Gold market report Gold and silver is little changed

Sep 27, 2013·Alasdair MacleodGold and silver is little changed on the week, having survived attempts to push gold lower through the $1300 level and silver through $21.25 on Tuesday. Precious metals are not the only markets to be waiting for a new sense of direction following the Fed’s decision not to taper, though in early trade today gold is showing some improvement.

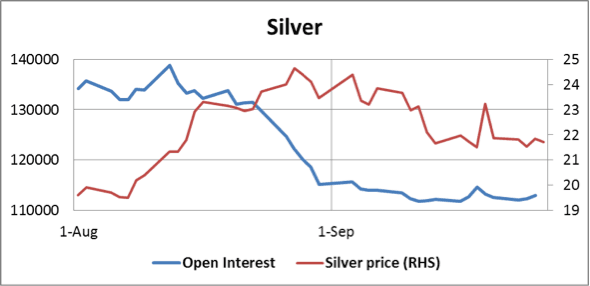

The general lack of interest is shown in the charts below, where open interest on Comex is now at very low levels.

It is noticeable how open interest has fallen from the time of the August lows, and in the case of silver it is down nearly 30%. The short positions have reduced from extremes to only abnormal, and the longs in most trader categories are on the low side. However, it is a sign of relative strength that against this lacklustre interest those August lows are holding, a performance that should worry those with short positions, given the strong demand for physical gold, summarised below.

Russia’s official gold reserves have increased to 1,015.5 tonnes and have nearly caught up with China’s 1,054 tonnes. With her massive oil and gas surpluses Russia is likely to continue to accumulate gold and overtake China soon. Kazakhstan now holds 134.5 tonnes, and Turkey continues to add to her position with 487.4 tonnes.

In the private sector net liquidation of the GLD ETF slowed to about 10 tonnes in September so far, after 17 tonnes in August, and is not a significant factor. And we learn this week, according to the Bank of Thailand that Thai gold imports in the first seven months were worth $10.9bn, which translates into approximately 240 tonnes, compared with a similar amount for the whole of 2012.Thailand is proposing a new official gold market in Bangkok, based on that country’s escalating demand. Elsewhere in the region China through the Shanghai Gold Exchange (SGE) has delivered enough gold to absorb all non-Asian mine output on its own, to which has to be added Hong Kong’s trade statistics for non-monetary gold adjusted for regional double-counting. The available figures for just these three centres are shown in the table below.

It is against this extraordinary background, where only some of total Asian demand dwarfs global mine supply by an extraordinary margin, that Western capital markets nervously worry about the short-term outlook for gold prices. Where this gold is coming from is a longer story, but there is little doubt that at current prices physical demand easily exceeds available supply.

Next Week

Next week is a quiet one for announcements, the highlight perhaps being on Wednesday with an expected no change in ECB interest rates, but a press conference to follow in the early afternoon may reveal some policy statements.

Monday: Eurozone: M3 money supply. UK: Current Account Deficit. US: Initial Claims. Japan: Core CPI.

Tuesday: Japan: Vehicle Sales. UK: Halifax House price Index. Eurozone: Manufacturing PMI; Unemployment. US: Manufacturing PMI; Construction Spending; ISM Manufacturing; Vehicle Sales.

Wednesday: Eurozone: PPI; ECB Interest Rate. US: ADP Employment Survey.

Thursday: China: CPI; PPI. Eurozone: Composite PPI; Services PPI; Retail Trade. US: Initial Claims; Factory Orders; ISM Non-manufacturing Index.

Friday: US: Non-farm Payrolls; Unemployment. Japan: BOJ Monetary Policy Announcement.