Gold and silver prospects for 2022

Dec 23, 2021·Alasdair MacleodIt has been a disappointing year for profit-seeking precious metal investors, but for those few of us looking to accumulate gold and silver as the ultimate insurance against runaway inflation it has been an unexpected bonus.

After reviewing the current year to gain a perspective for 2022, this article summarises the outlook for the dollar, the euro, and their financial systems. The key issue is the interest rate outlook, and how that will impact financial markets, which are wholly unprepared for the consequences of the massive expansions of currency and credit over the last two years.

We look briefly at geopolitical factors and conclude that Presidents Putin and Xi have assessed President Biden and his administration to be fundamentally weak. Putin is now driving a wedge between the US and the UK on one side and the pusillanimous, disorganised EU nations on the other, using energy supplies and the massing of troops on the Ukrainian border as levers to apply pressure. Either the situation escalates to an invasion of Ukraine (unlikely) or America backs off under pressure from the EU. Meanwhile, China will continue to build its presence in the South China Sea and its global influence through its silk roads. Less appreciated is that China and Russia continue to accumulate gold and are ditching the dollar.

And finally, we look at silver, which is set to become the star performer against fiat currencies, driven by a combination of poor liquidity, ESG-driven industrial demand and investor realisation that its price has much catching up to do compared with lithium, uranium, and copper. The potential for a fiat currency collapse is thrown in for nothing.

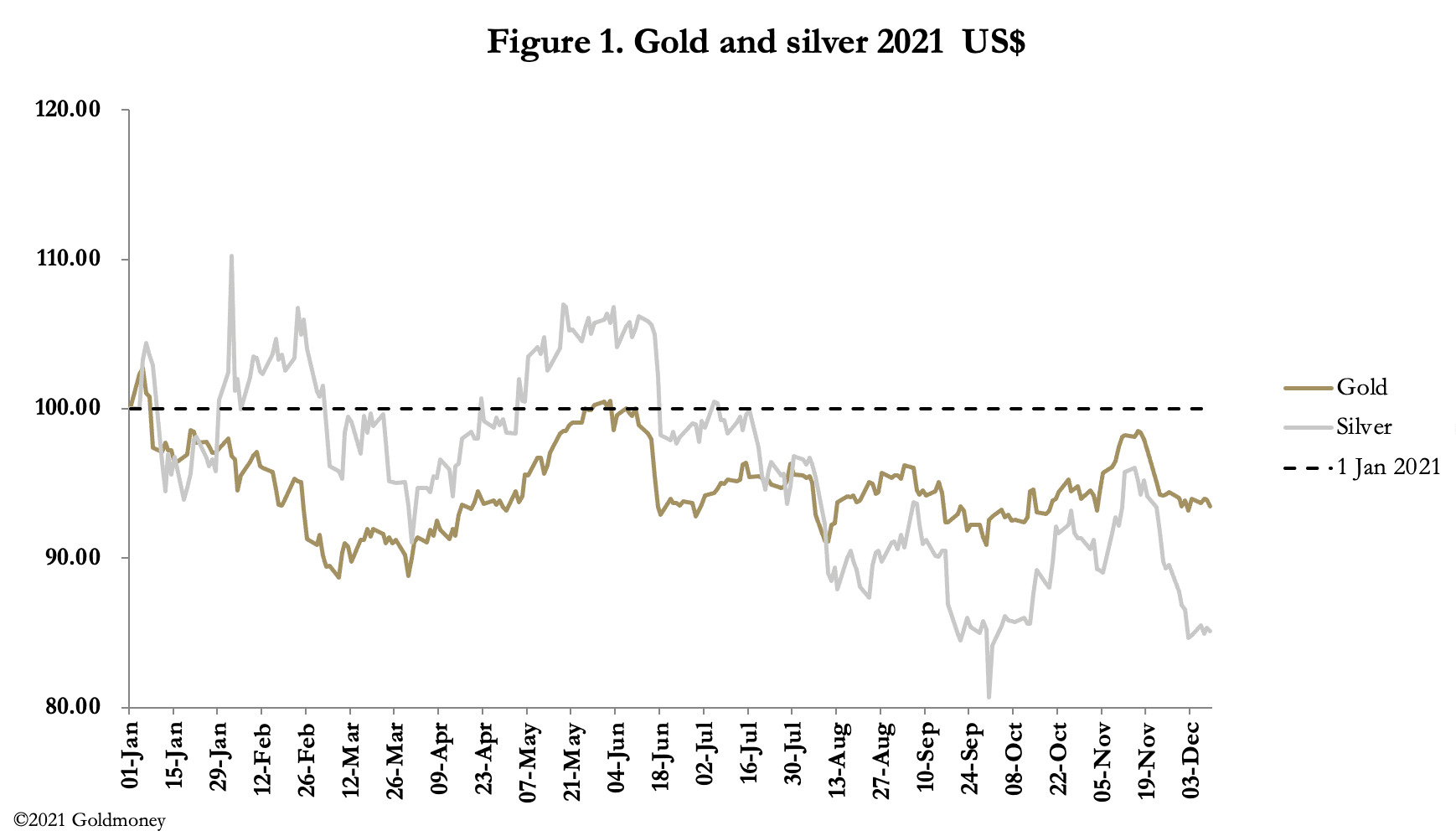

Having lost as much as 11.3%, gold is down 6.5%. And silver, which at one stage was down 19.3% is down 15%. Admittedly these returns followed strong gains in 2020, so 2021 could be described as a year of consolidation.

But this outcome was counterintuitive, given the monetary background. Total assets of the five major central banks (Fed, ECB, BoJ, PBoC and BoE) rose from $20.4bn to $32.5bn between February 2020 and today, which works out at an average annualised increase of 32% for each of two years on the trot. Since 2006, total assets for these central banks have increased by 500%.

Since February 2020, US M2 money supply has increased at an annualised rate of 20.2%, for nearly two successive years, and now stands at over 90% of GDP, having started the millennium at 44.4% of GDP. But as will be demonstrated later in this article, adjusted for the temporary withdrawal of liquidity through reverse repos, the true quantity of M2 money is practically 100% of GDP.

Without doubt, there is a surfeit of dollars and similar excesses of all other major currencies in circulation, a global condition which has worsened considerably since March 2020. The rate of inflation of currency and credit has never been so high on a global basis, ever. Yet gold and silver hardly reflected it.

Behind it all is the fatal but common mistake to fail to connect rising prices with currency debasement. No statements from any of the major central banks on monetary policy have mentioned the quantity of currency, only the consequences for prices and interest rates. And there is a broad consensus between central banks that rising interest rates are to be deployed only in the last resort. The right to issue as much currency as central banks desire will remain sacrosanct. That prices are rising above the common target level of 2% and will remain there must be denied.

For now, ovine investors accept this narrative unquestioningly. Officialdom is also wrongly committed to inflationary policies to increase the GDP total. Policymakers, establishment economists, and investment strategists alike fail to understand that increases in GDP are not indicative of an improvement in economic conditions — progress is intangible and unquantifiable. GDP is only a reflection of the quantity of currency and credit in the economy. The remarkable recovery from the collapse in GDP in 2020 was not an economic recovery; it was simply a reflection of ramped-up unproductive government deficit spending. And the savings ratio which shot up was no more than a temporary reservoir of stimmy-inflated bank deposits. What should worry us all is that no one in charge of economic and monetary policy, let alone the wider public, appears to understand this basic error.

It is not in their interest to do so, because take away GDP and the entire argument for state intervention collapses. For this reason, the commitment to monetary inflation must be total. We can conclude, to paraphrase Noël Coward, “Hurray-hurray-hurray, Inflation’s here to stay!”[i]

The antipathy to recognising this fundamental error is behind the confused market response to inflationary conditions — with the notable exception perhaps of cryptocurrency enthusiasts. But even for them, the inflation argument only goes so far as to recognise the difference between an open-ended facility to issue national currencies and the hard restrictions on the issue of bitcoin. No hodler has yet to come up with a convincing explanation of how bitcoin will replace failed fiat currencies as a widely accepted medium of exchange. It has been this confusion over what money truly is and the difference between money and fiat currency which in 2021 has suppressed a wider interest in physical gold and silver.

To this confusion has been added structural changes in the banking system with the introduction of Basel 3’s net stable funding ratio. Most banks now must comply with the NSFR, with the notable exception of UK banks so far, until that is, the New Year. The intention is to ensure that bank liabilities are stable with respect to the funding of assets, thereby lessening the risk of financing instabilities and their systemic consequences. Under the new rules a bank that maintains principal positions in derivatives of all types must accept a financing penalty. And even if a bank finds that dealing in derivatives is so profitable that it is worth paying the penalty, its management is unlikely to freely embrace business lines that could adversely affect its reputation with the regulators.

2021 was therefore a year when banks attempted to moderate their positions in derivatives as the NSFR was introduced, actions that are likely to continue into 2022. Bullion banks will want to cut their liabilities to unallocated precious metals’ deposit accounts — that can be done simply by varying account terms. But taking the short side of regulated futures contracts cannot be negated by the stroke of a pen. They must be closed or the NSFR penalty tolerated. My guess is that bankers will initially restrict their derivative positions to regulated futures markets because they can more easily be defended from a reputational standpoint.

Compared with London’s OTC forward and swaps, Comex’s regulated futures are by far the smaller market, approximately one eighth the size. And as banks reduce their derivative exposure, the withering of forward markets can be expected to unlock hidden physical demand. Physical commodities, including precious metals, are unregulated, but an unallocated bank account tied to a commodity price is. This might not trouble investors managing their own money, but any regulated investment manager holding unallocated gold deposits on behalf of clients will lose that facility. And if a manager wishes to retain price exposure, he will be forced to buy ETFs or persuade his compliance officer to sign off on an allocated physical investment instead.

As London’s forwards market shrinks, the structure of Comex, whereby the Swaps category and banks operating within the Producer/Merchant/Processor/User category are classified as non-speculators, when they are in fact speculators and not genuine hedgers, should come under increased scrutiny. The trigger for such a debate is likely to be an overall loss of market liquidity as the London market diminishes, leading to greater price volatility and severe price backwardations as derivative supply dries up. And while we can point to the effects of Basel 3 on precious metals, we must not ignore the consequences for other commodities and energy contracts. Following the recent global fiat currency debasements, many commodity contracts have been in persistent backwardation. The reduction of derivative liquidity is sure to aggravate physical shortages for commodities generally and inflate their prices further.

For policy planners in the central banks, these changes could hardly come at a worse time. Renewed rises in raw material and commodity prices will lead to a rational expectation of a far greater fall in state currencies’ purchasing power at the consumer level than has occurred so far. It appears therefore, that the fall in the purchasing power of the dollar and of other currencies has barely started.

For policy planners in the central banks, these changes could hardly come at a worse time. Renewed rises in raw material and commodity prices will lead to a rational expectation of a far greater fall in state currencies’ purchasing power at the consumer level than has occurred so far. It appears therefore, that the fall in the purchasing power of the dollar and of other currencies has barely started.

But even statistics cannot be taken at face value. Deposit liquidity is managed by central bank intervention using repurchase and reverse repurchase agreements (repos and RRPs respectively). By entering into a repo transaction, in return for collateral held as security a central bank injects liquidity into the financial system, increasing large deposits held at the banks. The liquidity crisis in September 2019 was dealt with in this way when the Fed’s overnight repos rocketed up to a record $80bn.

By entering into RRPs, a central bank removes liquidity from the financial system. Both repos and RRPs are temporary in nature, mostly being overnight in duration. Being temporary, we must adjust M2 money supply by subtracting repos from it and adding in reverse repos for a truer picture. The outcome is illustrated in Figure 3.

Repo balances had diminished to zero by July 2020, and RRPs only became significant last April. Together, these explain the deviation of the blue line from M2 (the red line) since December 2019. Taking the most recent RRP number of $1,748bn, the adjusted M2 level becomes approximately $23,100bn, an increase of 48.2%, or 24.1% annualised for two successive years.[ii]

The excess liquidity currently hidden in RRPs is the consequence of unfunded government deficit spending. It is government spending which ends up as surplus deposits in the banking system without them being offset by public subscriptions for government debt. Quantitative easing contributes to the problem, giving deposit money to pension funds and insurance companies in return for securities that end up on the Fed’s balance sheet.

The effect of this inflation on prices is still working through the US economy. It is important to appreciate that the inflation of bank deposits is the primary cause for the increase in raw material, production and consumer costs and prices, and not supply chain disruptions. Central bankers are being disingenuous when they insist that rising prices are a temporary phenomenon. The expansion of deposits and excess liquidity, particularly since last April, tells us that even without changes in the public’s level of retention of currency relative to goods, there is a considerable loss of the dollar’s purchasing power yet to come. And neo-Keynesian arguments that faltering demand will restore the balance between supply and demand for consumer goods are incorrect.

We therefore enter 2022 with the prospect of further increases in the rates of production cost and consumer price increases. That interest rates will begin to rise significantly is guaraanteed. Already, with the US CPI recording an annual increase of 6.8%, establishment investors are accepting a negative real yield on the 10-year US Treasury of 5.4%. And for those who follow John Williams’ Shadowstats.com, which calculates consumer price rises “Consistent with the methodologies of pre-1980 headline CPI reporting” at 14.9%, the real yield on the 10-year bond is minus 13.5%![iii]

How far interest rates will rise in the coming months is not yet clear, but it is likely that they will rise substantially more and sooner than is currently discounted. Furthermore, the tapering of QE is planned to be accelerated, reducing in a roundabout way the support to government funding from the Fed. Without that support, markets will almost certainly demand lower negative real yields on Treasuries at the least, forcing nominal yields considerably higher. The shock of a move towards market reality could be immense and unexpected.

Higher nominal yields on bonds mean significant investment losses for bond portfolios, and the basis for equity valuations will also be badly undermined. A substantial bear market in all financial assets is becoming more certain by the day. Furthermore, higher borrowing costs will threaten the zombie corporations unable to earn sufficient returns on their borrowings. It is a situation the Fed has tried to avoid, using QE to sustain low bond yields and high market values.

Having decided to reduce the monthly QE stimulus, a bear market in financial assets has been made more certain. To counter the effect, the Fed will probably end up increasing QE again to support market prices, as they did in March 2020. But QE and a return to it is blatant currency printing which can only serve to undermine the dollar’s purchasing power even further and eventually require yet higher bond yield compensation: it is no more than a temporary sticking plaster on a suppurating wound.

A developing slump in economic activity from higher nominal interest rates will also add to the Federal Government’s deficit by reducing tax income and increasing welfare spending. In any contemporary administration, particularly the Biden one, there is no mandate to address this problem and we must assume at this distance that it can only be resolved by further debt being issued at increasingly higher yields.

The situation resembles that faced by an earlier proto-Keynesian, John Law in 1720. To sustain his Mississippi bubble, he supported the share price by freely issuing his livre currency to buy stock in the market, which he could do as controller of the currency. It was not long before the livre’s purchasing power was undermined entirely.

As the current situation for the dollar unfolds, its purchasing power is set to decline similarly to the French livre of three centuries ago. But there is also an ugly systemic problem in the commercial banking network, for which to appreciate we must turn our attention to Europe.

Therefore, in real terms, not only are negative rates already increasing, but they will go even further into record negative territory due to rising producer and consumer prices. Unless it abandons the euro to its fate on the foreign exchanges altogether, the ECB will be forced to permit its deposit rate to rise from its current —0.5% to offset the euro’s depreciation. And given the sheer scale of recent monetary expansion, euro interest rates will have to rise considerably to have any stabilising effect.

The euro shares this problem with the dollar. But even if interest rates increased only into modestly positive territory, the ECB would have to quicken the pace of its monetary creation just to keep highly indebted Eurozone member governments afloat. The foreign exchanges are bound to recognise the developing situation, punishing the euro if the ECB fails to raise rates and punishing it if it does. The euro’s fall won’t be limited to exchange rates against other currencies, which to varying degrees face similar dilemmas, but it will be particularly acute measured against prices for commodities and essential products. Arguably, the euro’s derating on the foreign exchanges has already commenced.

But there is an additional factor not generally appreciated, and that is the sheer size of the euro’s repo market and the danger to it that rising interest rates presents. Demand for collateral against which to obtain liquidity has led to significant monetary expansion, with the repo market acting not as a marginal liquidity management tool as is the case in other banking systems, but as an accumulating source of credit. This is illustrated in Figure 4, which is of an ICMA survey of 58 leading institutions in the euro system.[v]

The total for this form of short-term financing grew to €8.31 trillion in outstanding contracts by December 2019. The collateral includes everything from government bonds and bills to pre-packaged commercial bank debt. According to the ICMA survey, double counting, whereby repos are offset by reverse repos, is minimal. This is important when one considers that a reverse repo is the other side of a repo, so that with repos being additional to the reverse repos recorded, the sum of the two is a valid measure of the size of the repo market. The value of repos transacted with central banks as part of official monetary policy operations were not included in the survey and continue to be “very substantial”. But repos with central banks in the ordinary course of financing are included.[vi]

Today, even excluding central bank repos connected with monetary policy operations, this figure almost certainly exceeds €10 trillion by a significant margin, given the accelerated monetary expansion since the ICMA survey, and when one allows for participants beyond the 58 dealers recorded. An important element of this market is interest rates, which with the ECB’s deposit rate sitting at minus 0.5% means Eurozone cash can be freely obtained by the banks at no cost.

The zero cost of repo cash raises the question of the consequences if the ECB’s deposit rate is forced back into positive territory. The repo market will likely contract in size, which is tantamount to a decrease in outstanding bank credit. Banks would then be forced to liquidate balance sheet assets, which would drive all negative bond yields into positive territory, and higher, accelerating the contraction of bank credit even further as collateral values collapse. Moreover, the contraction of bank credit implied by the withdrawal of repo finance will almost certainly have the knock-on effect of rapidly triggering a liquidity crisis in a banking cohort with exceptionally high balance sheet gearing.

There is a further issue to consider over collateral quality. While the US Fed only accepts very high-quality securities as repo collateral, with the Eurozone’s national banks and the ECB almost anything is accepted — it had to be when Greece and the other PIGS were bailed out. And the hidden bailouts of Italian banks by bundling dodgy loans into repo collateral was the way they were removed from national bank balance sheets and hidden in the TARGET2 system

The result is that the first repos not to be renewed by commercial counterparties are those whose collateral is bad or doubtful. We have no knowledge how much is involved. But given the incentive for national regulators in the PIGS to have deemed non-performing loans to be creditworthy so that they could act as repo collateral, the amounts will be considerable. Having accepted this bad collateral, national central banks will be unable to reject them for fear of triggering a banking crisis in their own jurisdictions. Furthermore, they are likely to be forced to accept additional repo collateral if it is rejected by commercial counterparties and bank failures are to be prevented.

The numbers involved are larger than the ECB and national central banks’ combined balance sheets.

The crisis from rising interest rates in the Eurozone will be different from that facing US dollar markets. With the Eurozone’s global systemically important banks (the G-SIBs) geared up to thirty times measured by assets to balance sheet equity, rising bond yields of little more than a few per cent will likely collapse the entire euro system, spreading systemic risk to Japan, where its G-SIBs are similarly geared, the UK and Switzerland and then the US and China which have the least operationally geared banking systems.

It will require the major central banks to mount the largest banking system rescue ever seen, dwarfing the Lehman crisis. The required expansion of currency and credit by the central bank network is unimaginable and comes in addition to the massive monetary expansion of the last two years. The collapse in purchasing power of the entire fiat currency system is therefore in prospect, along with the values of everything that depends upon it. The only sure-fire escape for the ordinary person is to physically possess the money of history that cannot be corrupted, and to which when the state theory of money is disproved yet again, becomes the only acceptable medium of exchange. That is physical gold and silver.

Elsewhere, I have reasoned that China has secretly accumulated enormous quantities of gold, likely to be at least 20,000 tonnes, possibly even more, and its citizens have also accumulated a further 17,000 tonnes.

Briefly, the evidence is as follows. The Peoples’ Bank was mandated to acquire and manage the state’s gold and silver resources by regulation in 1983, an extension of its foreign exchange monopoly. Consequently, the PBOC had a clear run-in accumulating gold during the 1981-2002 bear market while China’s citizens were banned from owning both metals. In 2002, the Shanghai Gold Exchange was established and the ban on gold and silver ownership by the public was lifted. The Communist Party even advertised the benefits of owning precious gold, developing significant levels of public demand — hence public ownership estimated at 17,000 tonnes.

At the same time the State invested heavily in mining and refining. Consequently, from virtually nowhere China became the largest gold mining nation by far and has maintained that position ever since. No gold was permitted to be exported, and the only Chinese refined bars ending up at the Swiss refineries have been very few and believed to have been smuggled.

While we cannot be certain of the numbers, the evidence that the Communist Party has prioritised the accumulation of gold, and to a lesser extent perhaps silver, and now exercises a high degree of monopolistic control over Asian gold markets is irrefutable.

Similarly, President Putin has also prioritised the accumulation of gold, though his reasoning was partly driven by American and IMF sanctions in the wake of Russia’s invasion of Ukraine in 2014. Russia’s strategic vulnerability is in the payment for her energy sales, which is overwhelmingly in dollars — the currency of her enemy. Furthermore, under the correspondent banking system, the US has source intelligence of every dollar that is held by Russia and of all her dollar transactions. Putin’s response has been to unload dollars acquired through energy and commodity exports in favour of gold and other currencies.

Russia’s political strategy is to allay herself closely with China through the Shanghai Cooperation Organisation and other Asian political groupings, to jointly control the Eurasian landmass, and therefore the bulk of the world’s population. As the swing energy provider to Western Europe, Russia is driving a wedge between America and the UK on one side, and their NATO partners on the other. Currently, she is sabre-rattling on Ukraine’s eastern flank, but the intention is more likely to exploit the interests of EU member nations and remove the EU from the US’s sphere of influence.

Similarly, China is rattling her sabres over Taiwan and the South China Sea. This is also designed to bring pressure to bear on America. The common factor is Russian and Chinese assessments of the Biden administration, which they appear to believe to be fundamentally weak.

With respect to gold and silver, we can summarise the current geopolitical position as follows. Between them, Russia, China, and their Asian allies have gone a long way towards cornering the world’s physical gold markets. They are now testing the Biden administration, and Putin has a clear intention to isolate America from Western Europe. Meanwhile, the Fed is pursuing monetary policies which, unless reversed (for which there is no conceivable mandate) will inevitably hand economic power to China and Russia because of their gold-friendly policies. And if America and her allies cut up rough, through their joint domination of physical gold and its markets, China and Russia have the means to destroy the unbacked, fiat dollar.

According to the Silver Institute, physical supply in 2021 increased over a depressed 2020 by 8% to 1,056 million ounces but remains below the output for 2014-2016. Meanwhile demand is up 15% this year at 1,033m oz leaving a marginal surplus of just 23m oz. The question obviously arises concerning demand patterns over the next few years at a time of accelerating investment in non-fossil fuel energy and electricity. For silver, increasing demand for electric vehicles and upgrading of mobile networks to 5G can be added to photovoltaic demand. Forecasting the balance of supply and demand is always difficult for silver because of substantial and unforeseen changes in usage (remember photography?), but it seems reasonable to assume that silver will be one of an elite group of beneficiaries from global environmental policies.

The mining industry faces additional cost burdens in many countries as they adjust their operations to comply with environmental, social and governance (ESG) regulations and guidance. International miners will be hampered in fund raising if they don’t comply, even for their mines in countries which have yet to formulate their ESG policies to Western standards. Higher costs such as those imposed by ESG compliance can be expected to force mines to extract higher grades to maintain cash flow, so only higher prices rising faster than costs will impart any value to lower grade ores. The effect of ESG is therefore likely to downgrade longer term mine supply forecasts.

Lithium Uranium and copper, three of the other beneficiaries of ESG, saw their prices rise in 2021. Lithium Carbonate prices are up 520% since January, Uranium rose 54%, while copper rose 25% on top of a strong post-March 2020 rise. In silver’s case, a swing factor is investment in ETFs which for the last decade has varied between 200-300m oz. By way of contrast with lithium uranium and copper, the silver price declined this year by 15%.

But as a measure of total interest, physical silver demand is the tip of a far larger derivative iceberg. According to the Bank for International Settlements, outstanding forwards and swaps total roughly 3750m oz equivalent between bullion banks, and there are further liabilities between banks and their depositors with unallocated accounts. In addition, there are 715m paper ounces in the regulated Comex silver contract, which with other regulated exchanges suggests that there are at least 4,500m oz of added long positions in derivatives, which is 20 times estimated net physical investment demand for this year. And that ignores regulated and unregulated options.[vii]

While it appears that industrial demand for silver is set to increase significantly, the pricing of silver in fiat currencies at one eightieth that of gold is also anomalous at a time of accelerating price inflation, more correctly understood as currency debasement. Mismanagement of monetary policies now virtually guarantees the death of fiat currencies, and the only salvation will be to replace or change them into credible gold substitutes, because most central banks have at least some gold in their reserves.

That being so, physical silver will reacquire a monetary role as supporting coinage. Its abundance in the earth relative to gold is said to be less than ten times, and its historical relationship under bimetallic standards was approximately fifteen to one. The demise of fiat currencies is likely to guide the gold-silver ratio towards these ratios, so the current ratio of eighty times is a blatant anomaly.

In the absence of an immediate crisis for the fiat currency regime, changes to the way banks treat derivatives for balance sheet purposes are likely to lead to a contraction of open positions. The introduction of the net stable funding ratio under Basel 3 regulations is designed to curtail derivative risk generally. The withdrawal over time of banks from trading activities because of the NSFR will reduce liquidity in both OTC and regulated derivatives, leading to greater price volatility. And the contraction of paper silver outstanding is likely to translate diminishing paper supply into increased physical demand.

Anecdotal evidence is that order books for silver from the refiners currently run into the middle of 2022, with large industrial consumers scrambling to secure supplies. Any surge in monetary demand is therefore set to have a disproportionate effect on silver prices to the upside.

The establishment has provided a window of opportunity for ordinary folk to insure against the financial and economic events now so obviously ahead of them. Those who have a grasp of basic economics and deploy common sense understand that interest rates will now rise, and soon. And with extraordinarily high negative bond yields, financial markets are more mispriced for this eventuality than in any time in recorded history.

There can be little doubt in dealing with the inevitable market shock ahead that central banks will continue to issue increasing quantities of their currencies in a vain attempt to stabilise their economies and to ensure government deficits are covered. And with the increasingly likely collapse of the Eurosystem and its commercial banks, we can expect a “whatever it takes” inflationary response from the ECB.

As their world collapses around them, central bankers will act like bulls in a china shop, destroying their credibility and currencies even more as their panic increases. Against this background, buyers of physical gold and silver will do so not because they expect to profit from it, but to preserve something from the chaos in prospect, which will be triggered by rising, and then soaring interest rates as currency time preferences escalate and their purchasing power collapses.

[i] From “There are bad times just around the corner”. The couplet was that misery’s here to stay but it is an apt description of the effects of inflation.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.

After reviewing the current year to gain a perspective for 2022, this article summarises the outlook for the dollar, the euro, and their financial systems. The key issue is the interest rate outlook, and how that will impact financial markets, which are wholly unprepared for the consequences of the massive expansions of currency and credit over the last two years.

We look briefly at geopolitical factors and conclude that Presidents Putin and Xi have assessed President Biden and his administration to be fundamentally weak. Putin is now driving a wedge between the US and the UK on one side and the pusillanimous, disorganised EU nations on the other, using energy supplies and the massing of troops on the Ukrainian border as levers to apply pressure. Either the situation escalates to an invasion of Ukraine (unlikely) or America backs off under pressure from the EU. Meanwhile, China will continue to build its presence in the South China Sea and its global influence through its silk roads. Less appreciated is that China and Russia continue to accumulate gold and are ditching the dollar.

And finally, we look at silver, which is set to become the star performer against fiat currencies, driven by a combination of poor liquidity, ESG-driven industrial demand and investor realisation that its price has much catching up to do compared with lithium, uranium, and copper. The potential for a fiat currency collapse is thrown in for nothing.

2021 — That was the year that was

This year has been disappointing for precious metals investors. Figure 1 shows how gold and silver have performed since 31 December 2020.Having lost as much as 11.3%, gold is down 6.5%. And silver, which at one stage was down 19.3% is down 15%. Admittedly these returns followed strong gains in 2020, so 2021 could be described as a year of consolidation.

But this outcome was counterintuitive, given the monetary background. Total assets of the five major central banks (Fed, ECB, BoJ, PBoC and BoE) rose from $20.4bn to $32.5bn between February 2020 and today, which works out at an average annualised increase of 32% for each of two years on the trot. Since 2006, total assets for these central banks have increased by 500%.

Since February 2020, US M2 money supply has increased at an annualised rate of 20.2%, for nearly two successive years, and now stands at over 90% of GDP, having started the millennium at 44.4% of GDP. But as will be demonstrated later in this article, adjusted for the temporary withdrawal of liquidity through reverse repos, the true quantity of M2 money is practically 100% of GDP.

Without doubt, there is a surfeit of dollars and similar excesses of all other major currencies in circulation, a global condition which has worsened considerably since March 2020. The rate of inflation of currency and credit has never been so high on a global basis, ever. Yet gold and silver hardly reflected it.

Behind it all is the fatal but common mistake to fail to connect rising prices with currency debasement. No statements from any of the major central banks on monetary policy have mentioned the quantity of currency, only the consequences for prices and interest rates. And there is a broad consensus between central banks that rising interest rates are to be deployed only in the last resort. The right to issue as much currency as central banks desire will remain sacrosanct. That prices are rising above the common target level of 2% and will remain there must be denied.

For now, ovine investors accept this narrative unquestioningly. Officialdom is also wrongly committed to inflationary policies to increase the GDP total. Policymakers, establishment economists, and investment strategists alike fail to understand that increases in GDP are not indicative of an improvement in economic conditions — progress is intangible and unquantifiable. GDP is only a reflection of the quantity of currency and credit in the economy. The remarkable recovery from the collapse in GDP in 2020 was not an economic recovery; it was simply a reflection of ramped-up unproductive government deficit spending. And the savings ratio which shot up was no more than a temporary reservoir of stimmy-inflated bank deposits. What should worry us all is that no one in charge of economic and monetary policy, let alone the wider public, appears to understand this basic error.

It is not in their interest to do so, because take away GDP and the entire argument for state intervention collapses. For this reason, the commitment to monetary inflation must be total. We can conclude, to paraphrase Noël Coward, “Hurray-hurray-hurray, Inflation’s here to stay!”[i]

The antipathy to recognising this fundamental error is behind the confused market response to inflationary conditions — with the notable exception perhaps of cryptocurrency enthusiasts. But even for them, the inflation argument only goes so far as to recognise the difference between an open-ended facility to issue national currencies and the hard restrictions on the issue of bitcoin. No hodler has yet to come up with a convincing explanation of how bitcoin will replace failed fiat currencies as a widely accepted medium of exchange. It has been this confusion over what money truly is and the difference between money and fiat currency which in 2021 has suppressed a wider interest in physical gold and silver.

To this confusion has been added structural changes in the banking system with the introduction of Basel 3’s net stable funding ratio. Most banks now must comply with the NSFR, with the notable exception of UK banks so far, until that is, the New Year. The intention is to ensure that bank liabilities are stable with respect to the funding of assets, thereby lessening the risk of financing instabilities and their systemic consequences. Under the new rules a bank that maintains principal positions in derivatives of all types must accept a financing penalty. And even if a bank finds that dealing in derivatives is so profitable that it is worth paying the penalty, its management is unlikely to freely embrace business lines that could adversely affect its reputation with the regulators.

2021 was therefore a year when banks attempted to moderate their positions in derivatives as the NSFR was introduced, actions that are likely to continue into 2022. Bullion banks will want to cut their liabilities to unallocated precious metals’ deposit accounts — that can be done simply by varying account terms. But taking the short side of regulated futures contracts cannot be negated by the stroke of a pen. They must be closed or the NSFR penalty tolerated. My guess is that bankers will initially restrict their derivative positions to regulated futures markets because they can more easily be defended from a reputational standpoint.

Compared with London’s OTC forward and swaps, Comex’s regulated futures are by far the smaller market, approximately one eighth the size. And as banks reduce their derivative exposure, the withering of forward markets can be expected to unlock hidden physical demand. Physical commodities, including precious metals, are unregulated, but an unallocated bank account tied to a commodity price is. This might not trouble investors managing their own money, but any regulated investment manager holding unallocated gold deposits on behalf of clients will lose that facility. And if a manager wishes to retain price exposure, he will be forced to buy ETFs or persuade his compliance officer to sign off on an allocated physical investment instead.

As London’s forwards market shrinks, the structure of Comex, whereby the Swaps category and banks operating within the Producer/Merchant/Processor/User category are classified as non-speculators, when they are in fact speculators and not genuine hedgers, should come under increased scrutiny. The trigger for such a debate is likely to be an overall loss of market liquidity as the London market diminishes, leading to greater price volatility and severe price backwardations as derivative supply dries up. And while we can point to the effects of Basel 3 on precious metals, we must not ignore the consequences for other commodities and energy contracts. Following the recent global fiat currency debasements, many commodity contracts have been in persistent backwardation. The reduction of derivative liquidity is sure to aggravate physical shortages for commodities generally and inflate their prices further.

For policy planners in the central banks, these changes could hardly come at a worse time. Renewed rises in raw material and commodity prices will lead to a rational expectation of a far greater fall in state currencies’ purchasing power at the consumer level than has occurred so far. It appears therefore, that the fall in the purchasing power of the dollar and of other currencies has barely started.Inflation outlook for the US dollar

First, we must define inflation: it is the increase in the quantity of money, currency, and credit, generally taken to be represented by total deposit liabilities in the banking system. It is not an increase in prices. Changes in the general price level is the consequence of a combination in changes of the quantity of deposit currency and changes in the level of the public’s retention of deposit currency relative to their possession of goods. We can record deposits statistically, but cannot quantify human behaviour.But even statistics cannot be taken at face value. Deposit liquidity is managed by central bank intervention using repurchase and reverse repurchase agreements (repos and RRPs respectively). By entering into a repo transaction, in return for collateral held as security a central bank injects liquidity into the financial system, increasing large deposits held at the banks. The liquidity crisis in September 2019 was dealt with in this way when the Fed’s overnight repos rocketed up to a record $80bn.

By entering into RRPs, a central bank removes liquidity from the financial system. Both repos and RRPs are temporary in nature, mostly being overnight in duration. Being temporary, we must adjust M2 money supply by subtracting repos from it and adding in reverse repos for a truer picture. The outcome is illustrated in Figure 3.

Repo balances had diminished to zero by July 2020, and RRPs only became significant last April. Together, these explain the deviation of the blue line from M2 (the red line) since December 2019. Taking the most recent RRP number of $1,748bn, the adjusted M2 level becomes approximately $23,100bn, an increase of 48.2%, or 24.1% annualised for two successive years.[ii]

The excess liquidity currently hidden in RRPs is the consequence of unfunded government deficit spending. It is government spending which ends up as surplus deposits in the banking system without them being offset by public subscriptions for government debt. Quantitative easing contributes to the problem, giving deposit money to pension funds and insurance companies in return for securities that end up on the Fed’s balance sheet.

The effect of this inflation on prices is still working through the US economy. It is important to appreciate that the inflation of bank deposits is the primary cause for the increase in raw material, production and consumer costs and prices, and not supply chain disruptions. Central bankers are being disingenuous when they insist that rising prices are a temporary phenomenon. The expansion of deposits and excess liquidity, particularly since last April, tells us that even without changes in the public’s level of retention of currency relative to goods, there is a considerable loss of the dollar’s purchasing power yet to come. And neo-Keynesian arguments that faltering demand will restore the balance between supply and demand for consumer goods are incorrect.

We therefore enter 2022 with the prospect of further increases in the rates of production cost and consumer price increases. That interest rates will begin to rise significantly is guaraanteed. Already, with the US CPI recording an annual increase of 6.8%, establishment investors are accepting a negative real yield on the 10-year US Treasury of 5.4%. And for those who follow John Williams’ Shadowstats.com, which calculates consumer price rises “Consistent with the methodologies of pre-1980 headline CPI reporting” at 14.9%, the real yield on the 10-year bond is minus 13.5%![iii]

How far interest rates will rise in the coming months is not yet clear, but it is likely that they will rise substantially more and sooner than is currently discounted. Furthermore, the tapering of QE is planned to be accelerated, reducing in a roundabout way the support to government funding from the Fed. Without that support, markets will almost certainly demand lower negative real yields on Treasuries at the least, forcing nominal yields considerably higher. The shock of a move towards market reality could be immense and unexpected.

Higher nominal yields on bonds mean significant investment losses for bond portfolios, and the basis for equity valuations will also be badly undermined. A substantial bear market in all financial assets is becoming more certain by the day. Furthermore, higher borrowing costs will threaten the zombie corporations unable to earn sufficient returns on their borrowings. It is a situation the Fed has tried to avoid, using QE to sustain low bond yields and high market values.

Having decided to reduce the monthly QE stimulus, a bear market in financial assets has been made more certain. To counter the effect, the Fed will probably end up increasing QE again to support market prices, as they did in March 2020. But QE and a return to it is blatant currency printing which can only serve to undermine the dollar’s purchasing power even further and eventually require yet higher bond yield compensation: it is no more than a temporary sticking plaster on a suppurating wound.

A developing slump in economic activity from higher nominal interest rates will also add to the Federal Government’s deficit by reducing tax income and increasing welfare spending. In any contemporary administration, particularly the Biden one, there is no mandate to address this problem and we must assume at this distance that it can only be resolved by further debt being issued at increasingly higher yields.

The situation resembles that faced by an earlier proto-Keynesian, John Law in 1720. To sustain his Mississippi bubble, he supported the share price by freely issuing his livre currency to buy stock in the market, which he could do as controller of the currency. It was not long before the livre’s purchasing power was undermined entirely.

As the current situation for the dollar unfolds, its purchasing power is set to decline similarly to the French livre of three centuries ago. But there is also an ugly systemic problem in the commercial banking network, for which to appreciate we must turn our attention to Europe.

The looming collapse of the euro

Like the Fed, the ECB is resisting interest rate increases despite producer and consumer prices soaring. Consumer price inflation across the Eurozone was most recently recorded at 4.9%, making the real yield on Germany’s 5-year bond minus 5.5%. But Germany’s producer prices for October rose 19.2% compared with a year ago. There can be no doubt that producer prices have yet to feed fully into consumer prices, and that rising consumer prices have much further to go, reflecting the acceleration of the ECB’s currency debasement in recent years.[iv]Therefore, in real terms, not only are negative rates already increasing, but they will go even further into record negative territory due to rising producer and consumer prices. Unless it abandons the euro to its fate on the foreign exchanges altogether, the ECB will be forced to permit its deposit rate to rise from its current —0.5% to offset the euro’s depreciation. And given the sheer scale of recent monetary expansion, euro interest rates will have to rise considerably to have any stabilising effect.

The euro shares this problem with the dollar. But even if interest rates increased only into modestly positive territory, the ECB would have to quicken the pace of its monetary creation just to keep highly indebted Eurozone member governments afloat. The foreign exchanges are bound to recognise the developing situation, punishing the euro if the ECB fails to raise rates and punishing it if it does. The euro’s fall won’t be limited to exchange rates against other currencies, which to varying degrees face similar dilemmas, but it will be particularly acute measured against prices for commodities and essential products. Arguably, the euro’s derating on the foreign exchanges has already commenced.

But there is an additional factor not generally appreciated, and that is the sheer size of the euro’s repo market and the danger to it that rising interest rates presents. Demand for collateral against which to obtain liquidity has led to significant monetary expansion, with the repo market acting not as a marginal liquidity management tool as is the case in other banking systems, but as an accumulating source of credit. This is illustrated in Figure 4, which is of an ICMA survey of 58 leading institutions in the euro system.[v]

The total for this form of short-term financing grew to €8.31 trillion in outstanding contracts by December 2019. The collateral includes everything from government bonds and bills to pre-packaged commercial bank debt. According to the ICMA survey, double counting, whereby repos are offset by reverse repos, is minimal. This is important when one considers that a reverse repo is the other side of a repo, so that with repos being additional to the reverse repos recorded, the sum of the two is a valid measure of the size of the repo market. The value of repos transacted with central banks as part of official monetary policy operations were not included in the survey and continue to be “very substantial”. But repos with central banks in the ordinary course of financing are included.[vi]

Today, even excluding central bank repos connected with monetary policy operations, this figure almost certainly exceeds €10 trillion by a significant margin, given the accelerated monetary expansion since the ICMA survey, and when one allows for participants beyond the 58 dealers recorded. An important element of this market is interest rates, which with the ECB’s deposit rate sitting at minus 0.5% means Eurozone cash can be freely obtained by the banks at no cost.

The zero cost of repo cash raises the question of the consequences if the ECB’s deposit rate is forced back into positive territory. The repo market will likely contract in size, which is tantamount to a decrease in outstanding bank credit. Banks would then be forced to liquidate balance sheet assets, which would drive all negative bond yields into positive territory, and higher, accelerating the contraction of bank credit even further as collateral values collapse. Moreover, the contraction of bank credit implied by the withdrawal of repo finance will almost certainly have the knock-on effect of rapidly triggering a liquidity crisis in a banking cohort with exceptionally high balance sheet gearing.

There is a further issue to consider over collateral quality. While the US Fed only accepts very high-quality securities as repo collateral, with the Eurozone’s national banks and the ECB almost anything is accepted — it had to be when Greece and the other PIGS were bailed out. And the hidden bailouts of Italian banks by bundling dodgy loans into repo collateral was the way they were removed from national bank balance sheets and hidden in the TARGET2 system

The result is that the first repos not to be renewed by commercial counterparties are those whose collateral is bad or doubtful. We have no knowledge how much is involved. But given the incentive for national regulators in the PIGS to have deemed non-performing loans to be creditworthy so that they could act as repo collateral, the amounts will be considerable. Having accepted this bad collateral, national central banks will be unable to reject them for fear of triggering a banking crisis in their own jurisdictions. Furthermore, they are likely to be forced to accept additional repo collateral if it is rejected by commercial counterparties and bank failures are to be prevented.

The numbers involved are larger than the ECB and national central banks’ combined balance sheets.

The crisis from rising interest rates in the Eurozone will be different from that facing US dollar markets. With the Eurozone’s global systemically important banks (the G-SIBs) geared up to thirty times measured by assets to balance sheet equity, rising bond yields of little more than a few per cent will likely collapse the entire euro system, spreading systemic risk to Japan, where its G-SIBs are similarly geared, the UK and Switzerland and then the US and China which have the least operationally geared banking systems.

It will require the major central banks to mount the largest banking system rescue ever seen, dwarfing the Lehman crisis. The required expansion of currency and credit by the central bank network is unimaginable and comes in addition to the massive monetary expansion of the last two years. The collapse in purchasing power of the entire fiat currency system is therefore in prospect, along with the values of everything that depends upon it. The only sure-fire escape for the ordinary person is to physically possess the money of history that cannot be corrupted, and to which when the state theory of money is disproved yet again, becomes the only acceptable medium of exchange. That is physical gold and silver.

Geopolitical factors

This millennium, Kipling’s “Great Game” moved from the Central Asia of the nineteenth century and the Middle East to become truly global, with America and its close five-eyes allies on one side, and a coalition of China and Russia on the other. It also happens that the two protagonists are on different sides in the matter of money and currencies, with China and Russia having seized control over the world’s physical gold while America insists gold has no role in modern currency systems.Elsewhere, I have reasoned that China has secretly accumulated enormous quantities of gold, likely to be at least 20,000 tonnes, possibly even more, and its citizens have also accumulated a further 17,000 tonnes.

Briefly, the evidence is as follows. The Peoples’ Bank was mandated to acquire and manage the state’s gold and silver resources by regulation in 1983, an extension of its foreign exchange monopoly. Consequently, the PBOC had a clear run-in accumulating gold during the 1981-2002 bear market while China’s citizens were banned from owning both metals. In 2002, the Shanghai Gold Exchange was established and the ban on gold and silver ownership by the public was lifted. The Communist Party even advertised the benefits of owning precious gold, developing significant levels of public demand — hence public ownership estimated at 17,000 tonnes.

At the same time the State invested heavily in mining and refining. Consequently, from virtually nowhere China became the largest gold mining nation by far and has maintained that position ever since. No gold was permitted to be exported, and the only Chinese refined bars ending up at the Swiss refineries have been very few and believed to have been smuggled.

While we cannot be certain of the numbers, the evidence that the Communist Party has prioritised the accumulation of gold, and to a lesser extent perhaps silver, and now exercises a high degree of monopolistic control over Asian gold markets is irrefutable.

Similarly, President Putin has also prioritised the accumulation of gold, though his reasoning was partly driven by American and IMF sanctions in the wake of Russia’s invasion of Ukraine in 2014. Russia’s strategic vulnerability is in the payment for her energy sales, which is overwhelmingly in dollars — the currency of her enemy. Furthermore, under the correspondent banking system, the US has source intelligence of every dollar that is held by Russia and of all her dollar transactions. Putin’s response has been to unload dollars acquired through energy and commodity exports in favour of gold and other currencies.

Russia’s political strategy is to allay herself closely with China through the Shanghai Cooperation Organisation and other Asian political groupings, to jointly control the Eurasian landmass, and therefore the bulk of the world’s population. As the swing energy provider to Western Europe, Russia is driving a wedge between America and the UK on one side, and their NATO partners on the other. Currently, she is sabre-rattling on Ukraine’s eastern flank, but the intention is more likely to exploit the interests of EU member nations and remove the EU from the US’s sphere of influence.

Similarly, China is rattling her sabres over Taiwan and the South China Sea. This is also designed to bring pressure to bear on America. The common factor is Russian and Chinese assessments of the Biden administration, which they appear to believe to be fundamentally weak.

With respect to gold and silver, we can summarise the current geopolitical position as follows. Between them, Russia, China, and their Asian allies have gone a long way towards cornering the world’s physical gold markets. They are now testing the Biden administration, and Putin has a clear intention to isolate America from Western Europe. Meanwhile, the Fed is pursuing monetary policies which, unless reversed (for which there is no conceivable mandate) will inevitably hand economic power to China and Russia because of their gold-friendly policies. And if America and her allies cut up rough, through their joint domination of physical gold and its markets, China and Russia have the means to destroy the unbacked, fiat dollar.

Silver

Silver appears to be badly mispriced. There are several factors that can only lead to this conclusion.According to the Silver Institute, physical supply in 2021 increased over a depressed 2020 by 8% to 1,056 million ounces but remains below the output for 2014-2016. Meanwhile demand is up 15% this year at 1,033m oz leaving a marginal surplus of just 23m oz. The question obviously arises concerning demand patterns over the next few years at a time of accelerating investment in non-fossil fuel energy and electricity. For silver, increasing demand for electric vehicles and upgrading of mobile networks to 5G can be added to photovoltaic demand. Forecasting the balance of supply and demand is always difficult for silver because of substantial and unforeseen changes in usage (remember photography?), but it seems reasonable to assume that silver will be one of an elite group of beneficiaries from global environmental policies.

The mining industry faces additional cost burdens in many countries as they adjust their operations to comply with environmental, social and governance (ESG) regulations and guidance. International miners will be hampered in fund raising if they don’t comply, even for their mines in countries which have yet to formulate their ESG policies to Western standards. Higher costs such as those imposed by ESG compliance can be expected to force mines to extract higher grades to maintain cash flow, so only higher prices rising faster than costs will impart any value to lower grade ores. The effect of ESG is therefore likely to downgrade longer term mine supply forecasts.

Lithium Uranium and copper, three of the other beneficiaries of ESG, saw their prices rise in 2021. Lithium Carbonate prices are up 520% since January, Uranium rose 54%, while copper rose 25% on top of a strong post-March 2020 rise. In silver’s case, a swing factor is investment in ETFs which for the last decade has varied between 200-300m oz. By way of contrast with lithium uranium and copper, the silver price declined this year by 15%.

But as a measure of total interest, physical silver demand is the tip of a far larger derivative iceberg. According to the Bank for International Settlements, outstanding forwards and swaps total roughly 3750m oz equivalent between bullion banks, and there are further liabilities between banks and their depositors with unallocated accounts. In addition, there are 715m paper ounces in the regulated Comex silver contract, which with other regulated exchanges suggests that there are at least 4,500m oz of added long positions in derivatives, which is 20 times estimated net physical investment demand for this year. And that ignores regulated and unregulated options.[vii]

While it appears that industrial demand for silver is set to increase significantly, the pricing of silver in fiat currencies at one eightieth that of gold is also anomalous at a time of accelerating price inflation, more correctly understood as currency debasement. Mismanagement of monetary policies now virtually guarantees the death of fiat currencies, and the only salvation will be to replace or change them into credible gold substitutes, because most central banks have at least some gold in their reserves.

That being so, physical silver will reacquire a monetary role as supporting coinage. Its abundance in the earth relative to gold is said to be less than ten times, and its historical relationship under bimetallic standards was approximately fifteen to one. The demise of fiat currencies is likely to guide the gold-silver ratio towards these ratios, so the current ratio of eighty times is a blatant anomaly.

In the absence of an immediate crisis for the fiat currency regime, changes to the way banks treat derivatives for balance sheet purposes are likely to lead to a contraction of open positions. The introduction of the net stable funding ratio under Basel 3 regulations is designed to curtail derivative risk generally. The withdrawal over time of banks from trading activities because of the NSFR will reduce liquidity in both OTC and regulated derivatives, leading to greater price volatility. And the contraction of paper silver outstanding is likely to translate diminishing paper supply into increased physical demand.

Anecdotal evidence is that order books for silver from the refiners currently run into the middle of 2022, with large industrial consumers scrambling to secure supplies. Any surge in monetary demand is therefore set to have a disproportionate effect on silver prices to the upside.

Summary and outlook

The year just ending has been a bad one for investors in precious metals, but stackers expecting the next financial crisis will be rejoicing at the unexpected windfall from bullion banks suppressing prices. Naïve investors, if they had a rudimentary understanding of monetary inflation, were directed into cryptocurrencies, leaving gold and silver to those seeking genuine protection from upcoming monetary and economic developments. Furthermore, policy planners and their epigones managing markets have demonstrated a reluctance to embrace the facts about inflation or alternatively are simply clueless.The establishment has provided a window of opportunity for ordinary folk to insure against the financial and economic events now so obviously ahead of them. Those who have a grasp of basic economics and deploy common sense understand that interest rates will now rise, and soon. And with extraordinarily high negative bond yields, financial markets are more mispriced for this eventuality than in any time in recorded history.

There can be little doubt in dealing with the inevitable market shock ahead that central banks will continue to issue increasing quantities of their currencies in a vain attempt to stabilise their economies and to ensure government deficits are covered. And with the increasingly likely collapse of the Eurosystem and its commercial banks, we can expect a “whatever it takes” inflationary response from the ECB.

As their world collapses around them, central bankers will act like bulls in a china shop, destroying their credibility and currencies even more as their panic increases. Against this background, buyers of physical gold and silver will do so not because they expect to profit from it, but to preserve something from the chaos in prospect, which will be triggered by rising, and then soaring interest rates as currency time preferences escalate and their purchasing power collapses.

[i] From “There are bad times just around the corner”. The couplet was that misery’s here to stay but it is an apt description of the effects of inflation.

[ii] At the time of writing M2 for November had not been released. It is therefore assumed to have risen moderately from the October figure.

[iii] See FLASH (Dec 10) at www.shadowstats.com

[iv] The Eurosystem’s balance sheet, that is the ECB’s plus those of the national central banks, has increased from €4,500bn in December 2019 to € 8,500bn today.

[v] ICMA European repo market survey No. 38.

[vi] The Euro system’s combined central banking balance sheet shows “Securities held for monetary policy purposes” totalling €3.694 trillion, and “Liabilities to euro area credit institutions related to monetary policy operations…” totalling €3.489 trillion at end-2020. Repo and reverse repo transactions are included in these numbers, and on the liability side represent an increase of 93% over 2019. It is evidence of escalating liquidity support for commercial banks, much of which is through repo markets, evidence that outstanding repos are considerably higher than at the time of the ICMA survey referenced above.

[vii] See BIS OTC derivative totals at https://stats.bis.org/statx/srs/table/d5.2

[iii] See FLASH (Dec 10) at www.shadowstats.com

[iv] The Eurosystem’s balance sheet, that is the ECB’s plus those of the national central banks, has increased from €4,500bn in December 2019 to € 8,500bn today.

[v] ICMA European repo market survey No. 38.

[vi] The Euro system’s combined central banking balance sheet shows “Securities held for monetary policy purposes” totalling €3.694 trillion, and “Liabilities to euro area credit institutions related to monetary policy operations…” totalling €3.489 trillion at end-2020. Repo and reverse repo transactions are included in these numbers, and on the liability side represent an increase of 93% over 2019. It is evidence of escalating liquidity support for commercial banks, much of which is through repo markets, evidence that outstanding repos are considerably higher than at the time of the ICMA survey referenced above.

[vii] See BIS OTC derivative totals at https://stats.bis.org/statx/srs/table/d5.2

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.