Gold defies hawkish rate environment

Feb 2, 2022·GoldmoneyJanuary saw a substantial change in the markets forward view on Fed policy. Fed fund futures are currently pricing in four rate hikes over the next twelve months (see Exhibit 1), the most hawkish outlook since the onset of the pandemic that led to the fastest and largest increase in the Fed balance sheet in history.

Exhibit 1: The Fed funds futures market is now the most hawkish since the onset of the pandemic, pricing in four rate hikes over the next twelve months

Source: Goldmoney Research

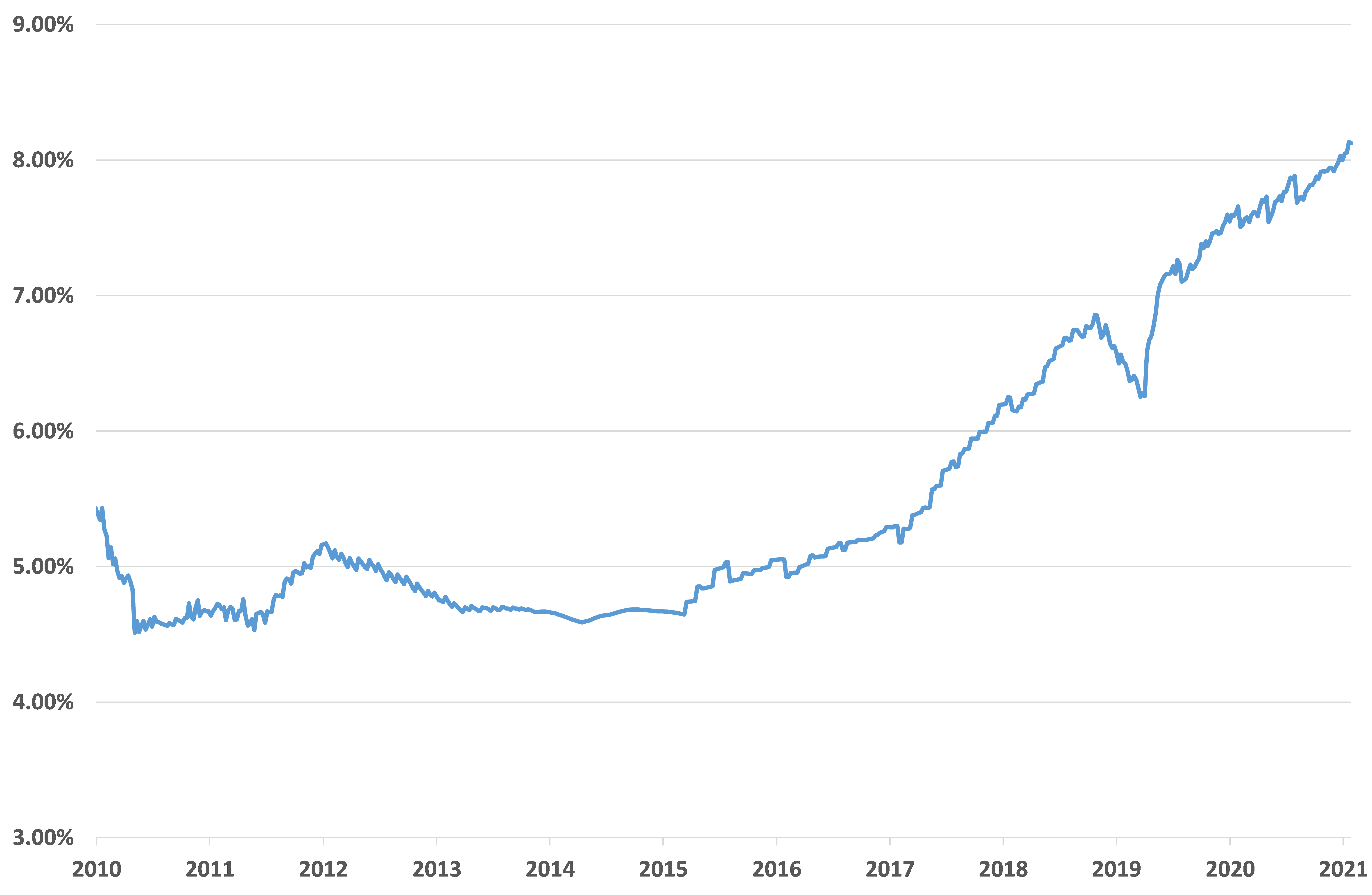

This, and the prospect that the Feds current round of quantitative easing (QE) will officially end in the near term, has led to an upward correction in both nominal yields and real-interest rate expectations. 10-year treasury yields are rapidly approaching 2%, levels not seen since summer 2019 when Fed funds rates were at 2.5%. This is a sharp rise from the 1.25% we saw in late summer last year.

Exhibit 2: Nominal interest rates are on the rise…

10-year Treasury yields, %

Source: FRED, Goldmoney Research

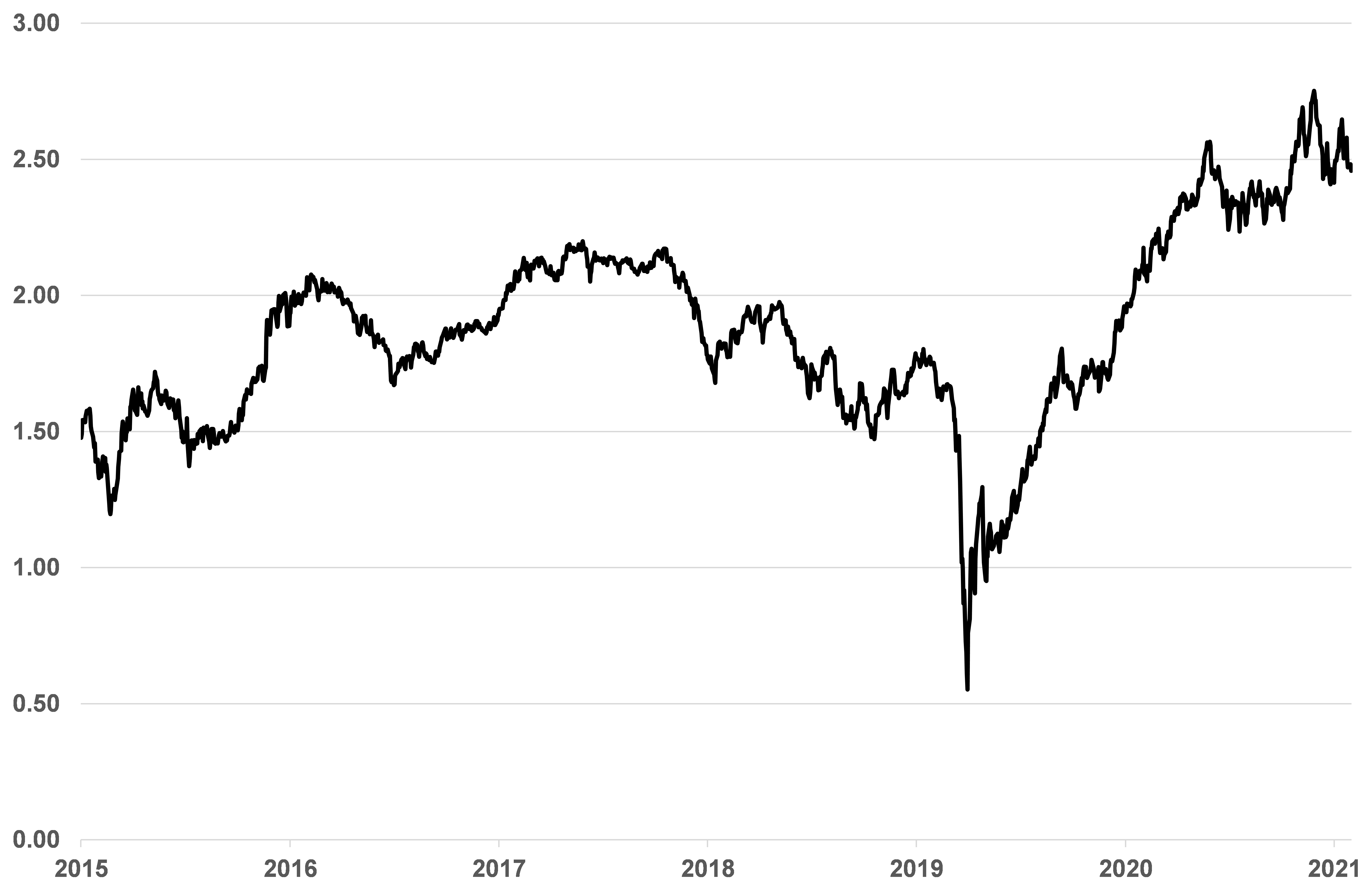

Real-interest rate expectations as reflected in 10-year TIPS yields (treasury inflation protected securities) are rising even faster, hitting -0.6%, having traded at a record low of -1.2% just two months ago.

Exhibit 3: …and real-interest rate expectations even more

10-year TIPS yields, %

The market’s reassessment of the Feds seriousness about rate hiking had a double impact on TIPS yields. On one hand it increased expectations for nominal rates. On the other hand it put a stop to the relentless rise in implied inflation expectations (breakeven inflation) we have witnessed over the past months. At least so it seems[1].

Exhibit 4: Hawkish rate prospects have put a pause on the relentless rise in breakeven inflation

10-year breakeven inflation expectation

Soruce: Goldmoney Research

In our gold price framework (Gold Price Framework Vol. 2 – The Energy Side of the Equation, May 28, 2018), we identified three main price drivers for gold prices over the long run: Central bank policy (real-interest rate expectations and quantitative easing), net central bank gold sales, and longer-dated energy prices. We found that gold prices are tracking these 3 drivers extremely well.

This raises an important question. With real-interest rate expectations rising, why haven’t gold prices corrected lower? While 10-year TIPS yields moved from an all-time low of -1.20% on 11 November 2021 to -0.6% as the time of writing, gold prices are flat (see Exhibit 5)

[1] We explain later why we think that breakeven inflation have been a poor proxy for «true» inflation expetations for the past year.

Exhibit 5: While 10-year TIPS yields increased by 60bps, gold prices are flat

In our view the answer has something to do with the recent structure TIPS market. According to data from the treasury department, TIPS account for only about 8% of outstanding US Treasury Securities. As of December 2021, there is a total of USD22tn outstanding, of which TIPS account for USD1.7tn (see Exhibit 6).

Exhibit 6: TIPS only account for around 8% of outstanding Federal debt securities

% of total outstanding treasury securities

Source: Treasury direct, Goldmoney Research

The Federal Reserve currently holds a record amount of assets overall and a record amount of treasury securities on its balance sheet. As of last Wednesday, the Fed held USD8.788tn in total assets, of which 65% were treasury securities (see Exhibit 7).

Exhibit 7: Roughly 2/3 of the assets on the Feds balance sheet are treasury securities

$ million (LHS), % of total assets held (RHS)

Source: Fred, Goldmoney Research

Importantly, while the Fed holds about 20% of all outstanding Treasuries (including TIPS), it holds an even larger share of the TIPS market. As of last Wednesday, the Fed held 27% of all outstanding treasury inflation adjusted securities. More importantly, since the beginning of the Covid19 pandemic, the Fed has been buying TIPS at a much faster rate than non-inflation adjusted treasury securities (see Exhibit 8).

Exhibit 8: The Fed has been buying TIPS at a much faster rate than nominal Treasuries

TIPS as % of Treasury Securities held by the Fed

When the Fed buys treasuries, it effectively depresses rates. If the Fed would buy TIPS at the same rate as it buys nominal treasuries, we would expect to see an equal effect on the respective yields. But as the Fed bought TIPS at a faster rate during the pandemic, it depressed TIPS yields more than nominal Treasury yields.

This impacts breakeven inflation, the difference between the yields on TIPS and Treasuries of the same maturity. Breakeven inflation is the implied 10-year inflation expectation that is embedded in TIPS. Normally, this is what the market expects for PCI inflation over the next 10 years. However, the Feds “overbuying” of TIPS resulted in overstated implied inflation expectations.

Conversely, as the Fed started to taper its asset purchasing program over the recent months, it had a more pronounced effect on TIPS yields compared to treasury yields, and thus negative effect on breakeven inflation. In our view this partially explains why 10-year breakeven inflation rates have declined over the past 2 months even as measured inflation exploded.

Inflation expectations have likely been on the rise, despite the dip in breakeven inflation

When the pandemic broke out and the Fed started buying assets at the fastest rate in history, it triggered a run on gold. Inflation expectations rose and real-interest rate expectations dropped, but gold prices rallied much more, exceeding our model-predicted prices. This exuberance was short lived though, and gold price corrected from their highs by late 2020. In the proceeding months, gold again followed our model-predicted prices. But by late spring 2022, something new happened. Despite TIPS yields moving sharply lower, gold prices remained largely flat. We think the reason is that from early 2021 onwards, gold no longer simply followed TIPS yields, but rather “true” real-interest rate expectations (which were lower than what was implied in TIPS yields). Fast forward to November 2021 when TIPS yields suddenly started to rise, gold prices remain stable as well. Again, we think gold prices followed “true” real-interest rate expectations rather than TIPS yields.

Our gold price model uses 10-year TIPS yields as a proxy for real-interest rate expectations. Thus our model also predicted much higher prices than what was observed for most of 2021, but then also predicted a sharp downward correction over the past two months on the back of rising TIPS yields (see Exhibit 10).

Exhibit 10: model predicted gold prices based on TIPS yields vs actual prices

$/ozt

Source: Goldmoney Research

To be clear, in this report we are not trying to make the argument that the markets long-term inflation expectations are correct. In fact, we find the market severely underestimates the risk that we are just at the beginning of a multi-year high-inflation cycle. What we illustrate is simply that the markets true inflation expectations were not accurately reflected in TIPS yields over the past year because the Fed distorted the TIPS market even more than the market for nominal Treasuries.

This implies that gold prices paint a much more accurate picture of the markets real-interest rate expectations than TIPS yields currently do. And what gold prices are telling us is that the market thinks long-term inflation expectations have continued to rise over the past months, contrary what 10-year breakeven inflation rates suggest.

Our medium term outlook

In our view, while the upcoming rate hikes still pose a risk for gold prices near-term, the threat will be short-lived. The relentless rise in asset prices over the past 22 months, particularly in equities, has been a direct consequence of the truly extraordinary central bank policy we have witnessed since the onset of the pandemic. This implies that reversing this policy bears an undeniable risk that these markets could crash.

In our view, there are two possible paths forward. Either the Fed treads very lightly, and manages to complete the taper and raise rates a few times without spooking equity investors too much. But the Fed will hit a hard ceiling of how far they can raise rates. We don’t expect the Fed will be able to raise rates even to the pre-pandemic highs of 2.5% of 2019. After that, it would be just waiting for the next economic downturn, which then forces the Fed to slash rates again to zero (or maybe even below) and restart QE. The other path is that the Fed more aggressively raises rates near term and even attempts to unwind the balance sheet as they panic over observed inflation. Remember, after unwinding just $700bn of assets from its balance sheet between 2018 and summer 2019, repo markets began to revolt violently, forcing the Fed to suddenly reverse course. The Fed began to buy assets faster than ever before, even faster than during the financial crisis of 2008-2009. Given that both the Feds asset holdings and stock market valuation are now significantly more elevated than when the Fed tried this the last time in 2018, we think aggressively hawkish Fed action would cause a crash in asset prices.

This would then trigger a much quicker and sharper response in Fed policy in our view. We think a lot of what is currently perceived as an economic recovery is in fact a wealth effect where parts of the population benefitted from the asset price rally. Reverse this rally and the wealth effect reverses too. Contrary to path one, we would not have to wait for the next economic downturn, the crash would cause the downturn. In our view, the Fed will not sit idle for too long this time and instead opt for a full reversal of the policies that triggered it.

We think the gold market fully agrees with that part of our view. It remains largely unimpressed with the threat of rate hikes not because market participants do not think they will not happen, but because they expect this tightening phase to be short-lived. What the market currently is not in agreement with us on are the long term inflation prospects. While we think the markets true inflation expectations exceed reported breakeven inflation (and continue to rise), the market prices in still very little probability that the current price inflation isn’t largely transitory. Given our forward view on energy tightness (we will write about this in an upcoming report), this seems overly optimistic.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney or Menē, unless expressly stated. Please note that neither Goldmoney, Menē, nor any of its representatives provide financial, legal, tax, investment, or other advice. Such advice should be sought from an independent regulated person or body who is suitably qualified to do so. Any information provided in this article is provided solely as general market commentary and does not constitute advice. Neither Goldmoney nor Menē will accept liability for any loss or damage, which may arise directly or indirectly from your use of or reliance on such information. Goldmoney is a shareholder of Menē, the author a director and shareholder of Goldmoney, and has, therefore, an indirect interest in Menē.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney or Menē, unless expressly stated. Please note that neither Goldmoney, Menē, nor any of its representatives provide financial, legal, tax, investment, or other advice. Such advice should be sought from an independent regulated person or body who is suitably qualified to do so. Any information provided in this article is provided solely as general market commentary and does not constitute advice. Neither Goldmoney nor Menē will accept liability for any loss or damage, which may arise directly or indirectly from your use of or reliance on such information. Goldmoney is a shareholder of Menē, the author a director and shareholder of Goldmoney, and has, therefore, an indirect interest in Menē.