Gold Price Framework Vol. 2: The energy side of the equation

May 28, 2018·Stefan WielerBuilding on our proprietary energy-proof-of-value gold price framework, we

a) present an improved gold price model;

b) provide an in-depth analysis of the energy exposure of the cost structure in gold mining and;

c) give an outlook for the gold market.

Our improved framework confirms our previous findings that energy is an important building block to understanding gold price formation. The in-depth bottom-up analysis here explains why. Given our positive forecast for longer-dated energy prices and our negative long-term view on real-interest rates, we believe that the outlook for gold prices is skewed strongly to the upside.

View the Entire Research Piece as a PDF here.

Introduction

In this report, we will dive deeper into the relationship between gold and energy, explain how energy markets work - particularly the one for oil - and discuss our views on the future outlook for energy prices and thus gold. The note is divided into three parts. In the first we revisit our gold price framework model from last year and add some important improvements. The new model has a better fit and is simpler as it requires only one step instead of two. In the second, we analyze the energy exposure of the gold mining industry, provide and in-depth look at the true energy costs of each step of the production process, confirming the strong link between energy prices and gold we found in our top down model. In the third, we take a closer look at the energy markets and the outlook for the coming years.

In our first framework note (Gold Price Framework Vol. 1: Price Model, October 8, 2015) we described in extensive detail how longer-dated energy prices are an important building block for understanding how gold prices form. Solving for gold in US dollars, we found that a majority of price movements can be explained by just a few key drivers: real-interest rate expectations, central bank policy and changes in longer-dated energy prices. Our analysis showed that changes in longer-dated oil prices are a statistically highly significant driver for changes in the price of gold. The revised model we present in part one of this note, confirms these findings with a statistical t-value of 28.0 (8.5 for the regression on y-o-y price changes) for the 5-year oil price coefficient.

Based on this framework, we then showed in our more recent report (see Inverted Asymmetry – Gold Price Outlook, September 20, 2016) that much of the increase in the gold price from $280/ozt in 2001 to $880/ozt in 2008 was driven by the rapid rise in forward energy prices (as reflected in longer-dated oil prices) and that the decline in longer dated energy prices since 2011 was a major contributor to the gold bear market from 2012-2015 (in USD terms). We concluded that we had most likely hit an inflection point for both longer-dated energy prices and real-interest rate expectations during 2016, implying that the outlook for gold became increasingly skewed to the upside.

The findings above are also consistent with our in-depth analysis of the cost side of gold producers which we present in part two of this report. It becomes obvious that gold mining is energy intensive when looking at the direct energy exposure, that is the fuel and power consumption of gold producers. Even comparably simple open pit mining consumes a lot of fuel for trucks and excavators and underground mining consumes electricity for cooling in addition to that. The processing of the gold ore is also highly energy intensive. Most large gold mining companies report these direct energy costs in one way or another. Typically these reported costs are somewhere around 15-25% of all-in operating costs at current energy prices. Our calculations show that costs are likely closer to 20-30% of operating costs.

However, this does not account for the indirect energy costs, which can be significant. Indeed, indirect energy costs are the energy cost of embedded raw materials and services needed for gold mining such as steel, chemicals, tires, cement etc. Ultimately even wages partially reflect energy costs as changes in energy prices affect the living costs such as housing and food of workers. While we do have comprehensive data for the direct energy costs, indirect energy consumption is much harder to find, much less estimate precisely, as the gold producers don’t disclose them in any form (and probably have no actual way to measure them to begin with). However, for this report, we meticulously dissected the expense side of the income statements of the largest gold producers in the world and found that on average, direct and indirect energy costs account for about 50% of the cost of gold production over the short run (meaning a change in energy prices has an almost instant impact on the cost side of gold producers). Naturally, this cost increase must be reflected in the gold price, otherwise producers are in effect operating at a loss and in turn will reduce output.

Importantly, while changes in energy spot prices change current production costs, what really matters for the price of gold are the longer-dated energy prices. Why is that? Imagine oil prices drop to USD10/bbl tomorrow because inventories reach storage capacity. Yet longer-dated oil prices remain at USD60/bbl because that is what is what the markets believes is required to ensure there is enough investment in future production capacity. So which price should be reflected in the current gold price? We believe that the forward gold price should correspond the forward oil price as that is what will determine long term production costs for gold. However, unlike oil, gold can be stored at almost no costs and there are no storage capacity constraints. Hence the gold forward curve slope is essentially a function of lease rates. If spot prices divert from that relationship it would open an arbitrage opportunity that would quickly be exploited and thus vanish. As a result, when the oil forward curve is in steep contango , the gold spot price cannot trade at corresponding discount to the gold futures prices. Hence both gold forward and gold spot prices should reflect forward oil prices, not spot prices.

While changes in energy costs impact gold mining costs by 50% over the short run, this becomes closer to 100% over the long run as rising (or occasionally declining) energy costs feed through every aspect of the economy and lead to a general price inflation. For example, when energy prices double, costs for a new excavator don’t double overnight. Some parts of the production costs for the excavator go up instantly, such as the steel, the synthetic parts and energy used in manufacturing process. But overhead costs probably don’t change that fast. Hence excavators may become instantaneously more expensive, but not 100% more expensive. In addition, the manufacturer of the excavator might not be able to pass on his increased costs to the miners straight away. Plus, a gold mining operation doesn’t need to replace its excavators all that often as heavy machinery tends to have very long lifetimes. When it purchases a new machine, it will amortize the cost over a very long time. Combined, this means that part of a gold miners costs is almost fixed over the short and medium term horizons and immune to changes in energy prices. Over time however, higher energy prices will trickle into every aspect of manufacturing. For example, as energy prices rise, building a factory becomes more expensive which over the long run will have to be reflected in sales prices. Administration costs go up as electricity, IT, phone bills, and wages and ultimately the price of every paper clip reflects higher energy prices. However, this may take years or maybe even decades to materialize.

What does that mean for gold prices? We find that gold prices only move in line with energy prices to the extent that gold producers are exposed to the instant cost change. For example, when longer dated energy prices double within a year and the average energy exposure is 50%, gold prices should go up by about 50%. But over the long run, gold prices will gradually reflect the entire price change. This is the reason oil priced in gold has remained remarkably stable over very long time periods (see Figure 1).

We would argue that, ultimately, everything is energy, and changes in energy prices – or in other others, the relative abundance/scarcity of energy2 - affect the primary industries first and from there feed into all economic activity no matter how far removed in appearance. And because gold, unlike fiat currency, is rooted in the primary industries, it will always retain a relatively stable price relationship to basic goods such as food and energy itself. This is the reason why gold is such an effective and reliable store of value throughout history, whether governments and central banks today embrace it or not.

In the third part, we build on our recently published oil report (Crude Oil – The Next 5 Years, May 14, 2018) and give an outlook what our call for rising longer-dated oil prices means for gold. We find that the asymmetric outlook for gold becomes even more skewed to the upside as both real-interest rate expectations and longer-dated oil prices are now past their inflection points.

Part 1 - Energy in the revised gold price framework

In our first framework note (Gold Price Framework Vol. 1: Price Model, October 8, 2015), we developed a gold pricing model in which we identified three main drivers for gold prices: Central bank policy (real-interest rate expectations and quantitative easing), net central bank gold sales and longer dated energy prices.

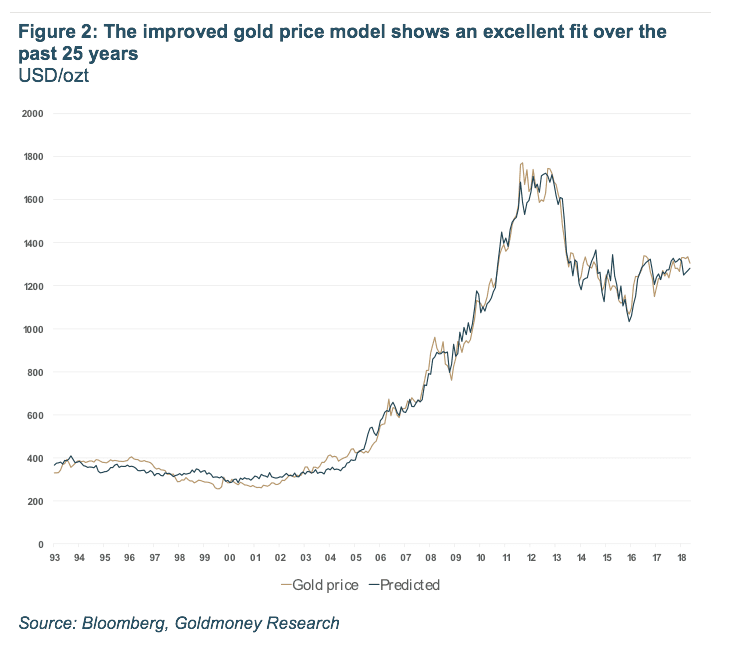

In this new report, we update our model and improve it. Specifically, we add the ECBs asset purchase program as an independent variable, as well as a variable to correct for extreme changes in longer dated energy prices and to fine-tune how real-interest rates feed into the model. As a result we get a better fit when compared to the original model and the individual variables show higher statistical significance (see Figure 2).

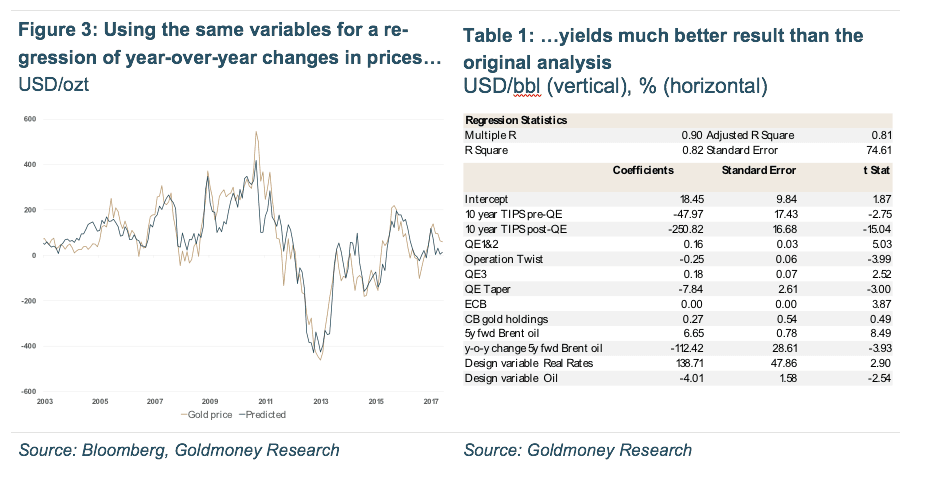

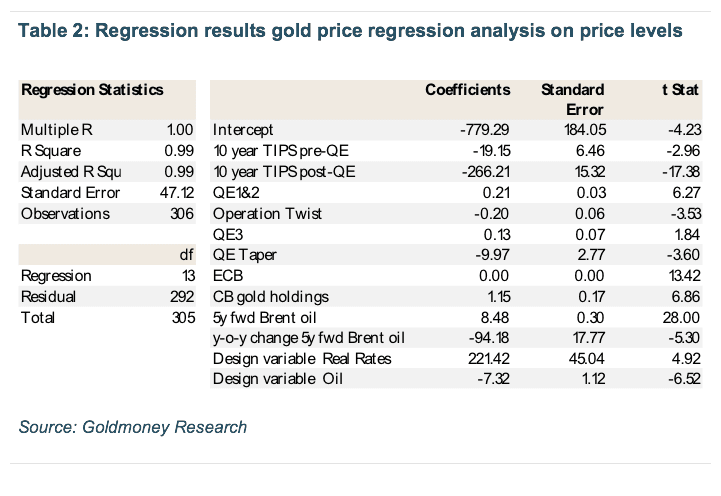

The statistical adjusted r-squared for the regression analysis (chart above) of gold price levels is 99%--the practical limit. Moreover, a simple regression analysis of the year-over-year changes in prices using the same variables has an adjusted r-squared of 81%, compared to the nevertheless significant 67% of our original work (see Figure 3 and table 1). Both the regression analysis on prices levels and year-over-year changes also predict the recent, year-to-date price moves much better than the original model, which tended to underpredict prices, implying that gold was currently overpriced by approximately USD100/ozt.

In this report we will not dive into a detailed explanation of each driver again. For that we recommend reading the original note. Instead, we will focus on the changes we made to the model.

1.1 Adding the ECBs asset purchase program as independent variable

When we first developed our model, we concentrated on the monetary policy from the US Federal Reserve. The FED began its unconventional easing policy in November 2008. QE2 followed in 2010 and QE3 in 2012 (the initial quantitative easing program would later be called QE1). By October 2014, when the FED officially halted its asset purchase program, the FEDs balance sheet had grown from roughly USD700-800 million to USD4.5 trillion. In 2011, inbetween Q2 and Q3, the FED also conducted Operation Twist, in which the Federal Reserve sold short dated Treasury bonds for longer dated ones in order to lengthen the duration of the FEDs balance sheet without altering its size.

The FEDs quantitative easing program had a huge effect on both nominal and real-interest rates. By the time the FED started the first round of QE, it had already lowered nominal interest rates (FED fund rate) to 1% and a month later it had reached zero. Yet real-interest rates (measured by 10-year TIPS yields3) were still at 2.8% in November and 2.1% in December of 2008. As the FED piled up assets on its balance sheet over the following years, both normal and real-interest rates moved gradually lower until real-interest rates hit their low at -0.8% in November 2012. Importantly, gold prices are inversely correlated to real-interest rates as we outline in detail in our original framework note. When real interest rates decline, other factors held equal, the price of gold goes up.

By buying assets, the central bank pushes real-interest rates lower, which is positive for gold prices. However, as we already realized in our original work, QE has an impact on the price of gold that far exceeds the impact it has on real-interest rates. In 2008 the average gold price was USD872/ozt and real-interest rates averaged 1.78%. By 2012 - the FED had launched its third round of QE and Operation Twist, which pushed real-interest rates down to -0.48% - the gold price had risen to USD1670/ozt. Our gold price model suggests that the move in real-interest rates (which was itself mostly driven by QE) was responsible for only about USD360 of that price move. The remaining USD390 was due to the QE policies specifically. In other words, had real-interest rates fallen to -0.48% without any QE, the peak in gold prices would likely have been USD400/ozt lower.

In our initial gold price framework, we had focused only on quantitative easing policies conducted by the FED. The rationale behind that was that QE, like real-interest rates, impact the relative value of the USD and thus the USD/gold exchange rate. More specifically, when yields of USD assets decline, gold becomes more attractive relative to holding USD. However, the reason why QE affects gold prices beyond the direct impact on real-interest rates may be that these asset purchases create additional incentives for market participants to seek alternatives as some assets are simply not available anymore in that they are held by the central bank. This effect is likely global, meaning it should not just impact gold prices in the host currency but in other currencies as well (albeit to a lesser extent). If true, this in turn means that asset purchases of foreign central banks should impact the USD/gold exchange rate as well even if the interest rate policy of these banks might not do so directly4.

We thus developed the model further by adding variables to the regression reflecting the various QE policies of major foreign central banks. We found that both the ECBs and the BOEs asset purchase program had a positive impact on the USD/gold exchange rate. However, while the ECBs QE program is statistically significant for both the regression analysis on gold price levels and year-over-year changes, the BOEs asset purchase program is not5.

We could not find a positive link between the QE policies of other central banks with gold prices. The coefficients for both the BOJs and the SNBs as set purchase programs, the two other central banks that conducted significant asset purchases over the past years, actually have a negative sign in the regression analysis. We believe this is likely due to the massive impact on currency exchange rates that occurred at the time these policies where announced. For example, the SNB began its massive QE specifically to devalue the Swiss franc and introduce a peg to the EUR, which in turn also resulted in a massive devaluation of the CHF to the USD. Hence the currency impact outweighed the impact from a possible flight to gold at the time when the SNB announced its QE. It is conceivable to assume however that the latter effect would simply manifest itself more slowly over time6.

For example, the SNBs assets purchases are, unlike those of the FED, not intended to stimulate the economy but rather to prevent a large appreciation of the currency that would in turn cause a large price deflation.. The SNBs announcement to peg the Swiss franc to the EUR at EUR/CHF 1.20, resulted in an instant currency depreciation which had a much larger effect on foreign exchange rates than on Swiss savers seeking refuge in gold. The SNB formally lifted the peg in December 2014, but soon after, it began to massively intervene once more by buying foreign assets even as the formal peg was no longer existence. This again moved the Swiss franc markedly lower while as the SNBs asset holdings continuously increased.

Over the long run, these central bank asset purchases should have the same effect on gold as the FED’s asset purchase program has. In search for yield/assets investors naturally look to alternatives and gold is clearly among these. However, in a regression analysis this is very hard to capture, which is likely the reason why both the BOJs and the SNBs asset purchase program are showing negative signs.

1.2 Real-interest rate measure

In our original model we found that real-interest rates are statistically significant in a gold price model when modeling price levels. It was harder to capture this effect in a regression analyzing month-over-month and year-over-year changes. The regression analysis on price changes yielded much better results when we used changes in gold investment demand in the form of COMEX speculative futures positions and ETF holdings as explanatory variables. In turn we showed that both COMEX net speculative positions and ETF holdings were basically a function of real-interest rates (measured as the 10-year TIPS yield). Hence the original model was a two-step model where in the first step we used real-interest rates to predict COMEX and ETF positions and in a second step we used the results to predict gold prices.

However, when working on our revised model we found that the link between real-interest rates and gold prices became much stronger in the post-credit crisis world. Hence in our revised model we used two variables for real-interest rates: real-interest rates up two the introduction of the FEDs quantitative easing in 2009 and real-interest rates post quantitative easing7. That way real-interest rates show a much higher statistical significance in the model compared to the previous model, particularly the post-QE real-interest rate coefficient. As a result, we no longer need a detour via COMEX and ETF positioning for the regression analysis of both price levels and year-over-year changes. However, using the same variables in a regression analyzing month-over-month changes gives a slightly worse fit than our original model using COMEX net spec and ETF positions) with a (still respectable) adjusted r-squared of 51% vs. previously 57%.

1.3 Variable for sharp changes in the oil price

One of the issues of the original model was that for the June 2008 – June 2009 period, the model didn’t have a great fit. The sharp changes in longer dated oil prices from USD88/bbl at the beginning of 2008 to USD141/bbl by mid-year and back down to USD63/bbl by early 2009 resulted in much higher volatility in predicted gold prices than in realized prices. A simple design variable which only has a value if year-over-year changes in longer-dated oil prices exceed a certain threshold greatly increases the fit. The rationale behind this is that gold prices do not reflect extreme changes in forward oil prices if these changes are the result of temporary imbalances in the oil futures market rather than changing long-term oil fundamentals.

What does that exactly mean? In our regression analysis we use 5-year for-ward Brent prices as a proxy for longer-dated energy prices. In our original report we explain in detail why we believe longer-dated Brent futures are a good proxy for overall longer-dated energy prices.

However, there is a caveat: Under normal conditions, longer dated oil futures reflect the market’s view on the marginal cost of future supply. For example, assume consensus expectations are that demand will grow five million b/d over the next five years and that existing production will be declining at two million b/d per year. Hence the market estimates that the oil industry must add 15 million b/d of incremental supply over the next five years in order for future supply to be able to meet future demand. Of all the projects that are currently in the pipeline and the drawing boards, the ones with the lowest production costs will be sanctioned first. The marginal project – the last project that is needed to add 15 million b/d over five years – has a breakeven price of USD50/bbl (see exhibit 5). Hence, longer-dated oil prices will have to reflect this price. If it is lower than that, not enough new projects will be started which will lead to a shortfall in the future. A price higher than that will result in too much supply coming online in the future and prices falling below the breakeven costs required. If the market suddenly concludes that decline rates are four mb/d per year instead of two mb/d, then an additional 10mb/d of future production capacity is needed. As all projects with breakeven costs under USD50/bbl have already been sanctioned, the new marginal project will have a higher breakeven cost. Hence, longer dated oil will have to rise to USD60/bbl to ensure an additional 10mb/d of future supply capacity is built.

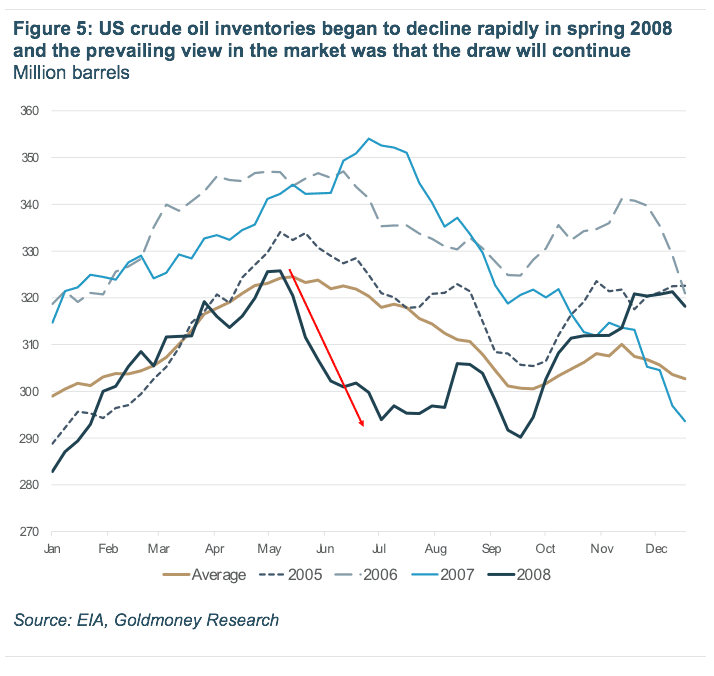

However, while in theory longer-dated future prices are set by marginal costs of future supply (and historical data is consistent with that), longer-dated fu-ture prices are also bound to simply supply and demand for these contracts. Importantly, longer dated future contracts are much less liquid than near dated futures. Hence, it takes significantly fewer contracts for longer-dated fu-tures to divert from fundamentals than at the short end of the curve. When oil spot prices rallied to USD150/bbl by July 2008, 5-year forward prices also rallied to USD140/bbl. But the marginal cost of future supply was nowhere near that level. In our view, longer-dated oil prices no longer reflected the marginal cost of future supply. Arguably there was indeed an extreme tightness in the oil market at the time. More specifically, there was a shortage of light sweet crude oil (or one can argue a shortage of heavy sour refining capacity) which lead to a dramatic decline in US and global crude oil inventories (see Figure 5). The prevailing market view at the time was that stocks would continue to decline rapidly going into fall. The coherent market response should have been for the crude oil forward curve to shift into a steeper and steeper backwardation8, pushing spot prices sharply higher. However, while the spot price did increase, so did longer dated futures. The latter was not consistent with a low and worsening inventory situation at all. Instead, the market priced in very high forward production costs but a relatively balanced current inventory situation.

Needless to say, that picture was wrong and was corrected quite quickly. The move higher in spot prices ultimately destroyed demand, which is what should happen, and prices began to decline. Later that year demand completely collapsed because of the impact of the credit crisis on economic growth. Inventories rose to multi decade highs in 2009. Importantly however, even without the dramatic impact of the credit crisis on oil demand, it is very unlikely that the tightness in the oil market would have persisted for years to come as incremental complex refining capacity and crude oil supply came online9.

So what caused then this sharp rise in the back end of curve that was seemingly inconsistent with forward fundamentals? It seems that the rally in the sport price had attracted a lot of so called “investment demand” to the back of the curve which was previously almost exclusively the domain of physical hedgers and professional commodity traders. “Investment demand” in the commodity world describes positions - predominantly long only - in the futures market that come from non-commodity specific market participants. For example pension funds, insurance companies, non-specialist hedge funds as well as retail investors.

Investment demand for commodities initially came almost exclusively via ETFs. Today some large institutional investors are trading futures directly but in many countries these investors are prohibited to enter future contracts and are require to get their exposure still via ETFs. Unlike specialist commodity traders such as hedge funds and trading houses, these market participants don’t tend to form opinions on fundamentals and position themselves accordingly; rather their commodity exposure is a strategic position in the portfolio aimed at increasing diversification and potentially an inflation hedge. Hence investment demand tends to be large and sticky. Because historically almost all investment demand was done via ETFs, investment demand was only present in the very front of the curve, where liquidity was the largest. Generally we find that the impact of investment demand on oil prices is limited, despite its size. This is because the positioning of these players is reasonably predictable: they hold futures contracts near the front of the curve and roll them into the succeeding contracts in a deterministic manner as expiry approaches. They never take physical delivery and they unwind as many positions as they enter each month. However, the back of the curve has a lot less liquidity and if investors move into the back of the curve, it can bring the supply and demand of longer dated futures out of balance.

While it is completely rational that the front end of the curve exhibited these violent price swings in 2008 as it simply reflects the changes (and to some extent expectations) in inventories, the back end of the curve should move much more gradually. If the back end of the curve would always reflect the marginal cost of future supply, then we should not witness the same price volatility as in spot prices as the underlying fundamentals don’t change that fast10. Rapid price changes in the back end therefore does most likely not just reflect a change in the market’s view of forward fundamentals. Between 2008-2009, it was likely a surge in investment demand that derailed longer-dated futures from fundamentals.

It seems that gold prices, which are driven by longer-dated oil prices rather than spot prices, were able to “look-though” this short-term price action. In other words, the gold market priced in more or less the ‘true’ marginal cost of future oil supply rather than what the futures market temporarily showed. And when prices collapsed in late 2008, the decline in the ‘true’ marginal cost of future supply was much less severe than what the futures market suggested and resulted in a much more benign decline in the price of gold. Hence gold prices didn’t follow the violent swings in longer dated energy prices to the same extent.

We would like to reiterate that the gold price framework presented in this note is not intended to be used as a trading tool. Rather than signaling whether gold is under or overpriced, the model should serve as a tool to understand what the price drivers are and where we currently stand in the cycle of these drivers. For example, we have long argued that longer-dated oil prices likely passed their inflection point a while back. Longer-dated oil prices don’t have significant downside potential from here and as we have outlined in our recent oil report, we think longer-dated oil prices must move higher over the next few years to ensure future supply. Real-interest rate expectations are in a similar situation, where we see limited upside for real-interest rate expectations even as nominal rates climb higher. This implies that the outlook for gold prices is skewed to the upside.

Over the next few weeks we will publish parts two and three of this report where we take a deep dive into the energy component of the costs of gold miners and give an outlook for gold prices based on the improved pricing framework.

1 Contango—an upward sloping future price curve--is the opposite of backwardation. In a contango term structure, spot prices trade at a discount to future prices.

2 The “price” of energy is a flawed concept because prices are usually observed in fiat currency, which does not provide a stable long-term benchmark. Over the past 100 years, energy prices in USD have gone up dramatically, but not because energy became scarcer, but because the value the USD has declined. This is true for all fiat currencies in existence. However, over those 100 years, there have been periods of energy scarcity and energy abundance, and this has an impact on the relative costs to produce gold.

3 We use the term real interest rates in this report when we actually refer to real interest rate expectations. Nominal interest rates for a given duration can be measured at any time by the yield to maturity of a bond. By buying a 10 year bond now and holding it to maturity, one knows exactly what the rate and thus the payout is. But with real interest rates it’s different as the level of inflation over the time period is not known until the period has ended. TIPS are traded and thus reflect the market’s estimates on inflation, or, to be precise, the markets estimates for the CPI over that period. But the payout of TIPS held to maturity is not known until maturity when the level of inflation measured by the CPI is known. Hence TIPS yields reflect real interest rate expectations rather than real interest rates themselves.

4 The latter could also turn out to be no longer true as ultra low, and particularly negative interest rates, might force some non-US market participants with no prior gold exposure into the only alternative to fiat. However, as with most QE conducted by central banks other than the FED, there is not enough data history yet to find any statistically significant relationship.

5 The BOEs asset purchase program might turn out to be a significant driver in a multivariate analysis at a later point when we have more data.

6 Which is difficult to proof in a multivariate regression analysis

7 Holding real-interest rate levels constant at the level of the last/first observation to fill in the blanks.

8 In a backwardated term structure, spot prices trade at a premium to future prices, the curve is downward shaped. Backwardation is typically present in a commodity market with low inventories as consumers of that commodity are willing to pay a premium for immediate delivery. Our original framework note explains backwardation and its counterpart, contango1, in detail.

9 Importantly, if the markets expectation was for future supply costs to have moved dramatically higher, then the spot prices should have been even higher than USD150/bbl. The tight inventory situation required a much steeper backwardation than what was present in the market.

10 With the exception of sudden and large moves in broad based price inflation that don’t have their origins in energy fundamentals but rather in monetary conditions.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.