Inflation roadmap

Dec 3, 2020·Alasdair MacleodIt is beginning to be obvious that global economic woes extend beyond covid lockdowns and that monetary inflation for the dollar, as the common foundation for other fiat currencies whose issuers face similar problems, will continue to accelerate.

Fiat currencies have only survived this long due to increased financialisation of the dollar and the US economy. Since the 1980s Wall Street has gradually dominated the US economy at the expense of Main Street. It has done so through monetary inflation, creating the conditions for the ultimate monetary collapse.

This article describes how the dollar’s collapse is likely to progress. There are two distinct aspects. The first is foreign selling, which is already becoming apparent in the weakening trade weighted index. The second is the realisation of domestic Americans that the purchasing power of their dollars will not remain stable, as the CPI suggests, but continue to decline, and that they should dispose of them sooner rather than later. There is evidence from prices of financial assets in a financialised economy that this is already beginning to happen.

Introduction

It is dawning on officials and commentators alike that the covid-19 crisis will not just go away and normality return when populations are vaccinated. The disease will be subdued, but the economic wreckage is immensely serious and long lasting. Talk of V-shaped or W-shaped recessions is increasingly being dismissed as little more than attempts to bolster consumer confidence or just wishful thinking. The damage to hospitality and retail industries is extremely serious, with bankruptcies extending to their suppliers and their supply chains as well. And it doesn’t stop with those sectors.

The global economy was already fragile, with nothing fixed by policies of extend and pretend since the Lehman crisis twelve years ago. In the advanced economies, monetary inflation has resulted in further accumulations of unproductive debt. And the greater the debt mountain, the greater the problem: modern economies have become prey to a fatal combination of profligate governments and zombie corporations managed by crony capitalists. It is a situation bound for failure, and the longer failure is put off the worse it will be.

Central to it all is an accelerating issuance of money by central banks. But the wise heads in commercial banks know they cannot be part of the solution, having already over-extended their balance sheets and are now suffering mounting bad debts. We blame the bad debts on the virus, but before the virus the global economy was already tipping into a credit-induced slump.

Have we forgotten the repo crisis, which, if nothing else, indicated that after eleven years of bank credit expansion, the banking system had run out of balance sheet capacity? Have we forgotten the trade war between the world’s two largest economies, and how that ground cross-border trade to a halt, driving exporting nations, such as Germany, into recession? And only then came the virus to deflect our attention from an already deteriorating situation.

To anyone relying on macroeconomic statistics, causes for alarm look overblown. But as Lord Canning remarked two hundred years ago, long before the modern reliance upon them, that you can prove anything with statistics — except the truth. The reality of Canning’s aphorism is set to surprise those who think GDP actually means something, and that changes in the CPI are an acceptable estimate of changes in the purchasing power of state-issued currencies.

This is the background to an acceleration of monetary inflation, which was with us long before the virus and its lockdowns. The virus merely made a deteriorating outlook even worse. As the second wave of covid-19 hits us, the full horror of the economic consequences is only now just dawning upon us. And our governments’ response can only be one: issue money without limit to stop zombie corporations from going bankrupt and to fund government deficits. Our economies are on the crumbling edge of a chasm, which without the support of increasing state intervention will fall into it. This imperative tells us that state-issued currencies are being sacrificed in a vain attempt to save us all.

Central to this sacrifice is the US dollar. As the world’s premier currency, it is the representative for all the others. If the dollar fails, the others fail. But the world’s insatiable desire for more dollars, vital for its credibility, is fading. That is the consequence of American trade protectionism and bank credit contraction replacing the previous vision of continual economic growth. All that is now history, and multinational corporations are beginning to realise it. Their need for yet more dollars is now diminishing with falling global trade prospects as America and China continue to pursue policies destructive to free trade.

International demand for dollars is reversing

In a number of recent articles, I have drawn a distinction between changes of a currency’s purchasing power emanating from the foreign exchanges and from purely domestic considerations. The motivations and reasonings of these two categories are different, and domestic users of the currency will be addressed later in this article. In the main, foreign users of the dollar are comprised of manufacturers exporting to another country including the US, businesses which will always require an element of treasury and currency management. This includes the maintenance of liquidity and the anticipation of foreign currency payments. The treasury department of a multinational corporation itself becomes a profit centre, dealing in the currencies of every country in which the corporation conducts business. And if the corporation manages its own employees’ pension fund, payment for foreign portfolio investment will usually be routed through the treasury department.

An organisation run on these lines does not take strategic positions, unlike foreign central banks and sovereign wealth funds, where politics can play a role. But it would be hard to refute the charge that as well as running a balanced position, corporate treasurers are tempted to speculate with their currency positions in order to generate extra profits. These speculations are normally in the more liquid currency and derivative markets. Nowhere is this speculation greater than in dollar exposure, where, according to the latest available figures from the US Treasury TIC system (for August) foreigners own an estimated $28.6 trillion, $22 trillion of which is invested in US long-term securities, an increase of $3.1 trillion since March.[i] The balance is in cash and short-term Treasury and commercial bills.

Of that increase, $2.4 trillion was due to private sector foreign investors increasing their exposure to equities and equity funds, with a further $363bn held by foreign official sources such as the Swiss National Bank and sovereign wealth funds. But adjusted for the performance of US equities, either private sector foreign-owned equities significantly underperformed the S&P500 index — up only 37% compared with 50% for the index and more for NASDAQ — or they have been net sellers.

Private sector foreigners have also reduced their holdings of Treasury stock and Agency debt by £254bn, which is hardly surprising, given ultra-low yields and the weakness of the dollar. But they have increased holdings of corporate debt, one assumes because of the attraction of higher yields, or just as likely, by investing in loans with an equity entitlement attached.

In addition to long-term financial investments, by August foreigners owned $6.6 trillion of dollar bank deposits and short-term bills, which together with the long-term investments described above totalled $28.6 trillion. This remarkable figure is about 140% of current US GDP and is easily the largest numerical displacement from national currencies into a foreign currency ever recorded.

The behaviour of these foreign private sector investors is likely to determine the near-term course of financial asset prices as well as the future exchange rate for the dollar, so it is essential to look at the dollar’s prospects from their perspective.

Future trade prospects

It will shortly be dawning on foreign corporations that the counterpart to the massive increase in US budget deficits will be a broadly matching increase in the trade deficit — unless, of course, there is a substantial change in US consumer savings habits. But that is discouraged by the Keynesians in charge of economic policy, because it is only by maintaining current spending that a consumer recession can be avoided. This leaves enormous potential for foreign manufacturers to increase sales into US markets.

The other side to this benefit is a predicted increase in dollar balances in the hands of the treasury departments of non-US multinationals, already overexposed to dollars. And with interest rates close to zero, the penalty cost of selling those anticipated extra dollars for forward settlement is unusually low. It will become increasingly clear to those looking at international trade opportunities in a post-pandemic trading environment that international markets will be flooded with more dollars, and that the wise course would be to sell them for forward settlement ahead of the event.

The dollar is already hitting three-year lows, as Figure 1 shows. And if there is a glut of anything in the foreign exchanges, it is of dollars.

State actors view the situation differently, and most of them are pro-dollar, maintaining them as the core of their foreign currency reserves. The exceptions are found in Asia, with China pushing for her yuan to be more accepted for international trade settlement. But having had little alternative China itself has maintained large dollar reserves. Russia, which earns dollars through energy exports has been pursuing a policy of adding to its gold reserves at the expense of dollars. Iran has been frozen out of dollars. With the exception of India — which is fence-sitting with not enough gold at the state level and with a history of strongly pro-Keynesian economic policies — the Shanghai Cooperation Organisation, its associate and observer members, are firmly in China’s camp with a growing preference for gold and yuan for their foreign reserves.

While the dollar still dominates international trade settlement, the Asian tide is turning against it. The big dollar earners, and therefore funders of US Government debt, are based in the region. In particular, China has changed her approach from exporting to America to placing a greater emphasis on encouraging her consumers to consume. In doing so, she has changed her currency intervention policy, allowing the yuan to rise against the dollar. At the same time, she has sold dollars for stockpiles of raw and industrial metals, sending a clear signal where her preferences lie, and that she is a further seller of dollars and dollar bonds.

China is emerging as the new key player in an American hegemonic world, deserting the dollar and dollar denominated debt while the rest of the world is awash with dollars. Couple this with the prospect of an accelerating dollar supply as the trade deficit grows, being twin to the US budget deficit, and a dollar crisis is in the making.

In certain respects, the dollar is in the same position as the Icelandic kroner in 2008. Two years before, Iceland’s trade deficit had shot up to 20% of GDP, and led by Fitch, rating agencies began to change their ratings to negative. Previously available financing became more expensive. And when the Lehman crisis hit, global economic confidence in Iceland evaporated and banks, attempting to preserve their own balances sheets and liquidity, suddenly attempted to withdraw their exposure to Iceland.

Iceland’s three major banks were massively overextended, having balance sheet assets about ten times Iceland’s GDP. Even though their balance sheets were denominated in króna, their funding was predominantly in foreign currencies, and it was the withdrawal of this funding that collapsed the banks and the króna. Today, US funding is denominated in dollars, but since America began to rely on the maintenance of its balance of payments (i.e. trade deficits covered by inward foreign investment), like Iceland before the Lehman crisis funding it has become dependent on foreign investment.

As well as this underlying fragility for the dollar, there can be little doubt that current economic conditions are adding to the problems of foreign and domestic banks operating in dollar markets, and that a periodic crisis from a contraction of bank credit is overdue. If liquidity injections by the Fed into the repo market in September 2019 had not rescued banks from an impending liquidity crisis, a banking crisis would almost certainly be upon us by now. But since then, the situation has worsened considerably, requiring the Fed to dramatically expand its balance sheet to create extra bank reserves.

Just as Fitch rang the bell on Iceland’s crisis, one wonders at what point rating agencies will realise that the US trade deficit is now rapidly expanding and downgrade the US economic outlook. The figures are stark: the budget deficit for 2020 was estimated at $3.3 trillion — about 17% of GDP. Given there is a timing lag between the inflationary funding of a budget deficit and its re-emergence as a trade deficit, the trend emerging in the St Louis. FRED chart below is only a start.

It will shortly become clear that official estimates that the US Government’s funding deficit will stabilise later in the current fiscal year are wide of the mark. The Congressional Budget Office estimated the current 2021 fiscal deficit will be $1.81 trillion before the second coronavirus wave. That will almost certainly be a considerable underestimate. It must be admitted that other major currencies face similar problems from rapidly escalating budget deficits, but it is with dollars that the greatest imbalances lie.

To the current estimates of foreign ownership of dollars must be added the bulk of trade deficits yet to percolate through from last year’s fiscal deficit and all of the current fiscal year. The danger is that corporate treasurers in non-US multinationals will wake up to this overload of dollars at the same time and act accordingly — just as the international banks did following the Lehman Crisis with Iceland. (The krona crashed from the official peg, at 131 to the euro on 7 October 2008, to 340 in about a month.)

For now, it is inconceivable to forex traders that the dollar could suffer such a fall. Yet, the dynamics are there for them to wake up one morning and turn from complacency to panic. Whether a panic will happen out of the blue or triggered by systemic failures in payment or production chains, we shall only know in due course. For now, we can only know that a cliff edge exists.

The domestic outlook

As noted above, domestic consumers’ motivations are very different from those of actors in the foreign exchanges. After putting aside savings — today almost entirely comprised of mandated contributions into pensions schemes and insurance policies — they maintain a balance between liquidity available for spending and the purchase of goods. Changes in this balance by the population as a whole have a profound impact on prices.

Since 23 March, when the Fed’s monetary expansion was reset into hyperdrive, the sum of cash, checking and savings accounts at the banks held by domestic residents increased by just under 20% to $17.4 trillion at end-September. These balances are split between corporates and individuals, financial and non-financials, residents and foreigners. While the amounts that ended up in domestic consumers’ hands and their bank accounts cannot be known, the fact that the first stimulus included a direct cash injection into every adult’s bank account of $1200 adds to their cash balances relative to their purchases of goods. But this is only one aspect of the $2.2 trillion CARES Act, which aims to help individuals and businesses cope with the pandemic’s financial consequences.

While some people will use government sourced money to pay down debt or add to their liquidity balances, this is not typical behaviour. When economic conditions worsen, of which there can now be no doubt, not only will the bulk of the inducement to consumers to spend be spent as intended, but they will also tend to reduce their liquidity balances in favour of goods. This is because deteriorating economic conditions inevitably lead to lower cash balances being maintained. If these conditions persist, further reductions in the ratio of dollar liquidity to goods commonly purchased will simply undermine the purchasing power of the dollar to the point where it is no longer used as a medium of exchange.

These conditions are set to persist and develop with no prospect of an offsetting and sustained demand for dollars from foreign sources. Even before all the CARES Act funds have been spent, a further package is expected, to be paid for again by monetary inflation. It is quite possible that a further contribution to consumers’ bank balances will end up accelerating the disposal of money for goods, not only undermining the dollar’s purchasing power at a greater pace than the monetary expansion would suggest is reasonable, but it will intensify the feedback loops which make the inflationary degeneration almost impossible to stop.

In a modern financial economy, the first evidence of the adjustment to lower personal cash balances is seen in the increased prices of financial assets, with the exception of fixed interest bonds. Cryptocurrencies, equity markets, monetary metals, commodities and raw materials are all rising in price, a condition that can only occur as the result of monetary debasement. It is evidence that those that can are already dumping dollars for financial assets, which raises the question as to the effect on the dollar’s purchasing power of the next dose of monetary inflation.

Interest rates

When economic actors realise that monetary debasement is not a lone episode and will continue, a lender will take into account his estimation of the future depreciation of the money’s purchasing power up to when it is due to be repaid. This is the basis of time preference. Equally, a borrower will understand that when a loan matures its value expressed in goods will be somewhat lower, yielding a benefit to him. An understanding of this condition, whereby a fall in the currency’s purchasing power favours borrowers at the expense of savers needs no further explanation.

The conditions today add some complexity to this basic proposition. Thinking they are stimulating economic activity, central banks intervene to suppress interest rates, increasing the transfer of wealth from lenders to borrowers. The trick requires government statisticians to supress the evidence of increases in the general level of prices to allow capital to circulate between lenders and borrowers at suppressed interest rates.

Central banks have been pursuing policies of suppressing interest rates since the 1980s, when led by the Fed and the Bank of England, the US and UK economies began to be moved from a production to a financial basis. The financialisation of economic activity has had the effect of increasing the control of central banks over their economies, a power that has not been used wisely.

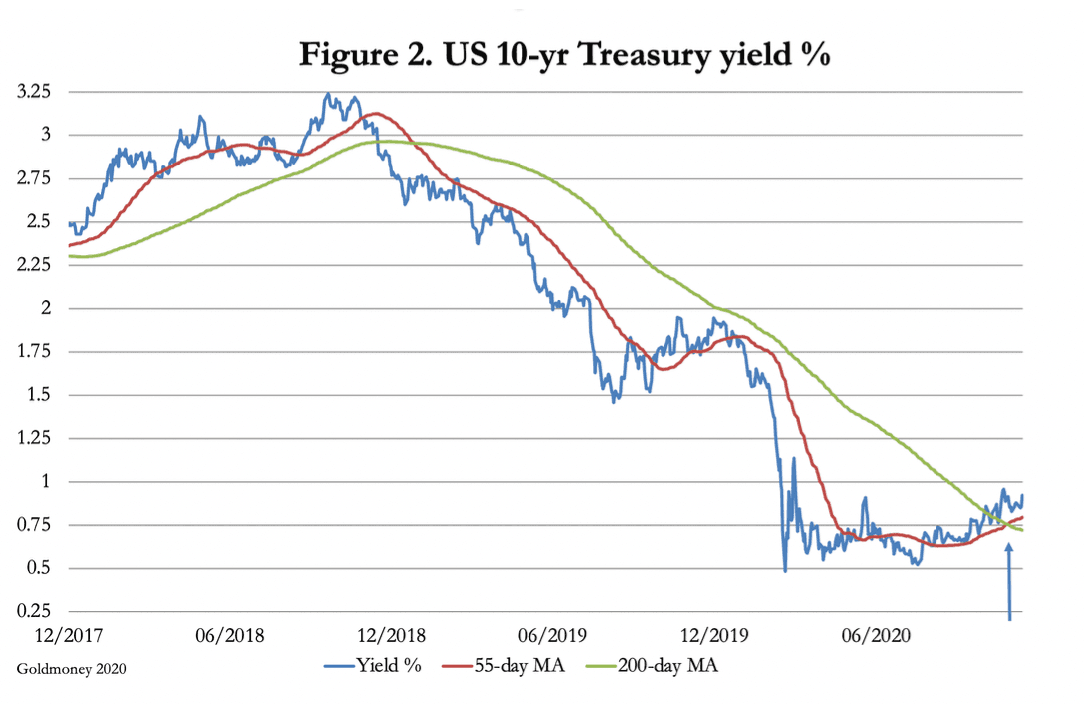

With that power has come a belief that monetary planning is the solution to everything. And as each policy step has failed in its objective, the suppression of interest rates has even taken them into negative nominal territory. Far from economic stimulation it has turned into a policy cul-de-sac; a brick wall beyond which no policy maker can travel. Because of financialisation, which has now made Wall Street considerably more important than Main Street, in economic terms the global interest rate structure has become so distorted that the rates at which savers will lend to borrowers no longer appear to matter. But with interest rate policies unable to suppress rates any further, they are finally beginning to rise. This is shown in Figure 2, of the benchmark US Treasury 10-year bond yield.

Rising yields for the benchmark 10-year UST is an early sign that the Fed is losing control over interest rates at the short end of the yield curve. Already, other than mandated pension and insurance funds, the only significant buyer of US Treasuries at these suppressed yields is the Fed.

The Fed is making the mistake of believing that having lowered its funds rate to zero and therefore the cost of borrowing they will stimulate economic activity. In fact, they stifle it, because no one in their right minds will lend money on terms where they are bound to lose. As this message becomes more widely understood and both domestic and foreign holders of dollars dispose of them instead of lending them, interest rates will rise irrespective of the Fed’s interest rate policies. They will need to rise to the level where economic actors feel they will be compensated for dollar debasement.

And here is the trap: raise the interest rate and government finances become completely undermined. The true cost of interest rate policies which support zombie corporations will also become apparent when they rise. Not only will inflationary funding become more expensive for all governments, not only will bad debts in the banking system suddenly emerge like a monster from the deep, but the increasing pace of transfers of wealth between the productive economy to the government and from saver to borrower will reveal how monetary inflation has hollowed out all aspects of the economy.

Faced with this prospect, the Fed will almost certainly refuse to raise rates sufficiently, and the dollar will continue to sink. But perhaps the decision will be taken from them: collapsing government bond prices will signal the game is up and the dollar, the reflection of full faith and credit in the US Government, will be on the way to extinction.

[i] See https://ticdata.treasury.gov/Publish/slt2d.txt

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.