GDP targeting — realistic or not?

Aug 11, 2022·Alasdair MacleodThe failure of the Bank of England to contain consumer price inflation has become a topic for debate at a time of changing premiership. It is thought that Liz Truss will seek to address this failure if she is elected Prime Minister.

It has been suggested that she will consider changing the Bank’s mandate to targeting growth in nominal GDP. It differs from inflation targeting in that the latter is a combination of nominal GDP and consumer prices. GDP targeting advocates presumably think it is easier to achieve targeting GDP alone and letting inflation take care of itself. While this debate is currently restricted to the UK, do not be surprised if it surfaces elsewhere.

The fallacies behind this line of thinking are fatal to the concept. Not only is an institution which has already failed to manage inflation expected to manage GDP outcomes more successfully, but there is worrying evidence that the Bank of England is not aware of what GDP actually represents.

As well as the institutional failures, this article explains why targeting GDP is bound to fail.

Introduction

There have been some suggestions that Liz Truss, who looks increasingly like a shoo-in for the next Prime Minister, is considering changing the Bank of England’s mandate from inflation targeting to targeting growth in nominal GDP.

As a concept it has superficial attractions, particularly in the context of what GDP actually is. It is not economic growth, as erroneously stated by nearly every economist and media source, but growth in bank credit spent on items in the consumer price index. If you could effectively manage it, then from monetary theory alone it follows that there would be greater control over the general level of prices than trying to target both economic growth, represented by non-inflationary full employment, and a CPI inflation rate of 2%.

Immediately, we can see that there are two conditions needed to satisfy the concept: the actual ability to target nominal GDP, and the validity of monetary theory upon which targeting it is based. Targeting GDP assumes you can direct banks to abandon the factors that drive a bank credit cycle. Because changes in bank credit arise from the interaction of changes in credit demand and the banking cohort’s own psychology alternating between greed for profit and fear of losses, in practice targeting GDP is virtually impossible.

Furthermore, GDP is only part of the economy. The rest, to which bank credit is also applied is flows into assets, both financial and non-financial. It would probably require the nationalisation of the banking system and total state control over credit allocation. But that would bring with it a host of other difficulties, encapsulated in the failure of communism.

The second condition is the relevance of monetary theory in determining the relationship between the quantity of credit and the general price level. There is little evidence that it is valid. We all know that if you increase the quantity of something you dilute its effect. And what applies mechanically must also apply to money, currency, and credit. But we are not talking here of something physical, such as the ratio of bleach to water and the biocidal effect. Always, with a circulating medium, there is an overriding human consideration. For example, between 1944 and 1971, under the Bretton Woods agreement there was a substantial increase in the quantity of dollar currency and credit: legal money, that is metallic gold and silver coin did not circulate at all. Yet, under those conditions prices in dollars remained remarkably stable.

When the Americans then opted for the instability of their own currency by abandoning its tenuous link with gold, prices in gold remained relatively stable and the dollar adopted alarming price instability. Figure 1 illustrates the point with oil prices, which has also been true for the wider commodity complex.

This is not to say that priced in gold, oil did not retain some volatility after Bretton Woods, but the evidence is stark. Monetarism is not the answer to the relationship between bank credit and prices by a long chalk.

So far, we have not even begun to consider the mechanism by which control over GDP might be managed. The intention behind GDP targeting appears to be to give the Bank of England a new mandate rather than scrapping it in favour of a new institution. But the Bank has failed miserably to control price inflation. Giving a new mandate to the Bank is backing a failed institution.

The Bank’s only tools are setting interest rates and in recent years buying and selling gilts — selling them so far is only in theory, but yet to be done in practice.

Government spending and GDP

During the covid crisis, UK government spending rocketed to about 50% of GDP, though since then it has declined to an estimated 43% in the current fiscal year (to April 5th, 2023). With up to half of it being government, when targeting GDP it is extremely important to decide how to treat government spending.

Government economists are bound to argue that government spending is important in economic terms, and that GDP growth must include it. But being commanded, the state’s taxes reduce consumer-driven consumption, replacing it with the provision of services not freely demanded. You don’t have to look elsewhere for examples of how state spending is a burden on overall economic activity, and that successful economic management is to focus on the private sector, eliminating government as much as possible. Instead, the easiest way to bolster GDP is for the government to increase its inflation-financed spending.

This leads to a divergence of interests. While the two candidates for Prime Minister are falling over themselves to be free marketeers with proposals to reduce the state’s presence as a proportion of the total economy, the reduction in GDP that this entails undermines GDP targeting. This needs to be explained to a sceptical cohort of establishment economists and commentators.

Furthermore, the new Prime Minister must be prepared to force his or her spending cuts on a cabinet of spending ministers advised by civil servants whose default objectives are the maintenance of departmental resources. Most Conservative Prime Ministers have been appointed with a zeal to take an axe on spending and bureaucracy, but there is good reason why they never achieve it.

Additionally, international comparisons of national economic performance by economists from supra-national organisations such as the IMF and OECD make no distinction between government and private sector GDP. In other words, the international economic group thinkers must be refuted as well as the domestic Keynesian establishment.

Especially in the current economic environment, reducing government spending is not going to be a simple task. Besides high spending ministries such as health, education and defence always demanding greater financial resources, there is the problem of price inflation leading to public sector employee unrest. The public is likely to sympathise with doctors, nurses, and teachers whose state salaries are rapidly losing purchasing power. Already, we see demands for something to be done about energy prices, with the media not only sympathetic with the hardships inflicted on the poor by irresponsible monetary and geopolitical policies, but also firmly of the opinion that it is the government’s responsibility to do something about it.

Britain is entering a recession with higher interest rates, and therefore bond yields and debt interest. The government faces spending increases on universal credit, other welfare, social care, and state pensions. The lesson from the last contraction in the bank credit cycle showed that government spending as a share of GDP rose from 36% in 2006/07 to 40.8% in 2010/11. With this credit contraction threatening to be significantly more disruptive than that, the government share of GDP could easily exceed 50% in the next fiscal year.

At both the Treasury and the Bank of England there appears to be ignorance of the existence of the cycle of bank credit. How the combined offices of the state can formulate policy, whether it is to target consumer price inflation or GDP without this basic knowledge is beyond reason. Against these difficulties, targeting GDP as a means of managing the economy will almost certainly flop.

Why interest rate policy fails

The neo-Keynesian assumption adopted by central banks is that interest rates are the “price” of money through which demand for it can be regulated. This is at odds with time-preference theory, which posits that interest rates reflect the discount applied to the current value of money for the loss of its possession, until its eventual return. Factors additional to the loss of its use are the risk that some or all of it might not be returned, and of anticipated changes in its purchasing power.

Following last week’s increase in its lending rate to 1.75%, Andrew Bailey, the Bank’s Governor, stated that consumer price inflation could hit 13.3% later this year. If that is correct, then the Bank’s overnight lending rate appears to be far too low. But even this is the wrong metric. After all, currency in the form of banknotes, which similar to overnight money is a liability of the Bank, pays nothing. The rates to look at for time-preference comparisons are the yields of government stock, or gilts, along the yield curve. One-year gilts yield 2.06%. Ignoring counterparty risk and the loss of possession entailed, it should be yielding closer to 13%, being the rate of CPI change expected by the Bank.

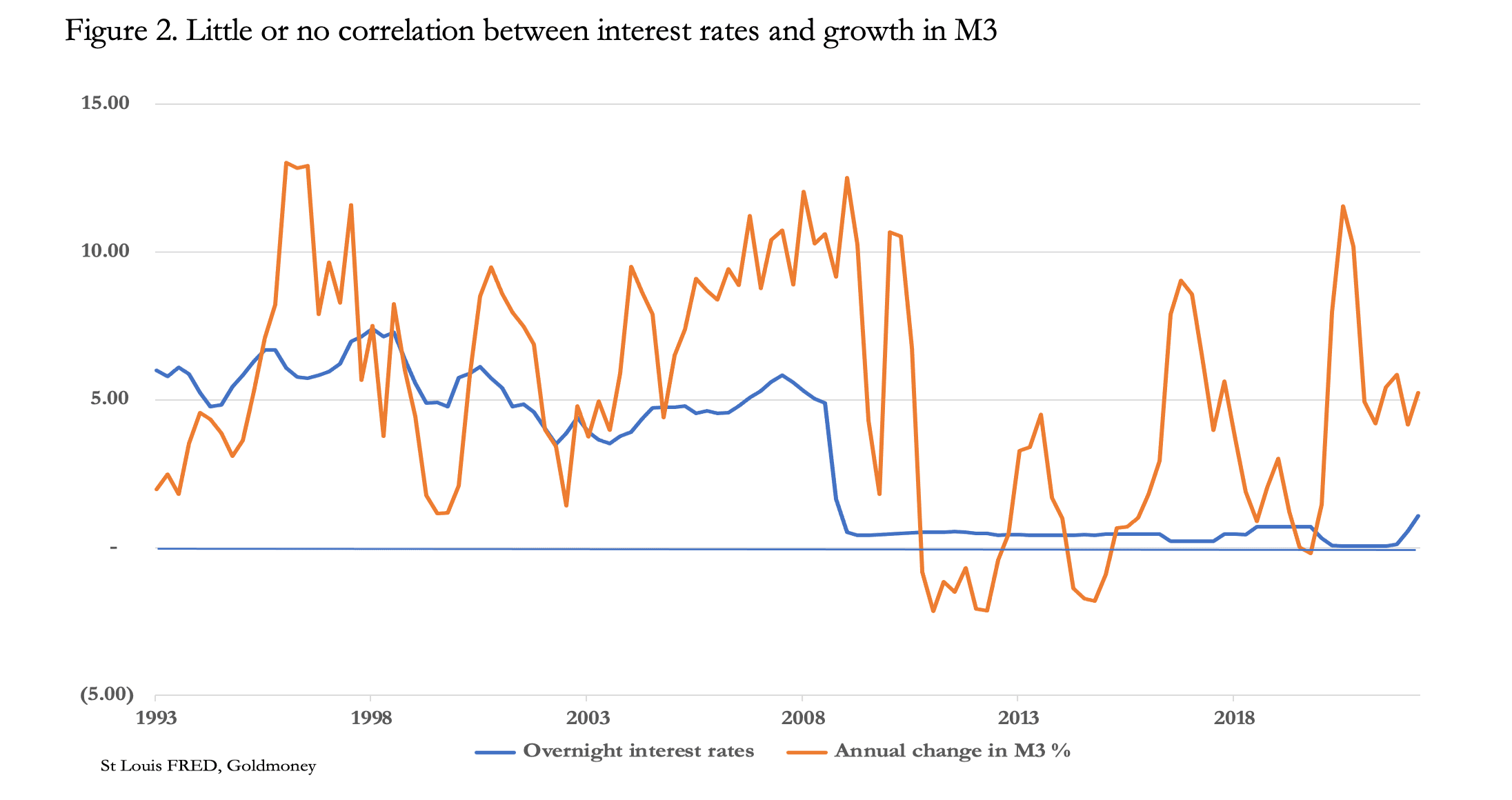

If only it were so simple. But we can say with confidence that gilt yields should be significantly higher than they are currently. That they are so suppressed and yet the economy does not appear to be booming is a sad indictment of monetary policy. It suggests that the correlation between interest rates, as the regulator of demand for credit, and the market for credit is non-existent. This is confirmed by the evidence in Figure 2.

It shows that interest rates cannot be the “price” of money, otherwise changes in overnight interest rates would generate the opposite directional changes in broad money. Therefore, interest rates can only reflect time preference. In which case, having distorted interest rates in the wrong quest, not only will interest rates fail as a tool to manage GDP, but they continue to fail to control consumer prices for the same reasons.

Bond market dealing fails as well

As well as interest rates, the other principal tool for monetary policy is quantitative easing and tightening. By buying gilts, the Bank of England injects currency in the form of bank credit into the sellers’ portfolios, principally pension funds and insurance companies. The intention is that this credit is passed on to other parties as the credit is reinvested. It amounts to an inflationary support mechanism for markets.

Not only do central banks see quantitative easing as a means of stimulating confidence in financial markets, but it anchors lower borrowing costs for their governments. And by suppressing yields along the curve, they also see it as a means of further stimulus once interest rates have hit their lower bound.

Presumably, policy makers would expect to be able to regulate GDP growth by market operations in the gilt market, buying gilts when GDP needs to be increased and selling them when it moves above target. But because financial assets are excluded from the GDP and CPI measures, any changes in total bank credit from the Bank’s market operations only affect these metrics indirectly.

The Bank of England bought a total of £895bn’s worth of gilts and bonds by the end of last year, since when they have instituted quantitative tightening by allowing holdings to mature, as well as by selling the minor quantities of corporate bonds they bought as part of post-Lehman QE. And last May, the Bank asked its staff to work on a strategy of actually selling some of the gilts on its books. As we shall see, with a recession in prospect that is unlikely to happen.

All QE is transmitted through bank credit, and at its peak it accounted for over 25% of sterling M3. Targeting GDP, which most analysts agree is beginning to decline, would require quantitative tightening to be abandoned and QE substituted in its place.

The oncoming recession

Understanding that GDP is simply the sum total of bank credit deployed in qualifying consumer items tells us why GDP in the UK is already contracting in certain lending categories, such as Manufacturing, and Wholesale and Retail sectors[i]. Bank balance sheets have become very highly leveraged, partly due to the impact on lending margins of suppressed interest rates, and partly because of extra debt incurred by businesses due to covid lockdowns. The suppression of interest rates is beginning to be unwound, and the covid epidemic has passed. Therefore, for bankers the current economic outlook is increasingly dire, and unless they act quickly to reduce their exposure to a contracting economy, their shareholders risk being wiped out.

There is little doubt that the cycle of bank lending is turning down. And even as the Bank’s Monetary Policy Committee is forecasting a 13.3% rise in consumer prices, independent financial analysts are talking of recession, and price rises rapidly falling back to more moderate levels. Furthermore, gilt yields have recently declined, with the ten-year gilt yield falling from 2.67% in late-June to 1.96% currently. In recent weeks, falling yields for government bonds are a global phenomenon, reflecting the current decline in oil and commodity prices.

At one level, we are seeing a repeat of the discrediting of Keynesian economics and perhaps the resurgence of monetarism which occurred in the 1970s. But so far, the MPC in its minutes rarely if ever mentions money supply. This is a serious omission, because GDP, outside the financial sector, is no less than bank credit., And commercial bank credit in one form or the other makes up 97% of total UK credit, the balance being bank notes.

Contracting GDP or recession — the same by different names

Contracting bank credit comes at a time when bank balance sheets are the most leveraged in history. With interest rates now rising, banks will be reducing their loan exposure to both financial and non-financial sectors for fear of loan losses. Not only will there be increasing pressure on the banks and those to whom they have loaned credit to liquidate financial assets, but the rising level of corporate failures is likely to apply further pressure for the withdrawal of bank credit.

In order to do some very rough estimates of the effect on the UK’s GDP, let us assume for a moment that there isn’t a banking crisis — an exogenous or endogenous shock. To restore the relationship of bank credit to shareholders’ capital to more conservative levels requires a contraction of bank credit of between a third and a half. That would put the average balance sheet assets to equity ratio for a British G-SIB at a more normal seven to ten times. The credit reduction would be split between credit for foreign operations, financial activities (including mortgage lending), and the qualifying domestic economy. GDP is directly impacted by withdrawal of credit from the domestic economy, with knock-on effects from the other two categories. This would probably result in an initial contraction of nominal GDP of between ten and fifteen per cent, without spill-over effects from credit contraction in financial markets and mortgage lending.

Even in the last credit downturn during and following the Lehman crisis, UK nominal GDP did not contract this much — it was only two or three per cent, as shown in Figure 2. Undoubtedly, it would have been greater but for the Bank of England’s intervention through its first round of QE. But this is only an initial effect.

Since the mid-eighties, the increasing securitisation and financialisation of the UK economy has led to banks relying more than they have in the past on financial asset values for their on-balance sheet activities and for collateral posted against loans. Rising bond yields will undermine these values as GDP declines, forcing banks to continue to withdraw credit. There is little doubt that the Bank of England will be required to indulge in QE on a far larger scale than seen heretofore, simply to stop GDP from contracting.

These conditions are global and will almost certainly lead to a banking crisis, if not originating in the UK likely to be in the euro system or Japan where balance sheet leverage for their global systemically important banks in both jurisdictions is at its highest, both averaging about twenty times. But as the non-US international finance centre, London and its banks will be in the eye of the storm. Therefore, it seems likely that there will be two policy difficulties facing the Bank of England. The first will be how to bolster nominal GDP, and for the second there is little choice: the Bank must be prepared to rescue the entire UK banking system.

This is where the simple Keynesian and monetary models are particularly mistaken in their assumptions of mechanical outcomes. In their interpretation of stalling GDP, the Keynesians assume that falling consumer demand will bring falling consumer prices, which must be avoided at all costs by renewed stimulation. With an appropriate lag in time, the monetarists express the same thing through the contraction of bank credit, for them measured in money supply. Their remedy is to foster the expansion of money at a moderate pace to offset deflation. Both arguments lead to forecasts of falling interest rates, concluding that to raise them now is a mistake.

But in both approaches, the human element is missing.

Prices are not mechanically related to currency and credit, a fact amply demonstrated in Figure 1 above, where under Bretton Woods prices were stable despite the massive post-war credit expansion. Following Bretton Woods, it was the currencies that become unstable rather than commodities in the absence of the fig-leaf of gold backing for the dollar.

With the purchasing power of fiat currencies already falling — and here we have to be careful with our definitions — the replacement of commercial bank credit by central bank originated credit through the banking system is likely to be judged in markets as a renewed acceleration of currency debasement. Public confidence in the fiat currencies themselves will almost certainly decline further, increasing prices of everything from commodities to consumer items. Reflecting time preference, interest rates and bond yields will also rise further, not fall with declining demand as the mechanical Keynesians and monetarists expect.

The precedent for this outcome is the John Law disaster, who was the proto-Keynesian who ruined France with his Mississippi bubble. When a scheme which uses credit in a fiat currency to foster a financial bubble fails, it is the currency that is taken down. Central banks have been following a carbon copy of Law’s scheme since the collapse of the dot-com bubble, if not before.

It is increasingly difficult to see how this outcome for currencies can be avoided. In addition to the difficulties of controlling GDP levels, there are mounting pressures on both energy and food supplies, threatening to drive not just the British into increasing poverty. Government ministers will be forced to respond, which inevitably leads to greater unfunded spending.

Conclusion

Attempts to move the Bank of England’s goalposts from managing inflation to nominal GDP exhibits a lack of understanding of why the Bank has failed so dramatically to control inflation. It commits policy errors shared by the other major central banks, enshrined in common group thinking.

It is clear from reading the minutes of its meetings, that the Monetary Policy Committee does not understand credit. They rarely, if ever, mention trends in money supply as a factor contributing to loss of the currency’s purchasing power. It is no exaggeration to state that the Committee fails to understand that rising prices is the manifestation of the currency’s declining purchasing power.

But most importantly, the Bank does not acknowledge the relationship between broad money supply and GDP. Nor does it comprehend that there is a cycle of bank credit, and in current conditions that the ratio between bank assets and equity are at an extreme. The consequences of rising interest rates, which have slipped out of the Bank’s suppressive control, will certainly lead to a reduction of bank credit and rapidly escalating systemic risks to UK counterparties to the euro system and Japan’s mega-banks, both of whose G-SIBs sport asset to equity ratios averaging twenty times.

The underlying problem the Bank faces is that the long period of financialisation of the British economy, originating from the big bang of the mid-1980s, is over. All the commentary from mainstream and government economists fails to recognise this change and its implications. The factors of demand for credit which has helped support the purchasing power of sterling along with that of other major currencies no longer applies. Instead, these economists persist with their Keynesian delusions of yesteryear. Economists, investment strategists and investment managers are living in hope that inflation will go away, and that interest rate increases will end not far above current levels before declining. Hope is not the basis for forecasting economic outcomes.

These same people would be the ones managing and observing attempts to achieve GDP outcomes. Having failed to deliver on their inflation mandate, there is no evidence they would be more successful if their goal posts are merely shifted. The failure is that state management of outcomes, which are the business of markets, merely defers and accumulates problems for the future.

The solution is to forget GDP targeting. Far better to reform the relationship between institutions of the state and markets, which means withdrawing the Bank of England from attempts to manage economic outcomes entirely.

[i] According to the Bank of England’s database.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.