FED talk

Oct 4, 2016·Stefan WielerFED talk

Introduction

Today’s sell off in gold has led to concerns that the >20% year-to-date rally in gold prices could begin to reverse. In our view this is primarily the reaction to renewed expectations that the FED is indeed prepared to raise rates again, which has led to large sell orders and pushed gold below a key technical level at USD1302/ozt. However, the asymmetry in the gold price outlook remains clear. There is very little downside to prices from here even if the FED raises rates multiple times over the coming year or two. Indeed, we see several triggers that could push gold prices sharply higher from here over that time horizon.

View the entire Research Piece as a PDF here...

Gold sold off more than 3% intraday today.

The sharp price decline came on the back of hawkish comments from Federal Reserve Bank of Richmond President Jeffrey Lacker today and Federal Reserve Bank of Cleveland President Loretta Mester yesterday. Mr. Lacker said today in Charleston, “While inflation pressures may seem a distant and theoretical concern right now, prudent preemptive action can help us avoid the hard-to-predict emergence of a situation that requires more drastic action after the fact,” thus urging the FED to raise rates before year-end. On Monday, Cleveland FED President Mester said in a Bloomberg TV interview that the economy is ripe for rate hike and highlighted that the November FED meeting should be considered a “live” meeting (although she added that she considers all meetings as “live”) and a November rate hike compelling, despite its close proximity to the US presidential elections. These comments have sent real-interest rate expectations as measured in 10-year TIPS sharply higher which pushed gold prices sharply lower (see Exhibit 1). Tuesday saw unusually high activity in the gold futures market. The hawkish FED talk triggered large sell orders, which pushed gold prices below the key technical levels of USD1300-1302/ozt, exacerbating the sell-off. This is something we have witnessed before.

Since the beginning of the year, the FED has tried to appear hawkish while the actual policy outlook has in fact become ever more dovish. At the end of 2015 there were 4 rate hikes expected and telegraphed by the FED in the FED dot-plot. The FED dot-plot shows the forecasts of each of the 16 members of the FOMC. Each dot represents a member’s view of where interest rates should be at for various timeframes, including a “long run” projection which represents where members think interest rates will be at the end of a hiking cycle. For 2016 the FOMC members expected 4 hikes (not including the first hike at the end of 2015). So far there have been none, and the FED members have continuously revised down their projections not just for this and next year, but also for the terminal (long run) rate. But every time after markets were disappointed by another zero round, some FOMC members came out with hawkish statements, and sometimes the FED minutes suggested that the FOMC became more hawkish. Every time the market reacted the same way: It pushed real interest rates higher and gold lower, and every time so far it was only temporary. Gold moved gradually higher, reflecting weaker interest rate projections.

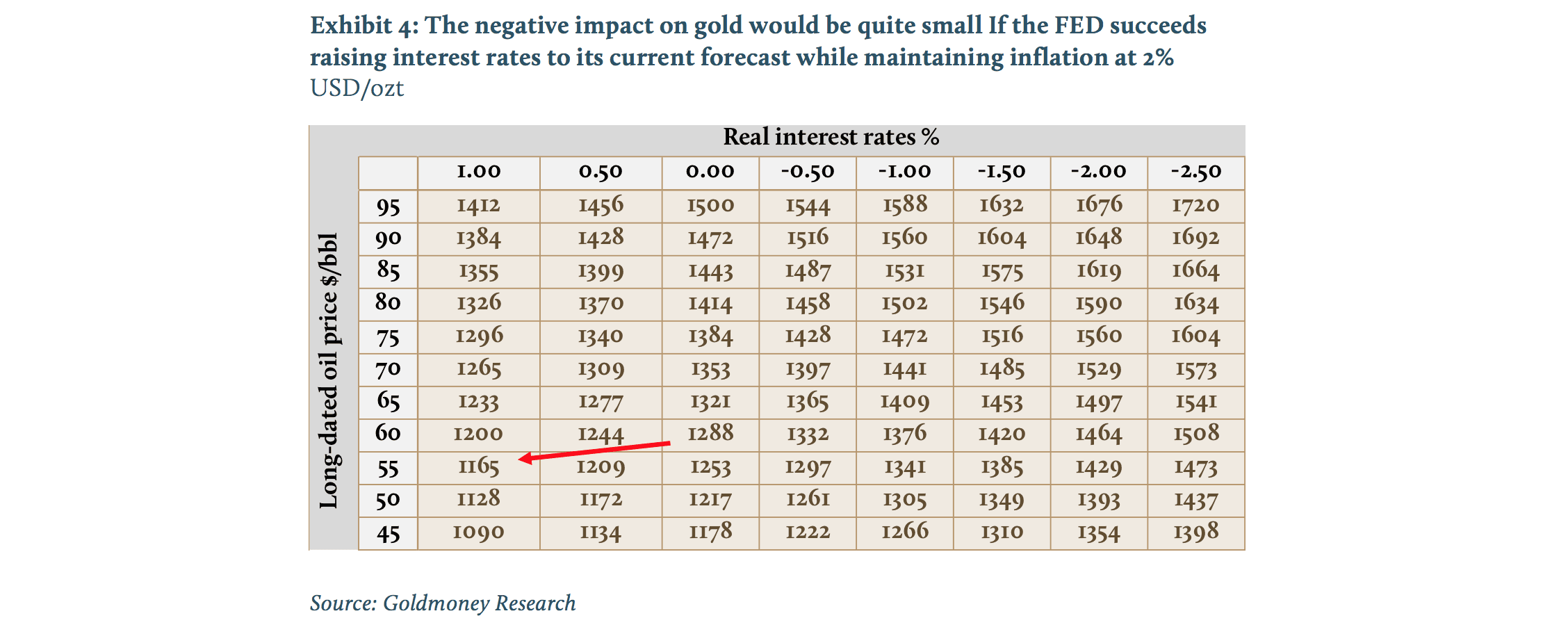

So what happens to gold when the FED actually raises rates? We think not much. The reason is that real-interest rates can’t really move much higher from here even if the FED raises rates. The FED’s own projection for terminal rates is now just 2.85%. The FED will most probably only raise rates if inflation reaches or exceeds its own target of 2%, which would imply that real-interest rates (currently at 0.04%) are capped at 0.85% over the long run. This upside limit on real interest rates sets the floor for gold prices and explains why its price outlook is skewed to the upside. Yes, if everything goes perfectly and the FED gets the chance to raise rates to its target over several years (without encountering any economic slowdown along the way) while maintaining a 2% inflation rate, then gold prices have a little bit more downside, but less than 10% (see Exhibit 4).

In fact, there are many more potential drivers to the upside.

1. The FED might increase its inflation target as already suggested by San Francisco Fed President John Williams. This means that real-interest rate expectations would become negative again even if the FED actually raises rates;

2. We start to experience an acceleration in broad based inflation as opposed to FED induced asset price inflation, pushing real rates back deep into negative territory;

3. The FED keeps delaying rate hikes and taking guidance for terminal rates even lower as it has done for years;

4. Any hiccup in the economy and the FED is forced to take rates lower instead of higher. Historically the FED has lowered rates several percentage points to counter recessions. At 0.5%, that would require steep NIRP;

5. Any renewed QE or new form of unconventional monetary policy such as ‘helicopter money’ would push gold prices sharply higher;

6. A renewed surge in longer dated energy prices (which bottomed in 1Q16, and we don't expect these levels to be retested) but is likely only to materialize in a few years.

Importantly, for gold to go higher from here it doesn’t need any Malthusian thinking. None of the scenarios above require a renewed global meltdown of financial markets or an even bigger event, such as a full blown currency crisis. The FED itself has simply set the floor for gold prices by revising its own guidance for rates to a point where the most hawkish scenario is that real-interest rates can only move marginally higher from here.

View the entire Research Piece as a PDF here...

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.