Gold and silver — Now it’s FOMO

Oct 17, 2025·Alasdair MacleodThe question facing dealers in precious metals is whether gold, silver, and PGMs have become Giffin goods. If so, further rises will create new demand with sellers retreating.

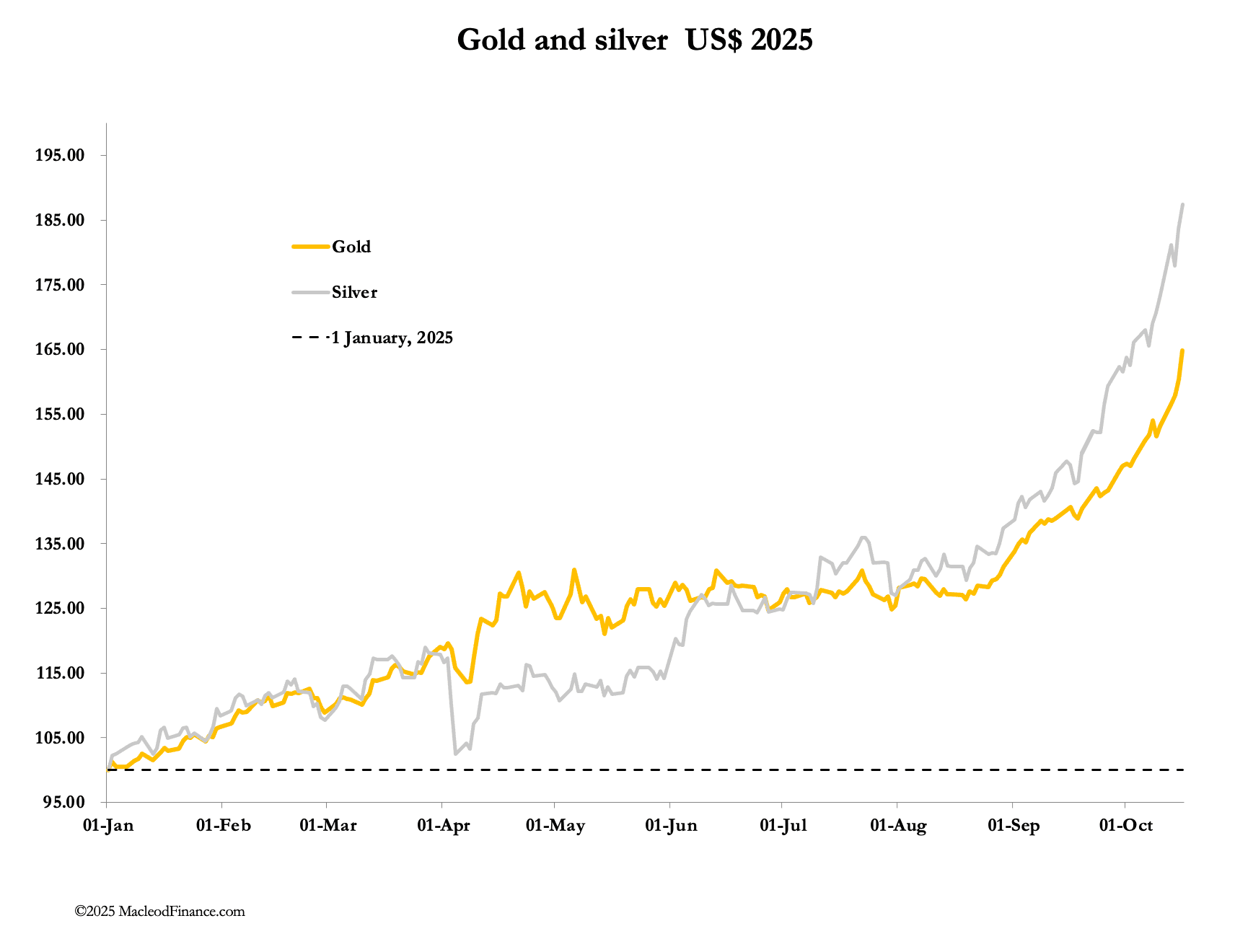

Gold and silver have had a rip-roaring week with their prices rising almost vertically. In European morning trade, gold was $4340, up $320 from last Friday’s close. And silver at $54 was up nearly $4. Adding to the sense of a gathering run on bullion stocks, reports from around the world are of queues of retail buyers no longer worried by high prices but seeking to buy small bars and coin in both metals before prices go even higher.

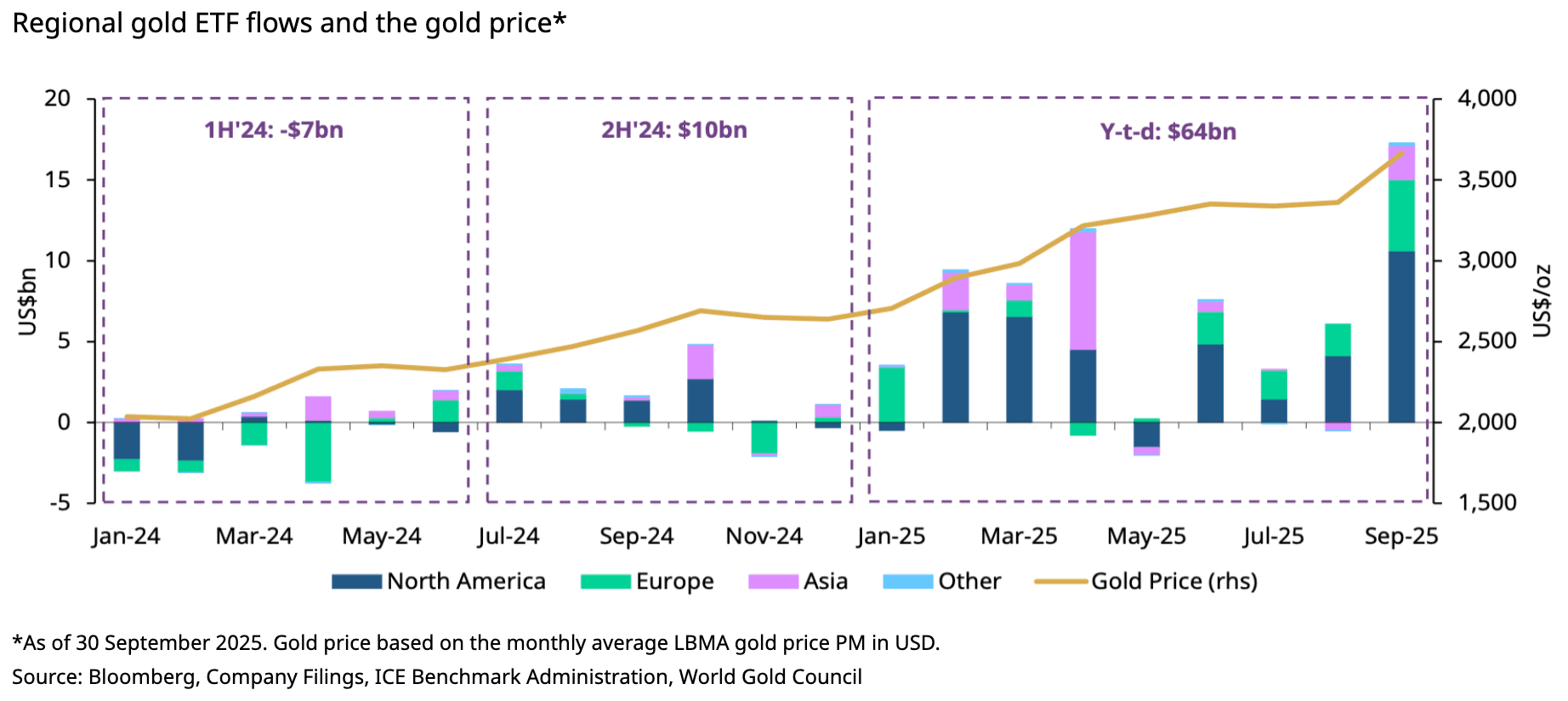

Investors are also missing out, belatedly buying into ETFs on a scale that’s still very small compared with the amount of investible funds. The chart below from the World Gold Council shows how September’s ETF inflows have jumped:

Backwardations between spot silver and the active Comex contract dipped to just under $1 over the last few days but have increased to $1.25 this morning, indicating that liquidity tensions are not going away. With that sort of arbitrage opportunity, you might expect traders to sell in London and buy on Comex. But the channel which reflects these transactions, Comex’s exchange-for-physical, are not spiking, which confirms there are no sellers in London at any price.

Meanwhile, Comex stand-for-deliveries are exceptionally high, with over 80 tonnes of gold and 560 tonnes of silver converted from paper since the beginning of the month. Furthermore, traders are still buying into the dying October contracts obviously as a means to obtain more gold and silver bullion. In the case of silver, this coincides with talk of aircraft shipments to London for the arbitrage.

Realistically, the likely size of London’s silver squeeze is too great to be satisfied by a few dozen planeloads of 10 tonnes a time. But silver’s disorderly market is not being replicated in gold, where lease rates and contangoes are more normal. So why is gold rising so strongly?

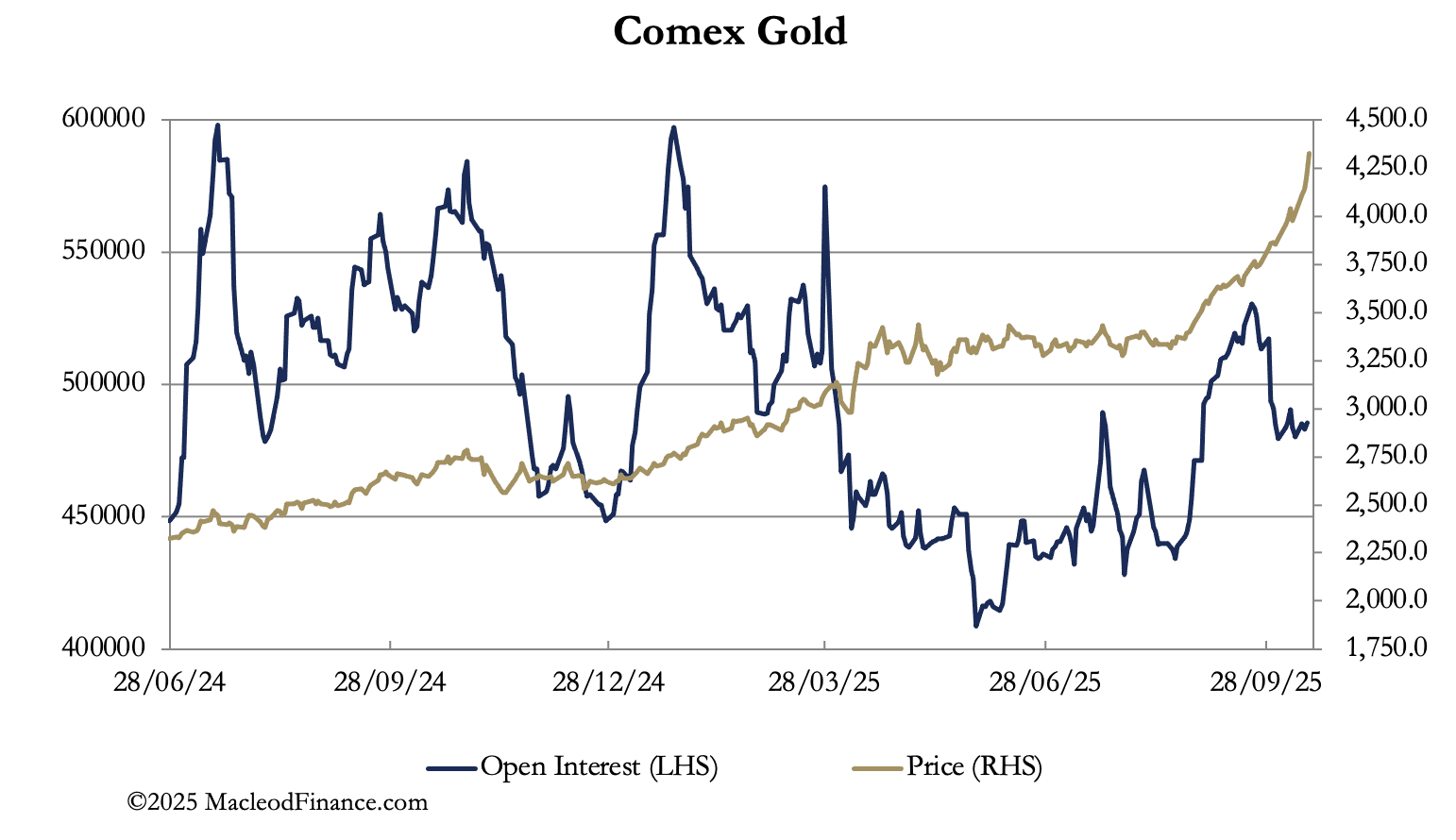

The bear squeeze still exists, as indicated in the relationship between Comex open interest and the price:

Note how there have been periods of falling open interest while the price has continued to rise. Rather than a rising price being driven by increased buying which is the normal relationship, there are times when open interest has contracted on a rising price. These can only be due to the swaps (mostly bullion bank trading desks) on Comex discouraging buyers by raising prices. It is particularly noticeable since mid-September, following which open interest fell significantly while the price has soared.

This unusual condition not leading to backwardations and soaring lease rates must be because the shorts on Comex are broadly hedged by longs in London. Most of this cover will be in forwards and options rather than in bullion. But there is greater underlying liquidity in gold than silver, so that the bullion banks are yet to face a squeeze on deliveries.

However, it should be noted that soaring lease rates and backwardations in silver are at the culmination of a squeeze, not its commencement. That prospect for gold is still ahead of us. And we should bear in mind that investors are only just beginning to buy into ETFs, and a continuance of this trend will eventually lead to a liquidity crisis in gold as well.

In conclusion, for gold the fat lady has yet to sing. But a pause in gold’s headlong rush can never be ruled out, because for short-term traders looking to short gold which they believe to be overbought it looks massively overextended.

Because the rise in the gold price is not being driven by speculators but by genuine hoarders, any dip in the price is likely to be bought, limiting downside. It may be more obvious in silver, though not yet in gold; but both metals appear to be turning into Giffin goods.

A Giffin good is one where rising prices choke off supply and generates more demand, reversing the normal supply and demand relationships. That is what small buyers queuing outside bullion shops are now doing, and less obviously are being followed by demand for ETFs.

It’s now FOMO — fear of missing out.