Milkshakes, Sugar Highs, and Gold: A Response to Brent Johnson’s Milkshake Theory

Mar 12, 2020·Roy SebagOn March 3, 2020, I found myself engaged in a twitter thread with Brent Johnson[1] of Santiago Capital after I had inquired into the merits of a particular investment theory which he has been promulgating over the past two years. Johnson calls his theory “The Milkshake”, and it has caused quite the swirl in contrarian economic circles.

Prior to our twitter exchange, I had heard about the “Milkshake Theory” due to Mr. Johnson’s activity on social media. However, I had never paid much close attention to the merits of this theory, as it was difficult to pin down the precise portfolio construction or statistical model which Johnson proposes. Ultimately, I was motivated to write this paper after our online discourse, when it became increasingly clear to me that Johnson advocates for a poorly conceived model founded upon unorthodox assumptions. Although it appeared to me that Mr. Johnson had not fully thought through his speculative ideas, he nevertheless felt confident enough in his universal theory to virtue signal to gold advocates such as myself. In speaking to several of our mutual friends, many share my view that, in a world awash with fiat charlatanry, Mr. Johnson is wrong to target sound money advocates as the ones proposing risky investment strategies to the global population of savers.

The Milkshake Theory as Originally Formulated is Logically Inconsistent

We begin our inquiry by attempting to analyze and understand the postulates and arguments proposed by Mr. Johnson’s Milkshake Theory. Mr. Johnson has not published any papers about his theory, so the primary sources for our adumbration are his interviews and social media exchanges. From his May 29, 2018 interview on Real Vision, I have sourced the following statements:

“The strength of the dollar is [going to] cause such chaos in the global monetary system that the safe haven that gold has always provided I think [will be in] higher demand and there will be a point where they [gold and the dollar] rise together.”

“I am not saying to go out and buy equities because things are good. I am saying go out and buy equities because things are bad; things are really bad, it’s just the road to bad looks much different than what the typical person thinks.”

The dollar, in my opinion, is going to go much, much higher over the next year to two years.”

“And so as I get into what the actual dollar milkshake theory is, it really comes down to the fact that I think the whole world is really one trade right now. And it's the trade on the dollar. Everything wraps around the dollar.”

From these statements, we can form a general understanding of the basic tenets which underlie the Milkshake Theory; these core axioms can be summarized as follows:

1. A “Strong Dollar” which is so strong that the whole world is “wrapped up” around its strength.

2. Somehow, in the face of this unprecedented dollar strength, both Gold and the Dollar rise “together”.

3. While this is happening, equity prices, measured in Dollars, also rise.

To begin with, these tenets propose various predictions without any indication of a clear time horizon.[2] This is problematic for the average investor because, while these predictions may turn out to be relatively true for some, they will simultaneously prove to be patently false for others. For an investment strategy to be coherent, it must be subject to a unified measurement at any point in time which encapsulates all proximal predictions. It is only in accordance with a clear temporal model that we can know if money invested according to the strategy is either maintaining or losing purchasing power.

Putting aside this structural issue, there is already a greater problem facing us: the way in which Mr. Johnson uses ambiguous terminology such as “dollar” and “dollar strength”. According to the presentation of his theory in interviews, the statements which comprise the core tenets of his argument are logically inconsistent.

Allow me to explain. The dollar and Gold cannot rise “together” when measured as Gold/USD. This statement, being a contradiction, is logically false. When Gold rises in dollars, the dollar is, by definition, losing purchasing power. I am not sure what kind of speculative, mental manipulation allows for Mr. Johnson to rationalize this claim, but I suspect that he may be confusing the concepts of the relative strengths between the dollar, foreign currencies, equities, and gold. This central problem will persist as an important theme as we continue our inquiry into the intelligibility and cohesiveness of the Milkshake Theory.

Again, the relationship between the dollar and gold is simple: either the dollar gains purchasing power against gold, or gold gains purchasing power against the dollar. The dollar is not defined as “a share of the S&P 500” or “equities” but, rather, it is defined as 1 unit of what it is in itself: a dollar. It is impossible, therefore, for the dollar and gold to “rise together” when gold is measured according to an inverse nominal relationship with the dollar. Despite Mr. Johnson’s insistence, premise (2) of his theory proves to be logically incoherent. We need not, however, terminate our inquiry with this basic error. Instead, I believe that I can correct the logical flaw in order to reframe and represent Mr. Johnson’s argument in the way in which it was originally intended, despite his ill-fated linguistic choices.

It appears to me that what Mr. Johnson seeks to predict with his Milkshake Theory is as follows:

A. The dollar rises relative to foreign currencies

B. The price of gold rises relative to the Dollar and foreign currencies

C. The value of equities rise relative to the Dollar and foreign currencies

D. Thus, equity values (measured against the dollar) will rise simultaneously with the price of gold (measured against the dollar, which also rises against foreign currencies).

Note that, in this reformation of the Milkshake Theory, we have eliminated the logical fallacy. We recognize that the dollar and gold cannot logically rise together; instead, we reformulate this hypothesis by proposing that it is equity values priced or measured in dollars, but not the dollar itself, which can rise simultaneously with gold. In this we see that gold and the equities can rise in relation to something else; in this case, the dollar or foreign currencies. However, the word “together” cannot be used here, as gold necessarily rises against the dollar. Furthermore, the rising of equity prices, relative to the dollar and foreign currencies, does not mean that we can conflate “equities” with “the dollar”.

In addition, Mr. Johnson often refers to a “strong dollar”. I believe that what he means by this phraseology is dollar-denominated equities. As we soon shall see, he does not merely refer to any and all equities; what he really means by “equities” is in fact the S&P 500. To simplify: the Milkshake Theory posits gold and equities rising together against all fiat currencies. Sadly, this doesn’t leave much room for a “strong dollar” which has us perplexed as to why Mr. Johnson ever chose to argue for his theory on this premise.

Now we must turn to the following question: Is it true that Gold and Equities can rise together over any meaningful period of time, say, the average savings cycle for a global citizen (35 years)? Before answering this question, we need to take a slight detour by first weighing the evidence Mr. Johnson has presented in his own attempt to answer the question.

Bad Assumptions Lead to Bad Models

As we have already mentioned, aside from the occasional interview or social media exchange, it has been difficult to ascertain the clear assumptions relating to Mr. Johnson’s model, as there exists no paper or clear investment formula proposed by him anywhere. I raised this specific point to Mr. Johnson in our Twitter exchange. In response, I was finally able to obtain some variables and logical arguments on which a model can be designed and tested. Here are Mr. Johnson’s initial axioms:

1. Mr. Johnson posits a 45-year-old earning roughly $100,000 a year with $100,000 in savings. This individual who we shall name “Jim” is able to save an additional $10,000 a year for his nest egg over a period of 20 years.

2. When Jim reaches the retirement age of 65, he no longer contributes to his savings and begins to draw down on his nest egg towards the present day. The amount Jim seeks to withdraw each year is 80% of his original earnings or $80,000 a year.

3. The question then becomes: where will be the best home for Jim’s nest egg? In the S&P500, in gold, or in a combination of both?

Now, I personally think these assumptions are fatuous and insufficient for testing the validity of the Milkshake Theory for the following reasons:

A. Our retiree Jim seems to be expecting too much from his savings program, having started to save too late (45 years) while expecting to withdraw a nominal 5x his cumulative outlay over the 20-year retirement period. I do not believe this hypothetical scenario in any way reflects the actual savings dynamic for retirees we see in the real world. Savings cycles average 35 years and not 20. Moreover, a rigorous inquiry into the history of capital markets shows that no investment program is capable of producing 5x nominal returns without significant risk or severe monetary debasement which would thereby impact the accessibility and purchasing power of any intended drawdowns.

B. The S&P 500 is a broadly US-centric index which may be accessible to US savers in the form of ETF’s or managed funds, but which remains entirely inaccessible to the majority of the world’s population. Furthermore, when foreigners purchase the S&P 500 or any US capital market asset, they are exposed to much higher transaction fees and taxes.

The retirees who I engage with every day at Goldmoney (where we oversee several pension schemes and over $400 million of assets owned by retirees) confirm points (A) and (B). What we see is that retirees begin to save sooner, they save a larger portion of their earnings, and they limit the drawdown of their nest-egg during retirement to a fixed percentage rather than a fixed dollar amount. Alas, these are the variables Mr. Johnson himself has presented, and we will work with them in order to assess whether his overarching theory is sound.

Once Mr. Johnson has put forward his initial variables, he proceeds with a crafty challenge: What would happen if this retiree invested in Gold vs. the S&P500 starting in 1991? At first, I thought Mr. Johnson was joking, having hand-picked a specific year as evidence of his universal theory, and after already having proposed highly unorthodox expectations for our retiree. My intuition was that Mr. Johnson either did not do his research, or that, by happenstance, he already knew this specific set of unrealistic, magic variables would work to advance his argument. In the world of Twitter, perhaps he assumed that I would be impressed with this demonstration. Nothing could be further from the truth. To me, this example invited more scrutiny and, from that specific moment, I have been inspired to resolve the efficacy of his claims. If Mr. Johnson’s Milkshake Theory is right, I would be happy to admit it, but only after conducting a rigorous analysis with objective modeling. Only then can we determine whether the unabashed confidence in the words and narratives argued by Mr. Johnson is grounded in historical facts that would enable us to measure his predictions into the future.

Returning to Mr. Johnson’s proof, he presents his evidence with the 1991 starting date and our hypothetical retiree Jim who begins investing according to the model proposed by Mr. Johnson.

The tables presented by Mr. Johnson immediately invoke suspicion to a seasoned security analyst. The following issues come to mind:

• What instrument is Mr. Johnson proposing the retiree own to achieve this performance? As I have previously written about, the SPY ETF was only launched in 1993. Therefore, any attempt to mirror an index performance of the S&P 500 (a mere spreadsheet), let alone generate a total return, would require some kind of fee slippage when acquiring, rebalancing, and paying other fees associated with the ownership of the underlying securities. Already, we can see that Mr. Johnson is proposing a hypothetical return which could not have been earned by our retiree Jim.

• Mr. Johnson does not include any taxation assumptions in his total return analysis. Every year of dividend reinvestment on the part of the retiree would have resulted in the paying of some portion of the dividend income as taxes, thereby reducing the principal balance rolling over. No such real-world adjustments are made by Mr. Johnson.

• Mr. Johnson does not account for any capital gains tax by the retiree as he begins to harvest his historical average cost in the S&P 500 in 2011 and onwards. This critical methodological flaw has the retiree enjoying tax-free returns on both the S&P 500 and gold.

Notwithstanding these methodological issues, it remains difficult for an intelligent investor to glean anything from a model that puts forward a thesis and then attempts to prove the theory according to one fixed set of variables - in this case, a 1991 starting point and a 45-year-old retiree with inordinate expectations. We will now correct these issues by reframing Mr. Johnson’s argument and presenting multiple proofs. In this way we will come closer towards an understanding of whether the Milkshake Theory is valid, or whether it is merely the result of a sugar high made up of untestable words and narratives.

Correcting the Milkshake Model with Multiple Proofs

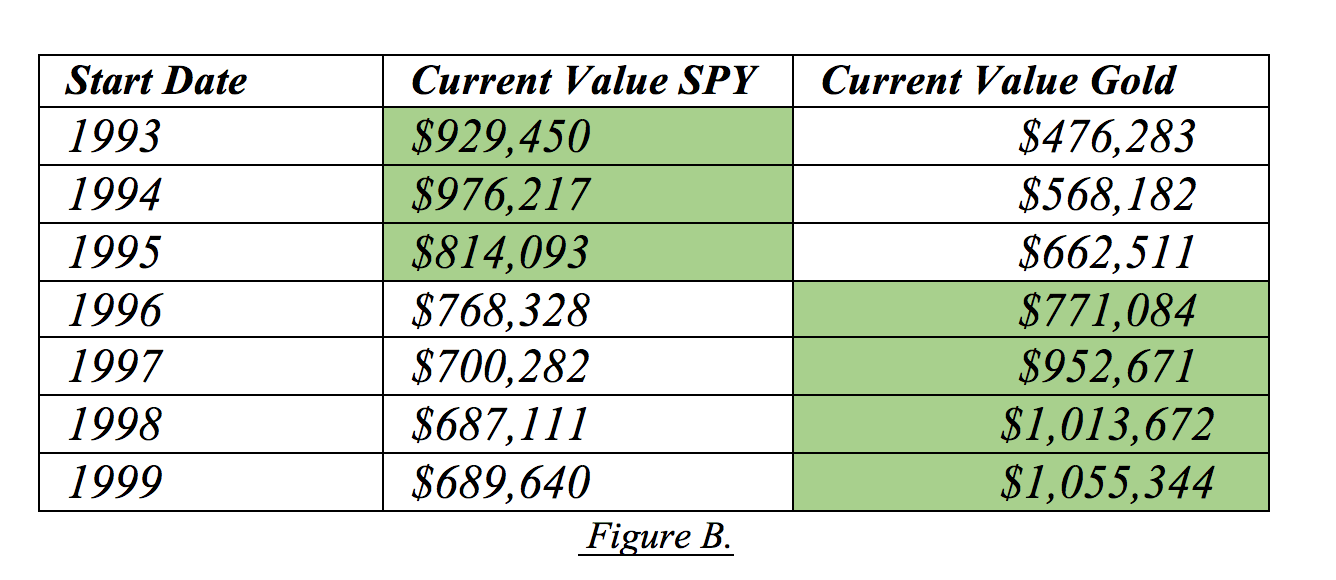

We shall now venture to provide multiple proofs for Mr. Johnson’s theory, with slight methodological improvements[3] to the integrity of the foundational model. We will do so while remaining sympathetic to the unrealistic retiree’s desires. That is to say a 45-year-old who earns $100,000 a year, is able to invest $10,000 a year for twenty years followed by an annual drawdown of the nest-egg to the tune of $80,000 a year through March 10, 2020.

The corrected model speaks for itself. What we may now clearly observe is that our retiree would have been better off investing in gold vs. the SPY in 4 out of the 7 starting years under consideration. For the gold investor, this result is achieved with far less volatility and with the benefit of the peace of mind which comes with not having to anticipate and time dividend reinvestments and taxes. All that was required of the gold investor was to start by purchasing $100,000 of metal and adding another $10,000 to this stockpile every year.

But what can we say about those three years from 1993-1995 where the SPY outperformed gold according to the methodology proposed by Mr. Johnson? Do these years provide enough basis for the Milkshake Theory to be seen as valid? Moreover, do these three years provide a rational basis for Mr. Johnson to assert that I should never advocate for 80-year-olds to own 80% of their wealth in gold?

In the final chapter of our inquiry, I will address this question by demonstrating that a holistic model premised on a global saver, a realistic savings cycle, and objective metrics that track equity price performance in Mr. Johnson’s favored dollars show that gold is unequivocally gaining purchasing power against not only the dollar, but also against the cumulative value of dollar- denominated stocks. Put simply, on a macroeconomic, concrete, and testable scale, the Milkshake Theory is wrong even when we correct for the logical fallacies in its originally formulated narrative. For the average saver around the world, gold is the best allocation that they can make - not the US dollar, not the S&P 500, not the SPY, and not even equities priced in US dollars.

The correct way to measure global equity values relative to Gold

At this stage of our inquiry, we have sufficiently proven that gold and the US Dollar cannot rise “together”. If we correct for this logical fallacy in how the Milkshake Theory is presented by assuming that the US Dollar actually means the “SPY ETF”, and if we subsequently input extremely bizarre retiree expectations, we are still presented with the fact that gold outperforms the SPY.

Needless to say, this milkshake is turning sour very quickly. But can it be rescued? To do so, we must try and find a way to demonstrate that Mr. Johnson’s central argument is valid over any meaningful period of time. And for whom? Mr. Johnson’s desire is evidently for a simple and universal model, which can be followed by anyone and measured objectively over time. Mr. Johnson clearly wishes for his theory to have universal practical import, especially considering his univocal argument that “any 80-year-old retiree anywhere should never own 80% of their wealth in gold”. To test this claim, I propose that we must incorporate the value of all global equities rather than just the SPY. In this way, we will gain a clear picture of what an average person around the world, investing in equities, and measuring that performance in dollars, would have achieved in relation to gold (also measured in dollars).

The first input we need is the value of all global equities over time. Not the index values, but the actual market cap values in US dollars. This is important as not everyone owns the indices but rather eclectic combinations of stocks constructed subjectively according to their personal financial aspirations. Sometimes the S&P 500 does well, and at other times the NASDAQ 100 does better. To think that one can handicap the long-term integrity of one index over another, as one can so easily achieve with the world’s most precious element, is a fool’s errand and, at best, it is an act of cognitive dissonance. Indices are spreadsheets with formulas that require constant rebalancing, making the challenge of mirroring an index over time to be a Sisyphean task. If you do not believe me, let me provide a few concrete examples:

• Of the 12 Original Dow Components on May 26, 1896, the last remaining component General Electric (GE) was rebalanced out in 2018. In other words, not one of the original constituents is even valuable enough to remain in the index while most of these companies have disappeared into the mists of time.

• By the end of 1929, there were 719 investment funds in existence in the United States. Today, only 6 remain in their contiguous legal structures. In other words, an actual human being could have bought and held only 6 investment funds from 1929 through March 11, 2020.

• These remaining mutual funds (MITTX, PIODX, VWELX, LOMMX, FFIDX, and DODBX) have mostly underperformed gold over their lifetime with some losing 90% or more to gold since 1971 (the date of gold’s demonetization).

The facts unequivocally show that hand-picking specific instruments and calling them broad terms such as “equities” or “US equities” results in a flawed model and hypothetical returns. We must inquire objectively into the value of all equities and see how they measure against Gold over time.

To do so, we will employ the Bloomberg World Exchange Market Capitalization in USD Index (WCAUWRLD). This index does something very simple; it merely computes the market value of every global equity listed on an exchange in US Dollar terms. Every day the new value in US Dollars gets recorded and, through this, we can track whether the wealth of global investors in equities is rising or falling in US dollars. Rather than the SPY or the NASDAQ, here we can see all the good, the bad, and the ugly from tech darlings, to failed IPO’s, to the bankrupt emerging market stocks. All of it computed as a single dollar value that can be tracked through time. Equally important is that this index allows us to test[4] another claim made by Mr. Johnson in his Milkshake Theory with the corrected logic employed: Do gold and “equities” priced in US dollars rise together?

Our results paint a dire picture for the Milkshake Theory and, more generally, for global equity investors. If we accept the corrected logic I have proposed, we do indeed see that equities and gold may rise together against the dollar. The problem, of course, is that within the same observation we can see that over a 16-year period, while equity values appear to grow nominally in dollars from $30.82 Trillion to $70.9 Trillion, the purchasing power of equities is consistently losing ground to gold, having declined from 74.13 to 42.76.

In other words, an ounce of gold owned by the average person around the world affords them more purchasing power to buy the average stock today than it did in 2014 or 2004. Conversely, an investment by an average person in the average global stock would have bought less weight of gold today than it did in 2014 or 2004. Thus, even in its correctly formulated narrative, the Milkshake Theory is self-defeating as the average investor is better off owning Gold rather than equities measured in dollars. Moreover, nowhere in our analysis and modeling do we see the “strong dollar” that Mr. Johnson is so passionate about. On the contrary, it is the structural weakness of the dollar which is necessary for the Milkshake Theory to be coherent.

Think about all those 16 years of lived experience, hard work, and savings. Think about all the failed equity investments that have come and gone. Think about all the recessions, inflations, crises, pandemics, wars, and peace. Through all of this worldly tumult, the average global saver consistently lost purchasing power when allocating to global equities rather than to gold. This is why gold always wins as a perennial store of value for man. This is why, to an average saver in the world who is 80 years old, it does make sense to own 80% of their wealth in gold over any meaningful period of time. Gold is in many ways their only method to preserve purchasing power and is far more stable than any local currency or local equity which may be accessible to them.

Conclusion

We are now at the conclusion of our inquiry. We have demonstrated through multiple proofs that the Milkshake Theory is self-defeating both in its proposed narrative and even when correctly modeling and testing its core axioms. It is an unfortunate outcome for Mr. Johnson, as the data shows that Mr. Johnson should have kept things simple by focusing on his notorious mantra: If you believe in math, buy Gold. His attempt to put forward a model which outperforms gold while somehow benefitting from timing the long-term debasement of the USD has been falsified[5]. Furthermore, this confirms that Mr. Johnson’s initial confidence was the result of bad assumptions, weakly constructed data models, and the preference of abstract theory over and above concrete testing. The work that I have completed in this paper sufficiently demonstrates that even an aggressive approach (the 80-year-old with 80% allocation to gold) is overwhelmingly superior for the majority of the global population. When eliminating hand-picked year-over-year performance and flawed retirement models, we can see clearly that gold outperforms global equity markets in USD and in all other currencies.

At Goldmoney, we do not fall prey to such intellectual foibles. Our view is that gold is money, a fact given by virtue of its physical properties and the exigencies of the natural order. We agree with the constitutional definition of a dollar, and we recognize the wisdom of our ancestors spanning 5,000 years who, for the majority of time, continuously defined money as a weight of gold or silver. Since 1971, we have observed this is no longer officially the case, even though central banks and the rich continue to unofficially treat gold as money. Since 2001, we have increasingly observed a rigged economy in the Western world: an economy which has been pushed to the very real limits of cooperative and ecological activity, and which is predicated on alchemical economic theories and abstract analyses. Since 2008, we have observed a step function in this modern approach towards money as a mere idea, the product of deleterious changing theories and the vagrancies of speculation. Consequently, we have witnessed a pronounced chasm between the real and the imaginary. As things presently stand, we have yet to identify any shift in the official approach espoused by Western economic leadership and, correspondingly, we believe this trend will continue.

Given this view, our investment philosophy has been to treat gold as money even though we live in an age where we are told it is not. That does not mean everyone should be fully preserving all of their savings in money, but it does mean that any investment theory proposed as a counterfactual should be rightly measured against gold. It also means that any prudent saver who subscribes to our philosophy should resist the tides of trend and instead allocate their nominal surplus to money which endures - that is, to gold.

[1] It is important to mention that I have great respect for Brent Johnson. He was an early supporter of BitGold, and we share many of the same friends. I also consider him a social media acquaintance and like-minded investor. My issues begin and end with the set of facts he has presented to argue his theory. Please keep this in mind while reading this paper.

[2] While Mr. Johnson mentions “one or two years” in some of his interviews. Those interviews took place in 2018. We are now two years into these predictions and Mr. Johnson continues to argue quite vehemently for the superiority of his theory. As such, I believe he has not sufficiently addressed the issue of providing a clear time horizon to measure his predictions.

[3] We use the SPY ETF rather than a hypothetical S&P 500 Total Return index value. In other words, the actual prices a retiree could have paid to acquire ownership of the underlying index. We adjust the dividend reinvestment proceeds for associated taxes using a flat 23.8% tax rate. We present every year from 1993-2000 which is the point at which the retiree would have stopped investing into the strategy. While this is not perfect and even hinders our analysis because the worst years for this model would have come later, I felt this was the correct balance. In this way, we provide a factual glimpse into what the strategy would have concretely produced for a retiree in any starting year from 1993-2000 and through to March 10, 2020, thereby capturing all the available data we have for the SPY ETF.

[4] Note how we employ indices. We do not assume that an investor bought or sold this particular index, but, rather, we are simply ingesting this data to infer a long-term trend which measures one absolute value - the value of all global equities in US dollars - versus another absolute value -that of gold priced in US dollars

[5] In a recent tweet, Mr. Johnson claimed that his current allocation to gold was only 10% begging the question whether he believes gold to be money. Afterall, if gold is money, everything else eventually depreciates in purchasing power relative to gold. If one owns just 10% of their savings in gold, they are effectively owning it as an insurance policy to cover the structural losses in purchasing power stemming from the remaining 90% of their non-gold portfolio.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.