prices) for the blue-collar worker. These are at least an assessment of retail prices which relate more closely to production values. But given how little workers spend on food today relative to the proportion of their earnings spent a century ago, and also changes in dietary habits, the table is of little value.

And lastly, Appendix 16 shows similar statistics for household goods between 1979 and 2019. But a dishwasher, for example, in 2019 bears very little relation to one available for purchase in 1979. And anyway, these appendices were intended to support an argument that Malthus was wrong, and that the expansion of the population would not lead to the earth’s resources running out. As end products which incorporate other costs overwhelmingly, consumer goods do not come into it.

While Pooley and Tupy could defensively claim that their statistical exercises are only illustrative and we should just get the general message they convey, it would be an admission that the statistical approach they employ is of little real value. Furthermore, promoters of the economics of free markets will find that by depending on flaky statistics and assumptions, the book’s conclusions are easily undermined and exposed to criticism from its opponents.

If the disproving of Malthus, climate change, and even macroeconomic beliefs which deny the fundamentals of human economics are to be tackled seriously without resorting to deductive knowledge alone, then there is a far simpler way to tackle the problem, leaving no holes in the argument whatsoever. This is our next topic.

Measuring commodity prices in real money

Let me introduce a real-life experience of trying to determine how prices have changed over a long period of time. Thomas Tweedie retired from a distinguished career as surgeon-general for the East India Company in Calcutta in 1844, whereupon he returned to Scotland and bought the Rachan Estate, near Peebles for £17,500.

The question as to what that sum is equivalent to one today is similar to the challenge of working out prices for commodities over a timespan, T1 and T2. As I have shown, trying to adjust a currency’s purchasing power backwards towards T1 is cumbersome, and the statistics are either not available, or if they are they are questionable. It is not the way to find an equivalent value for that sum of £17,500 today.

Fortunately, we have a simple way of solving the puzzle. In 1844, while it was presumably paid for by banker’s draft, the cost was 17,500 gold sovereigns, which were and still are legal tender. A one-pound banknote or the same credit in a bank deposit account was fully exchangeable in 1844 for one sovereign at any bank. Today, sovereigns are available at £373 each. Therefore, in today’s currency, Rachan would have cost £6,527,500.

Legally, real money, as opposed to currency and credit, is still gold not just for sterling but for the dollar and the European currencies that were absorbed into the euro. Gold has been legal money since Roman times, formalised in Justinian’s Corpus Juris Civilis in the fourth century, which consolidated Roman jurors’ findings of the previous centuries. That coin and small bars do not circulate, and that currency and credit cannot be swapped for them with the monetary authorities today does not change this fact. Nor does the authorities’ antipathy to gold, nor do government attempts to deny personal ownership of gold and gold coin change the status of gold as the only real legal money.

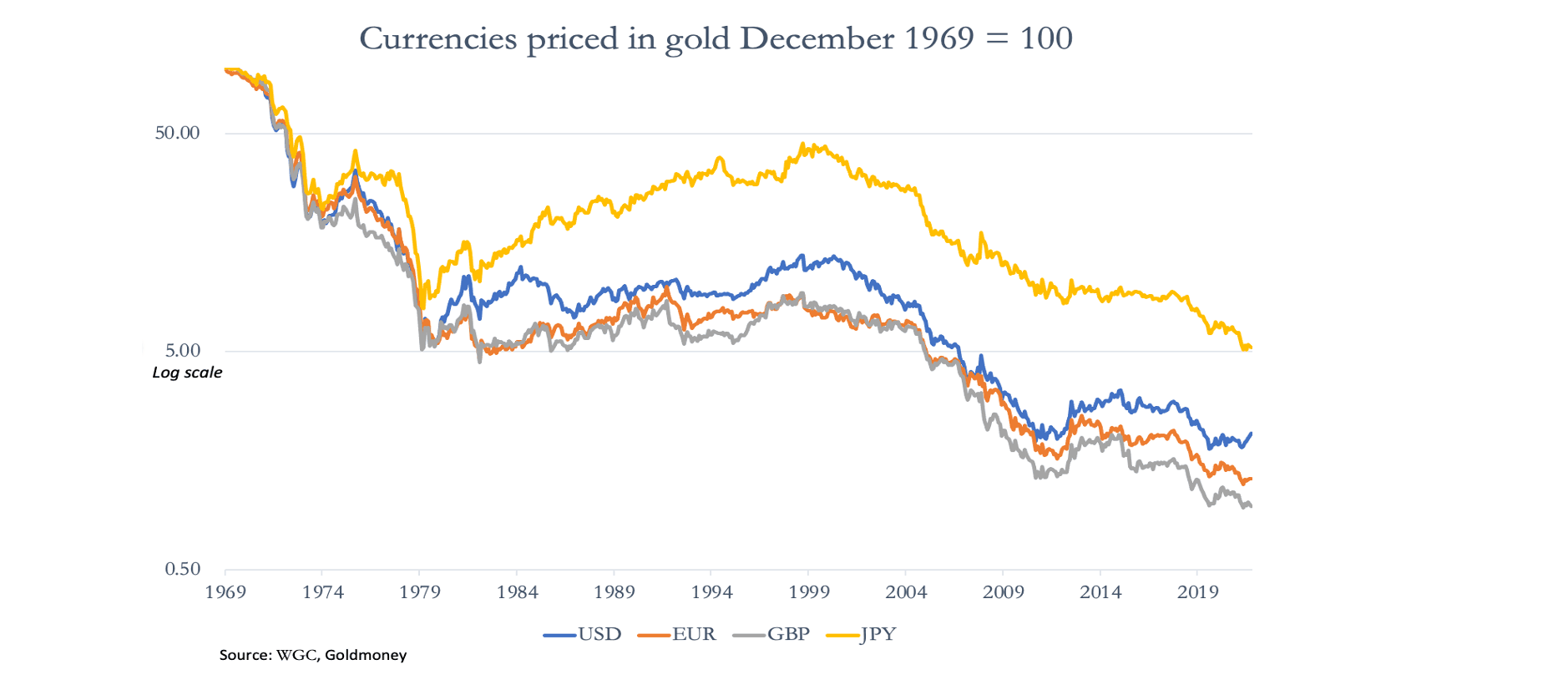

Since the Bretton Woods agreement was suspended, currency has been unanchored fiat, losing its purchasing power relative to real, legal money. The chart below shows how dramatic this loss has been since 1970, the year before Nixon suspended the Bretton Woods agreement.

The decline in the purchasing power of currencies, particularly when they became completely detached from gold, is by far the largest element affecting any price calculation over time. We know that legal money is only gold, so that we can say that sterling (in the Rachan illustration) has lost 99.2% of its purchasing power since 1970. The other currencies are similarly afflicted.

The longevity of the British sovereign coin, which has been sterling’s gold standard since 1817, makes the calculation easier in the case of sterling than for other currencies. But in an attempt to deny Malthusian economics, assessing changes in the general availability of commodities by referring to prices need not be extended over very many decades.

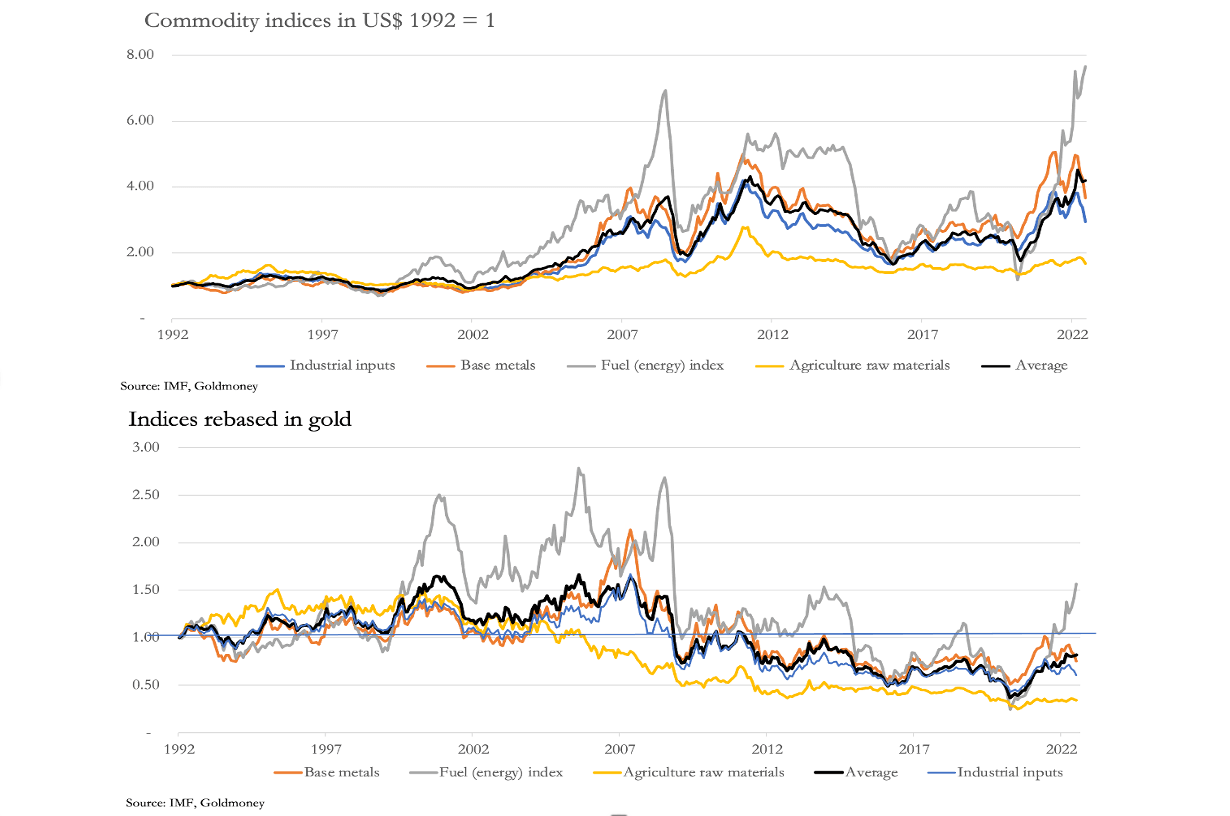

Returning to the theme of Superabundance, the purpose of the book is to illustrate that Malthusian dogma is wrong. In pursuance of this quest, the two charts below show non-cyclical resource groups, priced in dollars and in gold for the last three decades.

The upper chart shows a wide range of commodities and raw materials in IMF categories priced in US dollars. Their prices have been volatile over time, with the fuel category up 666% since 1992, and the dollar average of all groups up 320%. This is consistent with the loss of the dollar’s purchasing power.

The lower chart prices the same groups in gold. Note that the right-hand scale ranges less than half that in the upper chart. While there has been some volatility in individual categories, it is considerably less than when priced in dollars, and the average of them all is down 18% over three decades. It is the lower chart that provides evidence that priced in legal money, commodity and raw material prices as a whole have remained broadly constant over time or declined over the period. Therefore, Malthus was wrong.

But to make sure, we need to consider the expansion of above-ground gold stocks. Have they expanded less than they have in the past, pushing up the value of gold relative to commodities? It turns out to be a marginal effect, with gold stocks expanding at an average annual rate of 1.9% since 1990, compared with an average annual rate of 2.1% since Malthus’s time. Furthermore, the world’s population is estimated to have increased at about 1.6% annually on average since 1990, similar to the increase in above-ground gold stocks. Therefore, we can say that the gold supply of additional monetary metal is extraordinarily stable.

This is not to say that gold itself is free from price volatility. As we have seen with prices for energy and other commodities, currencies themselves impart volatility into them, and are certain to do the same to gold. But the point being made is that if you remove fiat currencies from the pricing of commodities and raw materials and substitute them with gold, a truer picture of commodity values emerges.

And in the context of Pooley and Tupy’s book, the answer to the Malthusian question is now properly answered.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.