Gold and silver surge ahead

Jan 23, 2026·Alasdair MacleodAmid signs of an intensifying derivative crisis in silver, gold is probably beginning to discount disruption in paper markets. Western speculators are sidelined.

Looking into the guts of COT reports, we see that the increase in Comex open interest in gold does not much reflect managed money buying into momentum. It rather reflects Globex trade, predominantly Asian in origin buying futures presumably with a view to taking delivery.

Is this why Comex stopped reporting stand-for-deliveries from 15th January in both contracts? Is it a warning sign of derivative problems?

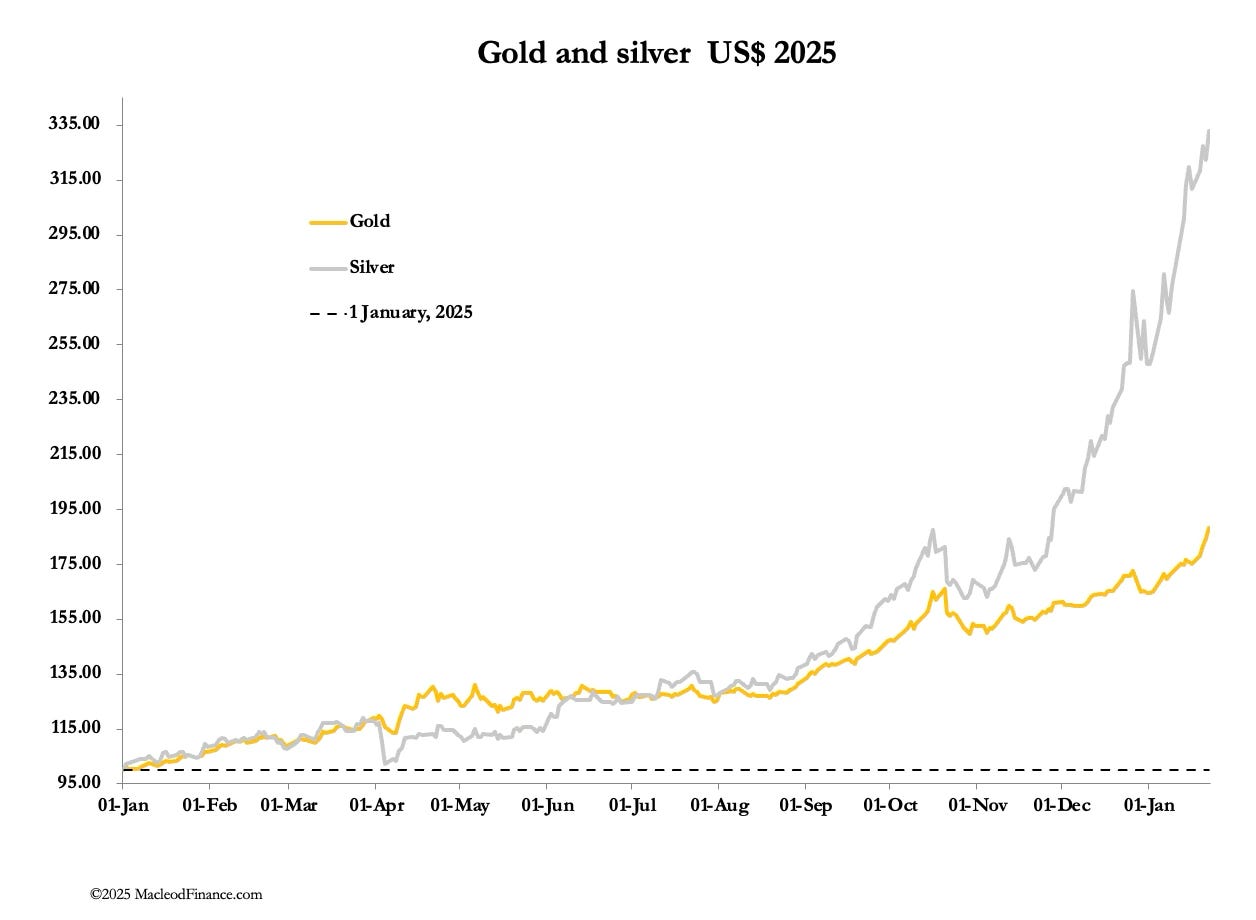

Gold and silver continued to rise this week, both establishing new record prices in all currencies. In early morning European trade, gold closed out the week at $4915, up $308, and silver at $98.20 is up $8.10. Overnight, they hit $4967 and $99.30 respectively.

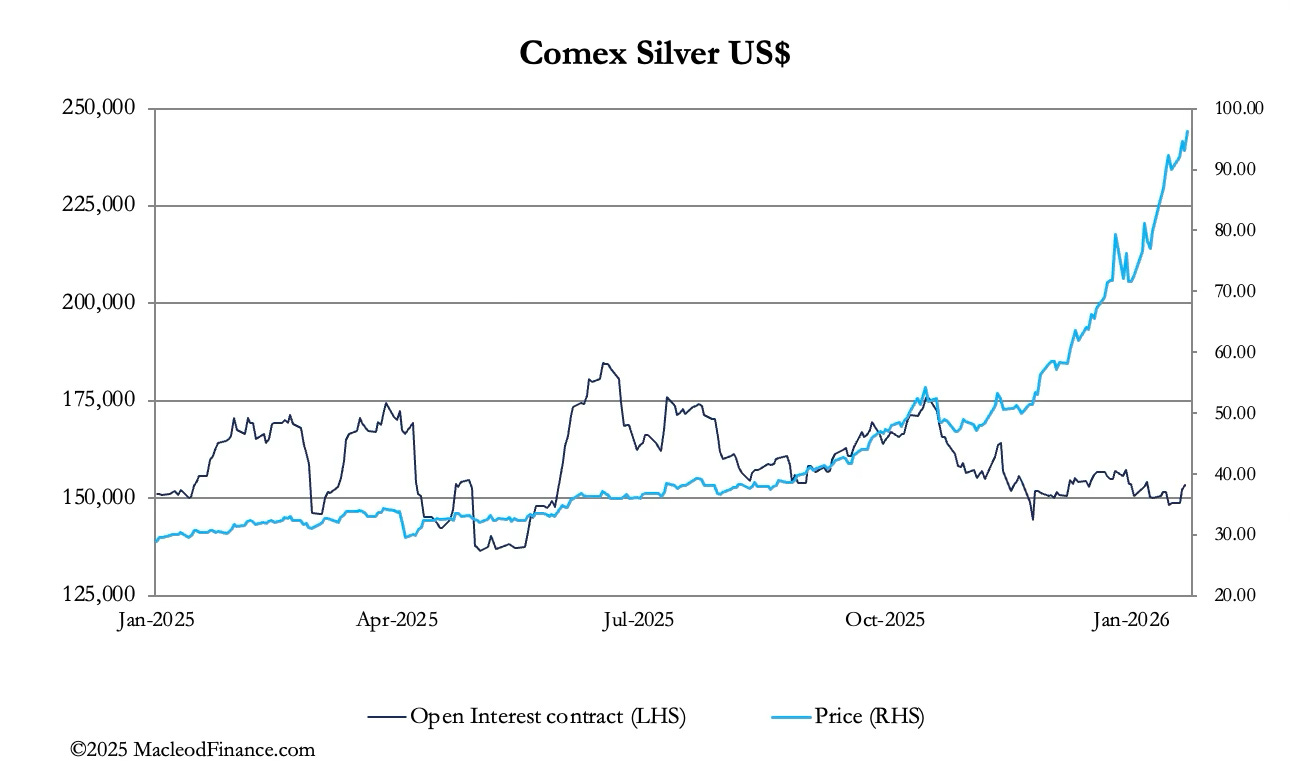

On Comex this week, volumes in both contracts were high, but declining somewhat in silver as the price rose, evidence of an intensifying squeeze on paper shorts.

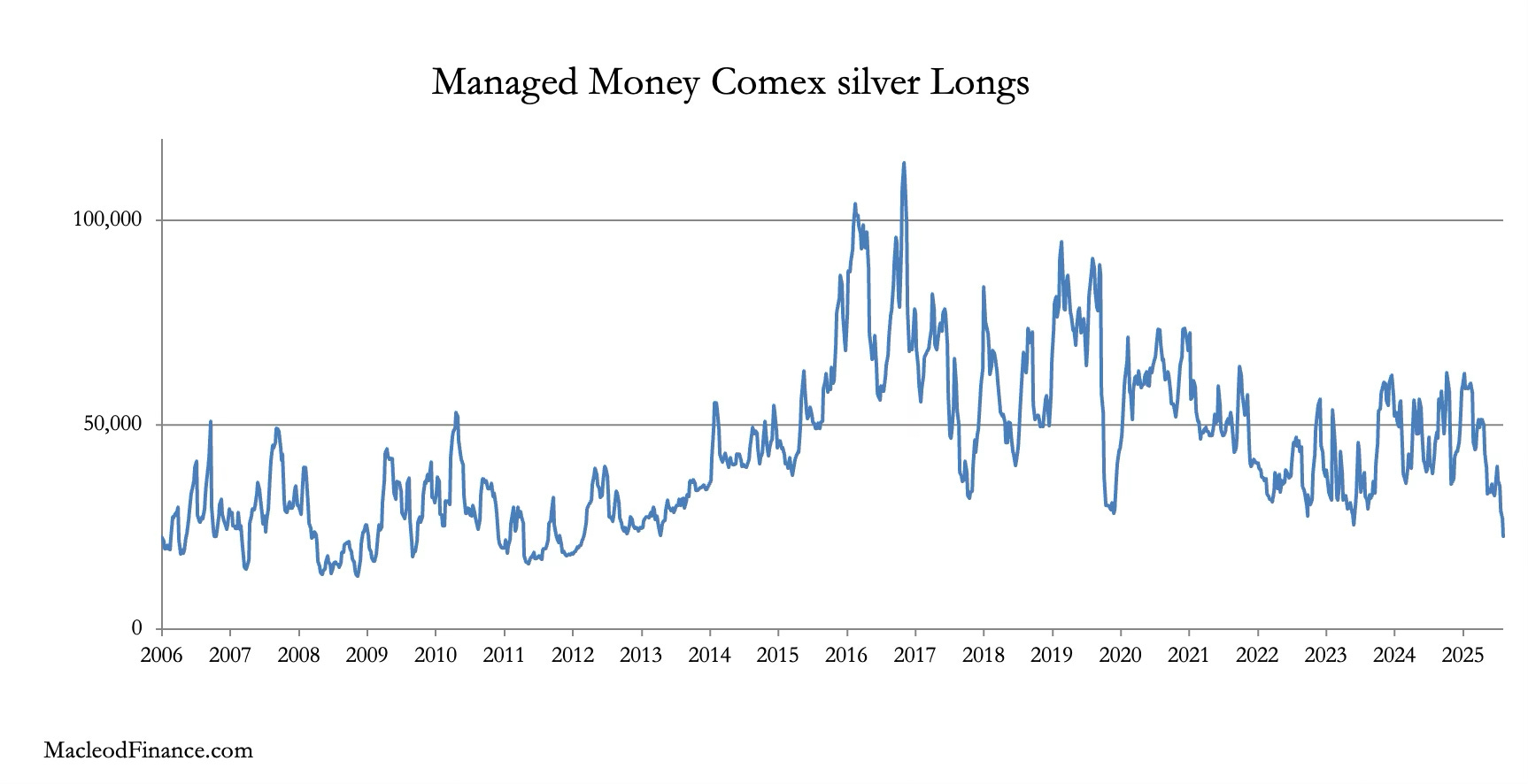

Why is it that hedge funds are not playing the silver game? It is reasonable to suggest that they should be making hay out of this short squeeze, but they appear not to. Instead, they seem scared by silver’s sheer volatility. The next chart continues to illustrate this fact:

To this evidence we can add the managed money longs from the CFTC’s Commitment of Traders numbers. They are approaching the lowest levels seen in the last 20 years:

Furthermore, the smart money leading the charge is in China where silver prices are a good 10% higher than in seemingly reluctant London and Comex.

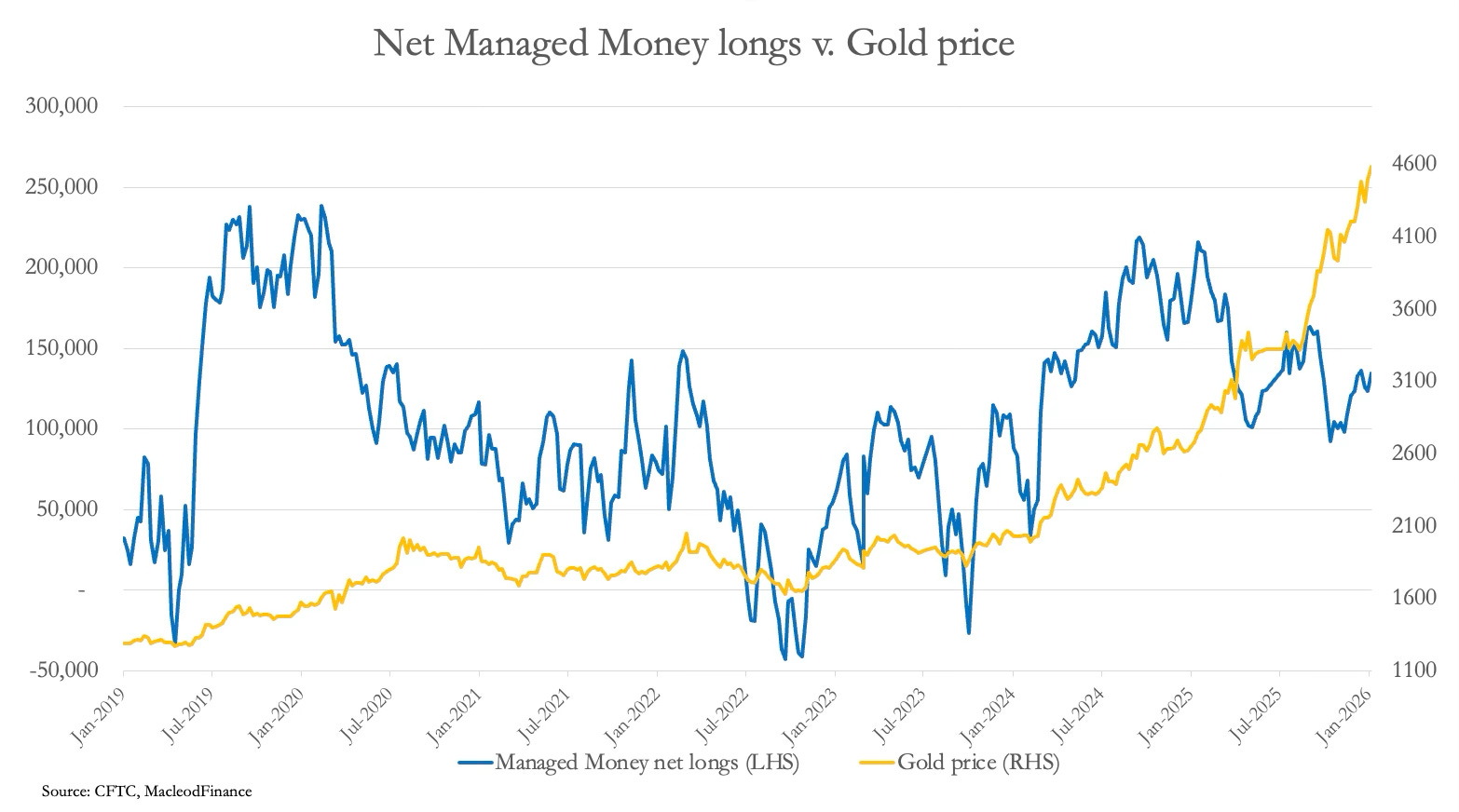

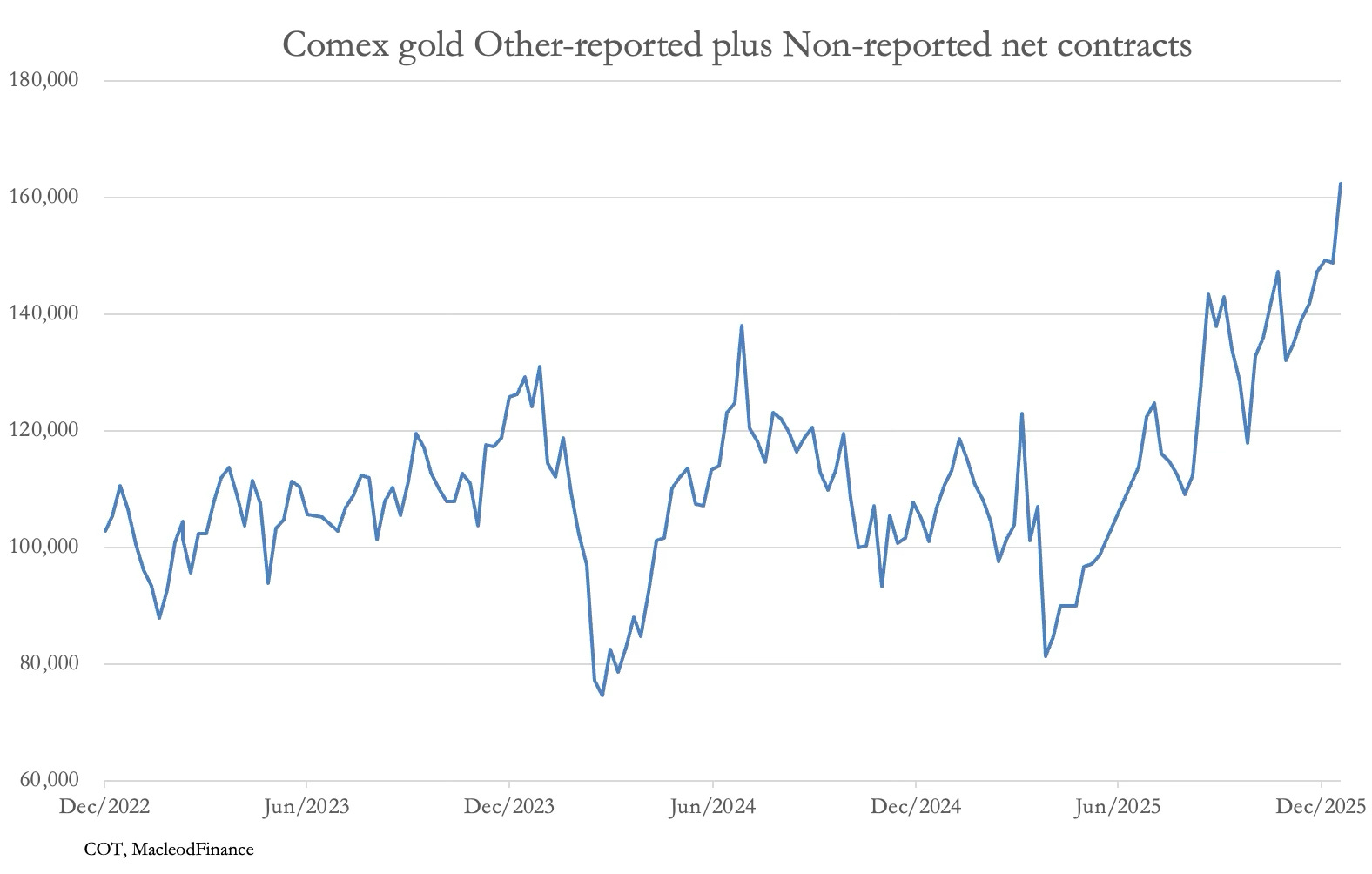

We cannot say for certain that China is setting out to destroy Western capital markets, but there is supporting evidence that they are being unfriendly towards our financial system. They have established a non-dollar payment system which is increasingly being used in what appears to be an alternative for the global south to the fiat dollar for trade settlement balances. And they are starving the West of rare earths, presumably extended to silver policy. It means the dollar is becoming sidelined and sold down, a process which may be accelerating. Further evidence that the west is frozen out of the action is seen in gold. The next chart shows US managed money longs on Comex:

While there has been an uptick in the net position since end-October, as an overbought/oversold indicator it is level with the long-term average. The position of the other and non-reported categories confirms that most of the long interest is there:

It is these categories that contain non-US and most of non-European interest including central banks, national wealth funds, and Asian family-offices.

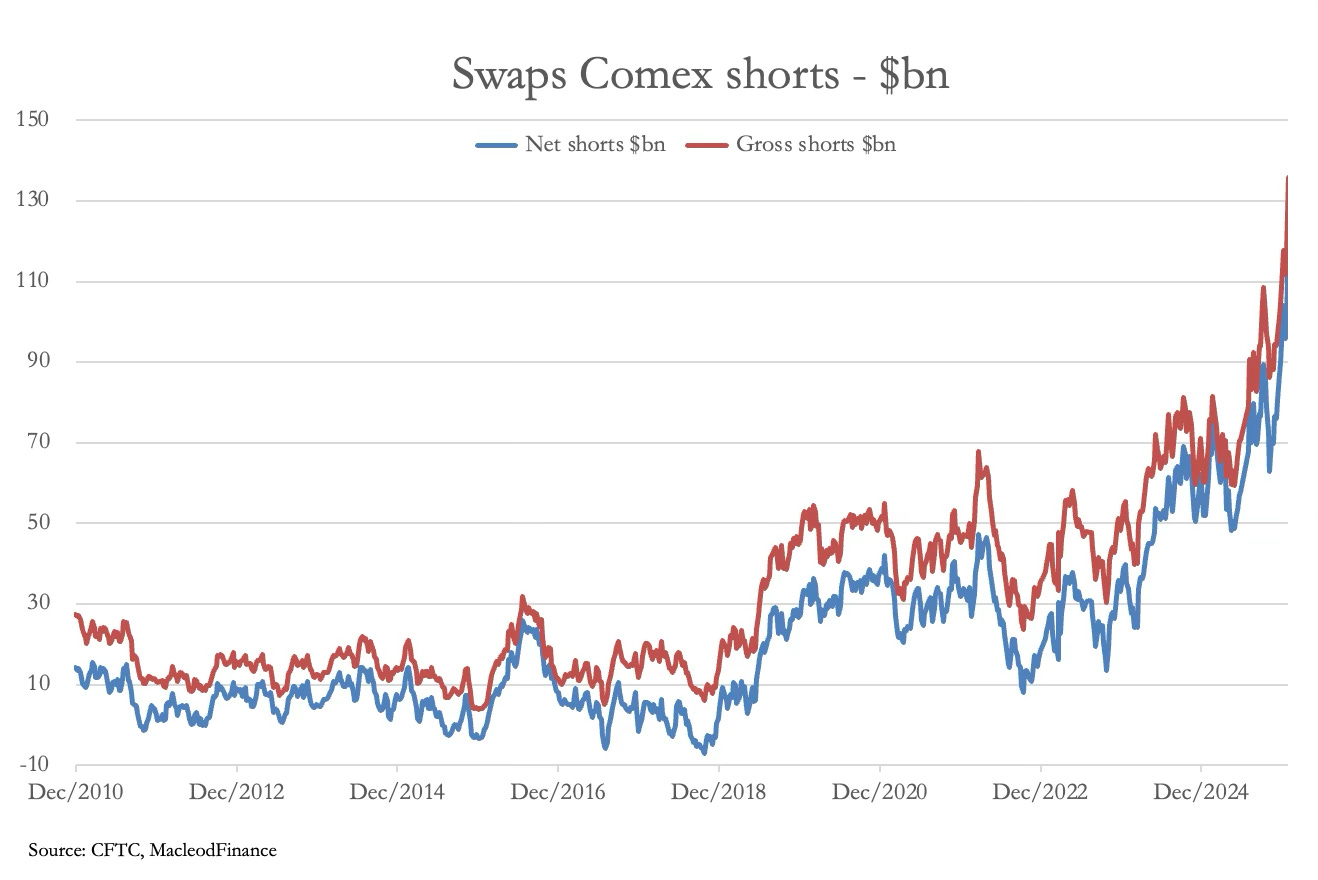

So far, we can assume that bullion banks and market makers in the swaps category are covered long in London forwards, though their short position on Comex is now positively scary:

Being long in London and short on Comex depends on the integrity of both markets being maintained, which in turn relies on counterparty risk not escalating. We can only guess how Comex feels about its potential liability in the event of counterparty failure and whether it will be prepared to destroy its own credibility by declaring force majeur, which it can do within its own rules. The LBMA and the Bank of England must be monitoring London’s forward markets with some concern as well.

In the end-game of the fiat currency era, these market disruptions are an interim event. However, the spread of counterparty risk throughout the entire derivative system would hasten the demise of credit, including the value of fiat currencies. We have yet to see investment managers take on board this risk and respond by the only way they can, which is to attempt to acquire physical gold and silver.

This panic of some $300 trillion in global investment portfolios desperately increasing their less than 1/2% exposure is yet to come. And when it does, it should be epic.