When normality is exposed as a Ponzi

Mar 3, 2022·Alasdair MacleodPutin’s hubris, yes-men for generals, lack of fighting conviction among the men, poor logistics and strong Ukrainian leadership and determination have combined to turn the Russian invasion of Ukraine into a military quagmire.

Meanwhile, the West has upped the stakes in a financial war. The underlying assumption is that the Russian economy is weak and those of the Western allies are stronger. A few key metrics shows this is incorrect. The underlying resilience of the Russian economy and its financial system is not generally understood, and instead EU sanctions could end up undermining the whole euro system and the euro itself.

This article looks at how errors on the battlefield are likely to bring the financial and economic war between the West and Russia out into the open. By suspending access to them, the West has made the mistake of proving to Russia (and all other national central banks) the ultimate uselessness of currency reserves and the benefits of gold. As well as leading to the likely collapse of the entire euro system, this article explains how this financial war could end up with a de facto gold standard for the rouble and call an end for the entire fiat currency Ponzi scheme.

There is a widespread assumption that the West is playing from financial strength into Russian weakness. This is not so. The Western economic system is in a deepening crisis of its own. Accelerated currency debasement is feeding into rising prices as purchasing powers decline. At the same time, the artificial economic boost from economic and currency interventions is fading. Some say it’s stagflation. But a better description is that the West’s problems stem from monetary inflation and increasing market awareness of the hidden taxation by negative real yields on government bonds. Central banks have enough of a dilemma dealing with the fall-out from their monetary policies without seeing an acceleration of financial hostilities against anyone.

At its root, the Fed, the Bank of England, and the European Central Bank have been running a currency Ponzi scheme by issuing additional currency for their government’s benefit while claiming it is for the benefit of the people. A Ponzi scheme is a fraud that pays existing investors with funds collected from new investors. This is the US SEC’s own definition.[i] It goes on to list some red flags, most of which will be familiar to Bernie Madoff’s victims.

Talking of Bernie, older hands will remember Bernie Cornfeld and his Investors Overseas Service, who like the hedge fund managers of a later generation believed in taking his fees from the profits generated by his funds — the forerunner of two and twenty. His marketing tagline to his salesmen, “Do you sincerely want to be rich?”, was backed up by eye-watering commission rates. But in the end, the costs of maintaining all the promised returns led to Bernie’s mutual fund of mutual funds collapsing in 1970.

Though his IOS was not a Ponzi in the strict sense, Cornfeld exposed the element of human nature which is attracted by all Ponzi schemes, including currency debasement — investment greed. Greed is now deployed by central banks to keep their fiat currency debasement illusion going. Unbacked fiat currency is a Ponzi because its expansion is financed by the transfer of wealth from everyone for the supposed benefit of everyone. Think of the currency Ponzi as conning people into a financial form of perpetual motion and that’s what we now have with the global monetary and financial system.

That’s the thing about Ponzi schemes: deep down, we know that the returns can’t keep on coming, but we still buy into them for fear of missing out. Until, that is, something reverses the flow of funds, collapsing the scheme.

Today, this is the situation with the whole fiat hypothesis. It has been going in its current form since 1971, when President Nixon took the dollar off from the Bretton Woods fig leaf of a gold standard. With a few ups and downs since, now we have all bought into the dollar-based fiat Ponzi. Everyone committed to it not only “sincerely wants to be rich” but believes we can be without having to work for it.

Since the 1980s the currency Ponzi was bankrolled by the expansion of bank credit aimed at consumers and their housing until the Lehman crisis. Since then, it has been financed by central bank QE, credit expansion, and the odd helicopter drop. Today, in the wake of covid lockdowns central banks are scrambling to keep the illusion alive by printing currency even more aggressively while screwing down interest rates and bond yields.

Meanwhile, the political class has become complacent. For them, their central banks will continue to fund the state’s excess spending while maintaining monetary and financial stability. And one can easily imagine that in dealing with matters of state, central banks are no longer consulted; their support is simply assumed.

Now we face an aggressive Russia. In the West it is unwisely assumed that America, the EU, UK, and their allies can just shut Russia down by isolating it from international financing facilities. By denying access to Western currencies at the central bank level, they believe that the Russian economy will be ruined rapidly. The rouble is rubble and prices are rising. ATMs are empty and bank runs are everywhere. Putin will be forced to give in in a matter of days, or a week or two at the outside.

Putin has responded most alarmingly by announcing the mobilisation of his nuclear capability, threatening to liquidate Ukrainians and/or his Western enemies. We can only assume that won’t happen because if it does, including Putin we are all dead anyway. Instead, escalation to world war levels should be more seriously considered as being financial and economic in nature. Last weekend we saw the first financial salvos being fired by the West: sanctions against prominent Russians, withdrawal of SWIFT access for Russian banks, and cutting off Russia’s central bank from access to its currency reserves.

The risk, which is barely understood even by central bankers let alone the politicians, is that Russia has the power to reverse the flows that keep the West’s currency Ponzi alive. In this article, we look at the situation on the ground, estimate how the financial war is likely to evolve, and how the fifty-one-year fiat Ponzi we are complacently accustomed to is likely to finally collapse.

Until a few weeks ago, Putin hardly put a foot wrong with his geopolitical strategy. Like Muhammad Ali in the Rumble in the Jungle against George Foreman in 1974, Putin let America tire itself out fighting in Iraq, Syria, and Afghanistan. Ali was then able to knock Foreman out with a flurry of punches in Round 8. Putin presumably thought that Sleepy Joe Biden was similarly vulnerable, allowing his military to take out Ukraine.

Until a few weeks ago, Putin hardly put a foot wrong with his geopolitical strategy. Like Muhammad Ali in the Rumble in the Jungle against George Foreman in 1974, Putin let America tire itself out fighting in Iraq, Syria, and Afghanistan. Ali was then able to knock Foreman out with a flurry of punches in Round 8. Putin presumably thought that Sleepy Joe Biden was similarly vulnerable, allowing his military to take out Ukraine.

Big mistake. He was ignoring General von Clausewitz’s aphorism quoted above, upon which his earlier anti-American strategy was firmly based.

While NATO cannot intervene directly, it has helped Ukraine to use the Porcupine defence — so called because any animal trying to kill a slow-moving porcupine will be deterred by its sharp and painful quills. It is the principal behind guerrilla warfare and why it is successful often against well-equipped and organised forces. In Ukraine’s case, its standing army is supplemented by Molotov-cocktail throwing conscripts taking out tanks and Russian armoured carriers, many of which have reportedly run out of petrol.

In Zelensky, Ukraine has discovered an inspiring leader, rallying every able-bodied man to the national defence. Unlike Putin, he is with them fighting in the streets. Ukraine occupies the moral high ground, while the Russian squaddies are wondering why they are attacking their kith and kin. Antitank weapons, Kalashnikov rifles and a few daring fighter pilots have ensured that the more sophisticated but unmotivated Russian military force failed to take Kharkiv easily. Ukraine’s second largest city is only jogging distance from the Russian border.

Until now, Putin has never lost a war: Chechnya, Georgia, Syria, and Crimea. We are told that he sees himself as a latter-day Peter the Great, the ruthless founder of modern Russia. But military strategy today is different; you cannot dispatch a cavalry regiment into Swedish or Ottoman territory, killing the locals at random and having your men forage off the land. You must be thoroughly organised, and there is nothing more important than supply lines. Putin appears to have been let down by his own hubris, incompetent generals, and poor logistics. But if the revolting Ukrainians don’t want his troops there, Putin will find, as both Leonid Brezhnev and the Americans in Afghanistan found, that an occupation rapidly becomes untenable for the reasons so clearly laid out in the quote from von Clausewitz above.[ii]

The western media understandably points out that a military failure or even just a difficult campaign will undermine Putin’s credibility in Russia. While all reporting is partisan, the failure to take Kharkiv quickly and the way the invasion is going generally is an obvious failure.

There is a heightened risk that Putin will respond more aggressively by other means, if only to save his own skin. Perhaps it was disappointment over the slow military progress and the help being given to the Ukrainians by the West that led to his threat to deploy nuclear weapons. But “other means” are likely to be financial in nature rather than nuclear, perhaps coupled with cyber-attacks on western communications and utilities.

By all accounts, and until the Ukrainian error, Putin had been a thoroughly efficient planner. His geopolitical strategy had been impeccable. Accordingly, we should assume that the West’s sanctions, even those targeted at Russia’s Central Bank, have been anticipated, considered, and countermeasures designed — an assumption confirmed when the Russian Central Bank quickly raised interest rates and rapidly ordered restrictions on foreign currency operations, mandating at least 80% of foreign currency received from overseas trade to be sold for roubles, thereby supporting the Russian currency.

By all accounts, and until the Ukrainian error, Putin had been a thoroughly efficient planner. His geopolitical strategy had been impeccable. Accordingly, we should assume that the West’s sanctions, even those targeted at Russia’s Central Bank, have been anticipated, considered, and countermeasures designed — an assumption confirmed when the Russian Central Bank quickly raised interest rates and rapidly ordered restrictions on foreign currency operations, mandating at least 80% of foreign currency received from overseas trade to be sold for roubles, thereby supporting the Russian currency.

Naturally, a run on customer deposits at the commercial banks has developed with panicking citizens withdrawing cash roubles at ATMs. This has been countered by new restrictions on foreign currency ownership. As always, deposit liquidation exposes bank asset illiquidity, and the higher the ratio of balance sheet assets to equity the less able a bank is to withstand a run on its deposits. Western commentators are now drawing attention to this age-old problem, but in doing so they are ignoring the longstanding role of a central bank which is to always provide liquidity to an embattled banking system.

It appears that SWIFT payments and currency transfers from the Russian Central Bank’s accounts with other central banks will be permitted only for oil and gas payments. The message to Putin is “we are going to do all we can to make your life impossible, but we expect you to continue to supply us with oil and gas”. This only makes sense if the financial sanctions being put in place rapidly bring Russia to its knees, making Putin desperate for the revenue from energy exports.

What is not clear is how Russia can spend the dollars and euros earned from energy exports if payments for imported goods and services are prohibited. If that is really the case, then foreign currency is valueless in Russian hands. The thinking behind these sanctions does not therefore make sense. But in practice, SWIFT does not really matter, because there are alternative means of settlement communications between banks. What matters more is guidance for Western banks from their regulators, forcing them not to accept payments from Russian sources. And that is also bound to threaten oil and gas related transfers. “If in doubt, chuck it out…”

Furthermore, it isn’t clear why Russia needs more dollars and euros anyway. Western leaders and the financial media merely assume that the Russian kleptocracy relies on foreign currencies. This is not true. The Russian economy is reasonably healthy and stable. Income tax is a flat 13%, business regulation is light, public-sector debt is less than 20% of GDP, and the banking system is considerably healthier overall than that of its neighbours. Libertarians in the West can only dream of these conditions. The loss of all oil and gas revenue is about the only thing which would hurt Russia, but that has been exempted in the sanctions. Anyway, depending on the exchange rate, Russia’s break-even oil price is said to be below $45, less than half the current level. Or put another way, Russia can more than halve its total oil exports at current prices and still get by. The margins on natural gas are probably similar.

In any event, Russia still has China as a major market for its energy and commodities. By switching extra supplies to China, China would simply cut back on its imports from the rest of the world. Admittedly, the pipeline network to China cannot handle oil and gas volumes on the European scale, but any revenue shortfall can be made up to a degree by additional sales of other commodities.

Therefore, while obviously painful, the sanctions against Russia are unlikely to undermine its entire economy. But Russia’s response might.

Putin will have calculated that with continuing commodity sales to China and other Asian states within the Shanghai Cooperation Organisation (which represents roughly half the world’s population) that they can squeeze Europe on energy supplies for as long as it takes. European nations will have found their economies are in a vice-like grip that threatens to get even tighter. Pepe Escobar’s tweet above refers.

But as Escobar suggests, even if that is not enough, being cut off from spending or selling euros for goods and settling through SWIFT, Russia would be reasonable to request payment in gold because there would be no point in accumulating valueless Western fiat currencies. The Central bank of Russia could then exchange some of the gold for roubles to supply the economy’s need for currency as necessary without undermining its purchasing power, adding the balance to its gold reserves. This would be edging towards a de facto gold standard, which could have the merit of stabilising the rouble and putting it beyond the reach of foreign attacks. Russia’s gold strategy and its consequences are discussed more fully below.

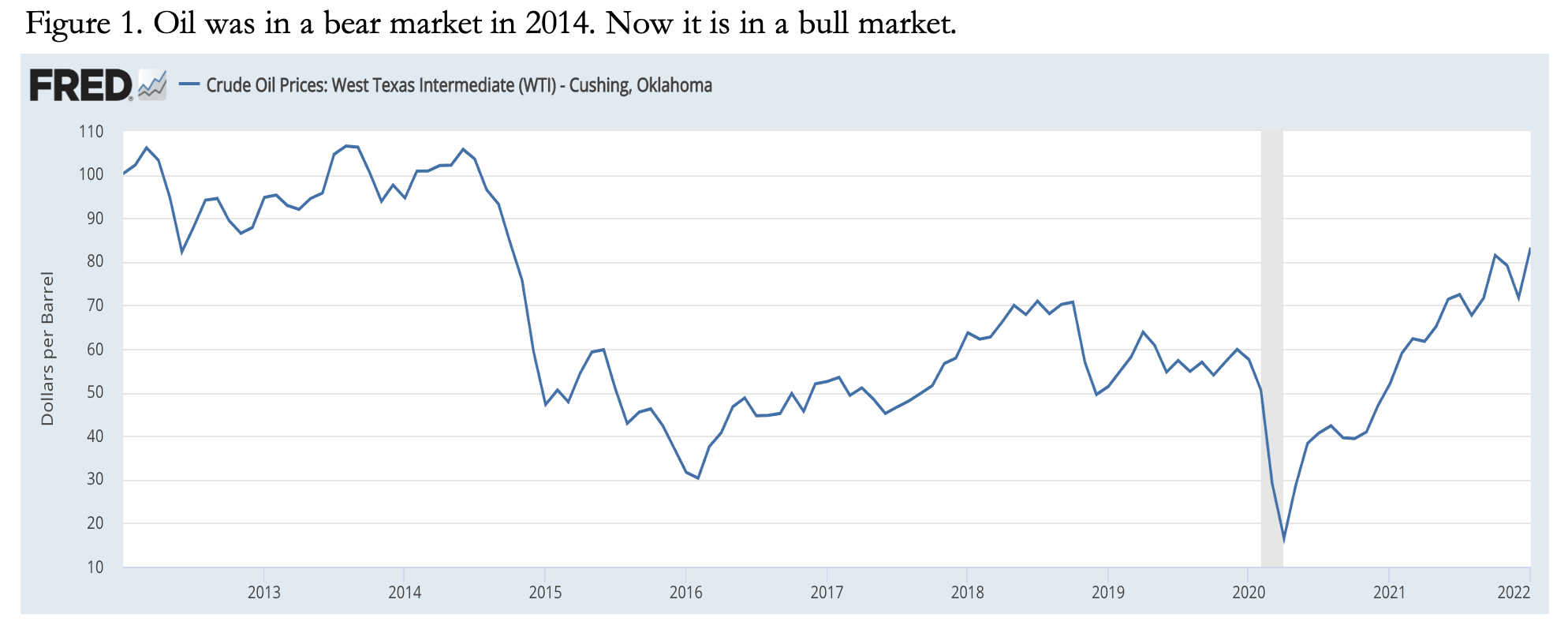

Furthermore, market conditions for energy are different from the time of the 2014 annexation of Crimea. Figure 1 shows that the oil price had peaked within three months of the annexation and that the subsequent collapse in energy prices with oil falling 70% in less than two years did enormous damage to the Russian economy.

Today, there must be no doubt that rising energy and commodity prices are driven by the exceptional rate of dollar and other fiat currency debasements since March 2020, making the oil price acutely vulnerable to further supply shocks. Think Sheik Yamani in the 1970s, when oil rose from under $3 per barrel to $28.90 at the end of the decade, and you have an indication of the peril Putin can inflict on the West and why it is a mistake to think that sanctions will repeat the 2014 squeeze on the Russian economy. This time, the squeeze will almost certainly rebound on the West.

The military failures in Ukraine and the hostile response from the West have increased the likelihood of Putin using the energy weapon against the EU. He may have miscalculated the stubbornness of Germany et al, thinking that they would prioritise their economies over political posturing. His use of the energy weapon might have been a Plan B option, but it is now increasingly likely it will be deployed following his military miscalculation.

Fortunately for Putin, in Elvira Nabiullina he has a sound economist and central banker in charge of Russia’s central bank. She was Putin’s wild-card promotion, having previously been his personal economic adviser. Since her appointment in 2013, she has overhauled the banking system and stabilised both the currency and economy in the wake of the Crimean invasion – she was not panicked by Western attempts to crash the rouble. It was undoubtedly on her advice that Putin announced measures to stabilise the currency following the restrictions announced by the EU, the US and UK earlier this week.

It would be wrong to think of her as a Putin puppet. Her body language at Monday’s meeting with Putin and other financial advisers (Figure 2) said it all. She sat at the far end of the long table, said little or nothing, avoiding eye contact. It was obvious that she was holding her own council when surrounded by Putin’s yes-men. Emphasising her qualities and command of the currency and banking system are important for our understanding why the West’s attempts to destabilise the Russian economy are likely to fail.

It would be wrong to think of her as a Putin puppet. Her body language at Monday’s meeting with Putin and other financial advisers (Figure 2) said it all. She sat at the far end of the long table, said little or nothing, avoiding eye contact. It was obvious that she was holding her own council when surrounded by Putin’s yes-men. Emphasising her qualities and command of the currency and banking system are important for our understanding why the West’s attempts to destabilise the Russian economy are likely to fail.

However, Nabiullina will almost certainly be aware of the acute fragility of the euro system. Italy’s Unicredit has had its Russian exposure of €14bn effectively frozen by Brussels. Société Générale is similarly exposed with its more highly leveraged balance sheet. Germany, Austria, and Italy’s commercial banking sectors are highly exposed as well. Additionally, if Putin proceeds with EU gas and oil restrictions, higher energy prices will increase the Eurozone’s commercial bank risks substantially. Over-leveraged banks will almost certainly require rescuing by the euro system’s central banking network.

The Eurozone’s €10 trillion plus repo market is also an acute risk factor. In-house lawyers and compliance officers at all Eurozone banks will be examining beneficial ownerships of accounts and counterparties to exclude all Russian interests. Three-party repo agents will be asked to submit counterparty details, and where Russian interests are suspected the closing leg of repos and reverse repos might be jeopardised. While financial commentators will assume that regulators will come up with solutions to settlement problems arising from these sanctions, there is a heightened risk from not only the contraction of the euro repo market, but from multiple settlement failures and the knock-on effects vividly demonstrated by the Herstatt Bank failure in 1974 — but on a far wider scale.

Trade finance and other payments are also likely to be missed or refused, which is an additional area of increasing counterparty risk. It will take very careful management by all central banks and regulators to ensure that problems in repo markets and missed settlements don’t lead to a systemic event. The chances of that working must be close to zero.

Whether Nabiullina at the RCB realises that the euro system central banking network’s liabilities already exceeds its assets due to falling bond prices and that it has nowhere to turn to for refinancing is an important consideration. This is a recent condition brought about by rising bond yields. Assuming that she is aware of it, Nabiullina will know that the immediate survival of the euro system and the euro itself will depend on her advice to Putin. Therefore, the survival of the euro system and the euro itself will be in his hands. And if the euro goes, the credibility of other fiat currencies — the dollar, pound, yen, and even the yuan — will probably be undermined subsequently as well, with a run on them from other central banks and their commercial banking networks deciding to reduce their foreign currency exposure.

Putin’s misjudgement in invading Ukrainian territory has turned him from being the ultimate national leader, a strongman and tactician in the image of Peter the Great, into yet another politician fighting for his survival. And with his firm grip on the reins of Russian power he is empowered to do anything to ensure that survival.

So it’s game on for the financial war, and possibly the end of the West’s giant fiat Ponzi scheme. In this context, we must consider the role performed by gold.

Since 2014, the gold price in dollars has risen over 60%, proving the central bank’s gold accumulation policy to have been more sensible that just switching dollars for other foreign currencies. In euros gold has risen 73% on the same timescale, because of the euro’s relative weakness to the dollar. Not only has diversification out of foreign fiat currencies been the most sensible policy, but now that access to fiat currency reserves has been compromised by foreign governments, the argument for further accumulation of Russia’s gold reserves becomes even more compelling.

Furthermore, Russia’s energy and commodity exports continue to accumulate foreign currencies, which are not really needed in the domestic economy. As pointed out above, it is essentially libertarian, with a 13% flat income tax, light regulation, and government debt at less than 20% of GDP. The only destabilising factor is bank credit, which thanks to Elvira Nabiullina’s firm stewardship at the RCB is a manageable risk. Foreign currency reserves are needed for interventionist policies, which is not Nabiullina’s style. Beyond minor amounts of foreign currency for day-to-day liquidity purposes, there is no need for them in Russia’s fundamentally free market economy.

By cutting off the RCB from its reserves, the West has made the case in Russia for gold reserves in their entirety, with only trivial amounts of foreign fiat for liquidity purposes. And the conditions necessary for tying the rouble’s liquidity to gold is partly there already. Last December, rouble currency M0 stood at $115bn equivalent while its gold reserves are valued at $141bn. Even allowing for a subsequent expansion of liquidity to support commercial banks, we can assume that official gold reserves still cover narrow measures of currency. The message sent by foreign governments and their central banks to the RCB is that to stabilise both the domestic currency and its valuation in foreign exchanges it is better to back the rouble with more gold than with increasing amounts of foreign currencies, which can always be deployed by Russia’s enemies in their attempts to undermine the rouble.

How long it will take for this penny to drop in Moscow is an intriguing question. Given the evidence of recent accumulations of gold reserves and an economy based on libertarian lines, it probably has already. The confirmation will be from all gold exports ceasing, and through friendly agents, such as the Chinese, Russia entering the bullion market to buy what it can. And as Pepe Escobar’s tweet suggests, there is always the option of only supplying energy in return for physical gold, an increasingly compelling argument. And if the Russian state has hidden bullion reserves, we can expect to have them partially or wholly revealed as well.

We can now see how the West’s financial sanctions are likely to backfire, initially destroying the euro system and its currency. The euro’s failure will undoubtedly be blamed on Putin and factors not shared by other central banks. But there is a significant risk that the euro failure will not only destabilise the global economy, but its major currencies as well. Ordinary people will then want to distance themselves from bank deposits and financial assets dependent on the continuation of the fiat Ponzi.

These messages will not be lost on other central banks, which will be re-examining their currency reserves policies. Central bank purchases of gold could increase materially, and leases and swaps where central banks are counterparties come to an end.

That being the case, are we now beginning to see a pathway through to the final destruction of unbacked fiat currencies, the ending of the fiat Ponzi, and a widespread realisation that true money, after all, is only physical gold?

[i] Investor.gov

[ii] Carl von Clausewitz was a general in the Prussian army, having served since the French revolution and through the Napoleonic Wars. The quote was in an article in the Daily Telegraph of 2 March.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.

Meanwhile, the West has upped the stakes in a financial war. The underlying assumption is that the Russian economy is weak and those of the Western allies are stronger. A few key metrics shows this is incorrect. The underlying resilience of the Russian economy and its financial system is not generally understood, and instead EU sanctions could end up undermining the whole euro system and the euro itself.

This article looks at how errors on the battlefield are likely to bring the financial and economic war between the West and Russia out into the open. By suspending access to them, the West has made the mistake of proving to Russia (and all other national central banks) the ultimate uselessness of currency reserves and the benefits of gold. As well as leading to the likely collapse of the entire euro system, this article explains how this financial war could end up with a de facto gold standard for the rouble and call an end for the entire fiat currency Ponzi scheme.

The destruction of the global fiat Ponzi scheme is a step closer

Being increasingly debased, western currencies serve to conceal deteriorating economic conditions, particularly in the US, EU, UK, and Japan. In China, less so perhaps. But China faces an old-fashioned property crisis which is sure to lead to further currency expansion and therefore, debasement of the renminbi. In this article about the state of the financial war between the US, UK and EU on one side, collectively the West, and Russia on the other, we focus on how the invasion of Ukraine is evolving into open financial warfare.There is a widespread assumption that the West is playing from financial strength into Russian weakness. This is not so. The Western economic system is in a deepening crisis of its own. Accelerated currency debasement is feeding into rising prices as purchasing powers decline. At the same time, the artificial economic boost from economic and currency interventions is fading. Some say it’s stagflation. But a better description is that the West’s problems stem from monetary inflation and increasing market awareness of the hidden taxation by negative real yields on government bonds. Central banks have enough of a dilemma dealing with the fall-out from their monetary policies without seeing an acceleration of financial hostilities against anyone.

At its root, the Fed, the Bank of England, and the European Central Bank have been running a currency Ponzi scheme by issuing additional currency for their government’s benefit while claiming it is for the benefit of the people. A Ponzi scheme is a fraud that pays existing investors with funds collected from new investors. This is the US SEC’s own definition.[i] It goes on to list some red flags, most of which will be familiar to Bernie Madoff’s victims.

Talking of Bernie, older hands will remember Bernie Cornfeld and his Investors Overseas Service, who like the hedge fund managers of a later generation believed in taking his fees from the profits generated by his funds — the forerunner of two and twenty. His marketing tagline to his salesmen, “Do you sincerely want to be rich?”, was backed up by eye-watering commission rates. But in the end, the costs of maintaining all the promised returns led to Bernie’s mutual fund of mutual funds collapsing in 1970.

Though his IOS was not a Ponzi in the strict sense, Cornfeld exposed the element of human nature which is attracted by all Ponzi schemes, including currency debasement — investment greed. Greed is now deployed by central banks to keep their fiat currency debasement illusion going. Unbacked fiat currency is a Ponzi because its expansion is financed by the transfer of wealth from everyone for the supposed benefit of everyone. Think of the currency Ponzi as conning people into a financial form of perpetual motion and that’s what we now have with the global monetary and financial system.

That’s the thing about Ponzi schemes: deep down, we know that the returns can’t keep on coming, but we still buy into them for fear of missing out. Until, that is, something reverses the flow of funds, collapsing the scheme.

Today, this is the situation with the whole fiat hypothesis. It has been going in its current form since 1971, when President Nixon took the dollar off from the Bretton Woods fig leaf of a gold standard. With a few ups and downs since, now we have all bought into the dollar-based fiat Ponzi. Everyone committed to it not only “sincerely wants to be rich” but believes we can be without having to work for it.

Since the 1980s the currency Ponzi was bankrolled by the expansion of bank credit aimed at consumers and their housing until the Lehman crisis. Since then, it has been financed by central bank QE, credit expansion, and the odd helicopter drop. Today, in the wake of covid lockdowns central banks are scrambling to keep the illusion alive by printing currency even more aggressively while screwing down interest rates and bond yields.

Meanwhile, the political class has become complacent. For them, their central banks will continue to fund the state’s excess spending while maintaining monetary and financial stability. And one can easily imagine that in dealing with matters of state, central banks are no longer consulted; their support is simply assumed.

Now we face an aggressive Russia. In the West it is unwisely assumed that America, the EU, UK, and their allies can just shut Russia down by isolating it from international financing facilities. By denying access to Western currencies at the central bank level, they believe that the Russian economy will be ruined rapidly. The rouble is rubble and prices are rising. ATMs are empty and bank runs are everywhere. Putin will be forced to give in in a matter of days, or a week or two at the outside.

Putin has responded most alarmingly by announcing the mobilisation of his nuclear capability, threatening to liquidate Ukrainians and/or his Western enemies. We can only assume that won’t happen because if it does, including Putin we are all dead anyway. Instead, escalation to world war levels should be more seriously considered as being financial and economic in nature. Last weekend we saw the first financial salvos being fired by the West: sanctions against prominent Russians, withdrawal of SWIFT access for Russian banks, and cutting off Russia’s central bank from access to its currency reserves.

The risk, which is barely understood even by central bankers let alone the politicians, is that Russia has the power to reverse the flows that keep the West’s currency Ponzi alive. In this article, we look at the situation on the ground, estimate how the financial war is likely to evolve, and how the fifty-one-year fiat Ponzi we are complacently accustomed to is likely to finally collapse.

Putin’s mistake

Until a few weeks ago, Putin hardly put a foot wrong with his geopolitical strategy. Like Muhammad Ali in the Rumble in the Jungle against George Foreman in 1974, Putin let America tire itself out fighting in Iraq, Syria, and Afghanistan. Ali was then able to knock Foreman out with a flurry of punches in Round 8. Putin presumably thought that Sleepy Joe Biden was similarly vulnerable, allowing his military to take out Ukraine.Big mistake. He was ignoring General von Clausewitz’s aphorism quoted above, upon which his earlier anti-American strategy was firmly based.

While NATO cannot intervene directly, it has helped Ukraine to use the Porcupine defence — so called because any animal trying to kill a slow-moving porcupine will be deterred by its sharp and painful quills. It is the principal behind guerrilla warfare and why it is successful often against well-equipped and organised forces. In Ukraine’s case, its standing army is supplemented by Molotov-cocktail throwing conscripts taking out tanks and Russian armoured carriers, many of which have reportedly run out of petrol.

In Zelensky, Ukraine has discovered an inspiring leader, rallying every able-bodied man to the national defence. Unlike Putin, he is with them fighting in the streets. Ukraine occupies the moral high ground, while the Russian squaddies are wondering why they are attacking their kith and kin. Antitank weapons, Kalashnikov rifles and a few daring fighter pilots have ensured that the more sophisticated but unmotivated Russian military force failed to take Kharkiv easily. Ukraine’s second largest city is only jogging distance from the Russian border.

Until now, Putin has never lost a war: Chechnya, Georgia, Syria, and Crimea. We are told that he sees himself as a latter-day Peter the Great, the ruthless founder of modern Russia. But military strategy today is different; you cannot dispatch a cavalry regiment into Swedish or Ottoman territory, killing the locals at random and having your men forage off the land. You must be thoroughly organised, and there is nothing more important than supply lines. Putin appears to have been let down by his own hubris, incompetent generals, and poor logistics. But if the revolting Ukrainians don’t want his troops there, Putin will find, as both Leonid Brezhnev and the Americans in Afghanistan found, that an occupation rapidly becomes untenable for the reasons so clearly laid out in the quote from von Clausewitz above.[ii]

The western media understandably points out that a military failure or even just a difficult campaign will undermine Putin’s credibility in Russia. While all reporting is partisan, the failure to take Kharkiv quickly and the way the invasion is going generally is an obvious failure.

There is a heightened risk that Putin will respond more aggressively by other means, if only to save his own skin. Perhaps it was disappointment over the slow military progress and the help being given to the Ukrainians by the West that led to his threat to deploy nuclear weapons. But “other means” are likely to be financial in nature rather than nuclear, perhaps coupled with cyber-attacks on western communications and utilities.

The energy price war

By all accounts, and until the Ukrainian error, Putin had been a thoroughly efficient planner. His geopolitical strategy had been impeccable. Accordingly, we should assume that the West’s sanctions, even those targeted at Russia’s Central Bank, have been anticipated, considered, and countermeasures designed — an assumption confirmed when the Russian Central Bank quickly raised interest rates and rapidly ordered restrictions on foreign currency operations, mandating at least 80% of foreign currency received from overseas trade to be sold for roubles, thereby supporting the Russian currency.Naturally, a run on customer deposits at the commercial banks has developed with panicking citizens withdrawing cash roubles at ATMs. This has been countered by new restrictions on foreign currency ownership. As always, deposit liquidation exposes bank asset illiquidity, and the higher the ratio of balance sheet assets to equity the less able a bank is to withstand a run on its deposits. Western commentators are now drawing attention to this age-old problem, but in doing so they are ignoring the longstanding role of a central bank which is to always provide liquidity to an embattled banking system.

It appears that SWIFT payments and currency transfers from the Russian Central Bank’s accounts with other central banks will be permitted only for oil and gas payments. The message to Putin is “we are going to do all we can to make your life impossible, but we expect you to continue to supply us with oil and gas”. This only makes sense if the financial sanctions being put in place rapidly bring Russia to its knees, making Putin desperate for the revenue from energy exports.

What is not clear is how Russia can spend the dollars and euros earned from energy exports if payments for imported goods and services are prohibited. If that is really the case, then foreign currency is valueless in Russian hands. The thinking behind these sanctions does not therefore make sense. But in practice, SWIFT does not really matter, because there are alternative means of settlement communications between banks. What matters more is guidance for Western banks from their regulators, forcing them not to accept payments from Russian sources. And that is also bound to threaten oil and gas related transfers. “If in doubt, chuck it out…”

Furthermore, it isn’t clear why Russia needs more dollars and euros anyway. Western leaders and the financial media merely assume that the Russian kleptocracy relies on foreign currencies. This is not true. The Russian economy is reasonably healthy and stable. Income tax is a flat 13%, business regulation is light, public-sector debt is less than 20% of GDP, and the banking system is considerably healthier overall than that of its neighbours. Libertarians in the West can only dream of these conditions. The loss of all oil and gas revenue is about the only thing which would hurt Russia, but that has been exempted in the sanctions. Anyway, depending on the exchange rate, Russia’s break-even oil price is said to be below $45, less than half the current level. Or put another way, Russia can more than halve its total oil exports at current prices and still get by. The margins on natural gas are probably similar.

In any event, Russia still has China as a major market for its energy and commodities. By switching extra supplies to China, China would simply cut back on its imports from the rest of the world. Admittedly, the pipeline network to China cannot handle oil and gas volumes on the European scale, but any revenue shortfall can be made up to a degree by additional sales of other commodities.

Therefore, while obviously painful, the sanctions against Russia are unlikely to undermine its entire economy. But Russia’s response might.

Putin will have calculated that with continuing commodity sales to China and other Asian states within the Shanghai Cooperation Organisation (which represents roughly half the world’s population) that they can squeeze Europe on energy supplies for as long as it takes. European nations will have found their economies are in a vice-like grip that threatens to get even tighter. Pepe Escobar’s tweet above refers.

But as Escobar suggests, even if that is not enough, being cut off from spending or selling euros for goods and settling through SWIFT, Russia would be reasonable to request payment in gold because there would be no point in accumulating valueless Western fiat currencies. The Central bank of Russia could then exchange some of the gold for roubles to supply the economy’s need for currency as necessary without undermining its purchasing power, adding the balance to its gold reserves. This would be edging towards a de facto gold standard, which could have the merit of stabilising the rouble and putting it beyond the reach of foreign attacks. Russia’s gold strategy and its consequences are discussed more fully below.

Furthermore, market conditions for energy are different from the time of the 2014 annexation of Crimea. Figure 1 shows that the oil price had peaked within three months of the annexation and that the subsequent collapse in energy prices with oil falling 70% in less than two years did enormous damage to the Russian economy.

Today, there must be no doubt that rising energy and commodity prices are driven by the exceptional rate of dollar and other fiat currency debasements since March 2020, making the oil price acutely vulnerable to further supply shocks. Think Sheik Yamani in the 1970s, when oil rose from under $3 per barrel to $28.90 at the end of the decade, and you have an indication of the peril Putin can inflict on the West and why it is a mistake to think that sanctions will repeat the 2014 squeeze on the Russian economy. This time, the squeeze will almost certainly rebound on the West.

The military failures in Ukraine and the hostile response from the West have increased the likelihood of Putin using the energy weapon against the EU. He may have miscalculated the stubbornness of Germany et al, thinking that they would prioritise their economies over political posturing. His use of the energy weapon might have been a Plan B option, but it is now increasingly likely it will be deployed following his military miscalculation.

The Financial War

It is generally right to assume that politicians, like their electorates, do not understand money and finance, which they delegate to central bankers who do not understand economics. If things are going to go wrong, it is likely to be in money and finance first with economic consequences to follow.Fortunately for Putin, in Elvira Nabiullina he has a sound economist and central banker in charge of Russia’s central bank. She was Putin’s wild-card promotion, having previously been his personal economic adviser. Since her appointment in 2013, she has overhauled the banking system and stabilised both the currency and economy in the wake of the Crimean invasion – she was not panicked by Western attempts to crash the rouble. It was undoubtedly on her advice that Putin announced measures to stabilise the currency following the restrictions announced by the EU, the US and UK earlier this week.

It would be wrong to think of her as a Putin puppet. Her body language at Monday’s meeting with Putin and other financial advisers (Figure 2) said it all. She sat at the far end of the long table, said little or nothing, avoiding eye contact. It was obvious that she was holding her own council when surrounded by Putin’s yes-men. Emphasising her qualities and command of the currency and banking system are important for our understanding why the West’s attempts to destabilise the Russian economy are likely to fail.However, Nabiullina will almost certainly be aware of the acute fragility of the euro system. Italy’s Unicredit has had its Russian exposure of €14bn effectively frozen by Brussels. Société Générale is similarly exposed with its more highly leveraged balance sheet. Germany, Austria, and Italy’s commercial banking sectors are highly exposed as well. Additionally, if Putin proceeds with EU gas and oil restrictions, higher energy prices will increase the Eurozone’s commercial bank risks substantially. Over-leveraged banks will almost certainly require rescuing by the euro system’s central banking network.

The Eurozone’s €10 trillion plus repo market is also an acute risk factor. In-house lawyers and compliance officers at all Eurozone banks will be examining beneficial ownerships of accounts and counterparties to exclude all Russian interests. Three-party repo agents will be asked to submit counterparty details, and where Russian interests are suspected the closing leg of repos and reverse repos might be jeopardised. While financial commentators will assume that regulators will come up with solutions to settlement problems arising from these sanctions, there is a heightened risk from not only the contraction of the euro repo market, but from multiple settlement failures and the knock-on effects vividly demonstrated by the Herstatt Bank failure in 1974 — but on a far wider scale.

Trade finance and other payments are also likely to be missed or refused, which is an additional area of increasing counterparty risk. It will take very careful management by all central banks and regulators to ensure that problems in repo markets and missed settlements don’t lead to a systemic event. The chances of that working must be close to zero.

Whether Nabiullina at the RCB realises that the euro system central banking network’s liabilities already exceeds its assets due to falling bond prices and that it has nowhere to turn to for refinancing is an important consideration. This is a recent condition brought about by rising bond yields. Assuming that she is aware of it, Nabiullina will know that the immediate survival of the euro system and the euro itself will depend on her advice to Putin. Therefore, the survival of the euro system and the euro itself will be in his hands. And if the euro goes, the credibility of other fiat currencies — the dollar, pound, yen, and even the yuan — will probably be undermined subsequently as well, with a run on them from other central banks and their commercial banking networks deciding to reduce their foreign currency exposure.

Putin’s misjudgement in invading Ukrainian territory has turned him from being the ultimate national leader, a strongman and tactician in the image of Peter the Great, into yet another politician fighting for his survival. And with his firm grip on the reins of Russian power he is empowered to do anything to ensure that survival.

So it’s game on for the financial war, and possibly the end of the West’s giant fiat Ponzi scheme. In this context, we must consider the role performed by gold.

Gold could be Russia’s strength

Since the West’s attempt to destabilise the rouble in 2014, Russia has diversified its foreign reserves, reducing its dollar exposure, increased its euro and renminbi exposure, and accumulating gold which now represents 23% of its foreign reserves, slightly more than its dollar holdings. At the Finance Ministry, the National Wealth Fund similarly has about 20% of its assets in gold (estimated to be a further 670 tonnes).Since 2014, the gold price in dollars has risen over 60%, proving the central bank’s gold accumulation policy to have been more sensible that just switching dollars for other foreign currencies. In euros gold has risen 73% on the same timescale, because of the euro’s relative weakness to the dollar. Not only has diversification out of foreign fiat currencies been the most sensible policy, but now that access to fiat currency reserves has been compromised by foreign governments, the argument for further accumulation of Russia’s gold reserves becomes even more compelling.

Furthermore, Russia’s energy and commodity exports continue to accumulate foreign currencies, which are not really needed in the domestic economy. As pointed out above, it is essentially libertarian, with a 13% flat income tax, light regulation, and government debt at less than 20% of GDP. The only destabilising factor is bank credit, which thanks to Elvira Nabiullina’s firm stewardship at the RCB is a manageable risk. Foreign currency reserves are needed for interventionist policies, which is not Nabiullina’s style. Beyond minor amounts of foreign currency for day-to-day liquidity purposes, there is no need for them in Russia’s fundamentally free market economy.

By cutting off the RCB from its reserves, the West has made the case in Russia for gold reserves in their entirety, with only trivial amounts of foreign fiat for liquidity purposes. And the conditions necessary for tying the rouble’s liquidity to gold is partly there already. Last December, rouble currency M0 stood at $115bn equivalent while its gold reserves are valued at $141bn. Even allowing for a subsequent expansion of liquidity to support commercial banks, we can assume that official gold reserves still cover narrow measures of currency. The message sent by foreign governments and their central banks to the RCB is that to stabilise both the domestic currency and its valuation in foreign exchanges it is better to back the rouble with more gold than with increasing amounts of foreign currencies, which can always be deployed by Russia’s enemies in their attempts to undermine the rouble.

How long it will take for this penny to drop in Moscow is an intriguing question. Given the evidence of recent accumulations of gold reserves and an economy based on libertarian lines, it probably has already. The confirmation will be from all gold exports ceasing, and through friendly agents, such as the Chinese, Russia entering the bullion market to buy what it can. And as Pepe Escobar’s tweet suggests, there is always the option of only supplying energy in return for physical gold, an increasingly compelling argument. And if the Russian state has hidden bullion reserves, we can expect to have them partially or wholly revealed as well.

We can now see how the West’s financial sanctions are likely to backfire, initially destroying the euro system and its currency. The euro’s failure will undoubtedly be blamed on Putin and factors not shared by other central banks. But there is a significant risk that the euro failure will not only destabilise the global economy, but its major currencies as well. Ordinary people will then want to distance themselves from bank deposits and financial assets dependent on the continuation of the fiat Ponzi.

These messages will not be lost on other central banks, which will be re-examining their currency reserves policies. Central bank purchases of gold could increase materially, and leases and swaps where central banks are counterparties come to an end.

That being the case, are we now beginning to see a pathway through to the final destruction of unbacked fiat currencies, the ending of the fiat Ponzi, and a widespread realisation that true money, after all, is only physical gold?

[i] Investor.gov

[ii] Carl von Clausewitz was a general in the Prussian army, having served since the French revolution and through the Napoleonic Wars. The quote was in an article in the Daily Telegraph of 2 March.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.