Fed pauses, ECB raises

Jun 16, 2023·Alasdair Macleod

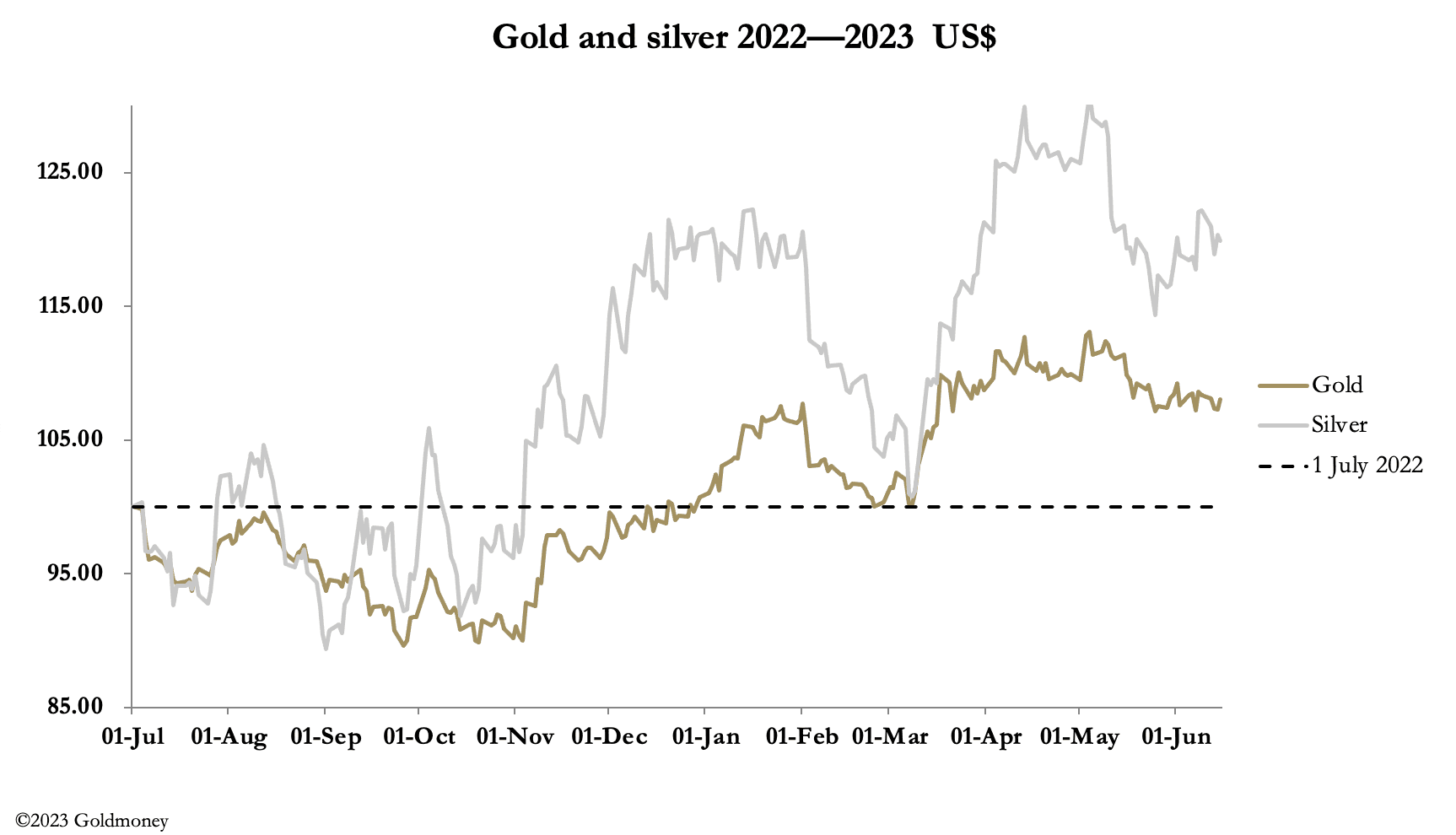

Gold and silver ended up little changed on the week after a sell-off in the Far East on Thursday morning, following the Fed’s decision to pause increases in interest rates. In Europe this morning gold was $1964, up $4 from last Friday’s close, and silver was $23.98, down 28 cents on the same timescale. Comex turnover in both contracts increased, indicating they were finding some support at these levels.

Gold’s action reflected speculator nervousness over how to interpret the Fed’s move, though it was as expected. The question on their minds was whether the Fed would resume its increases, having hinted that there are possibly one or two further rises to come. But the ECB’s rate increase yesterday, together with expectations of further rate increases by the Bank of England and others has undermined the dollar’s trade weighted index. This is next.

The decline from early March to test support at 101 was followed by a rally which peaked at the end of May, since when the TWI has resume its decline. That rally appears to be a Fibonacci 62% correction of the earlier decline, confirming it was most likely a rally in a bear market and that the 101 support will be breached.

The fundamentals leading to this possibility are in relative interest rate outlooks. Foreign exchanges now see a possible end to Fed hiking, while continuing at the ECB, the BoE, and elsewhere. The dollar will therefore be sold, and once it breaks below the 101 level on the TWI, subsequent falls could become significant.

This is particularly relevant for pairs traders — the hedge funds who buy or sell gold relative to the dollar. Therefore, on a break lower for the TWI, gold priced in dollars should rally strongly.

We are not there yet, but there is no doubt that a change is in the wind for currencies due to shifting relationships on interest rates. A weakening dollar might be seen to prolong the inflation problem, and rising bond yields everywhere are likely to lead to a resumption of bear markets for financial assets. Foreigners own nearly $25 trillion of long-term US dollar assets and will face a combination of a declining currency and falling asset values.

In BRICS+, increasing numbers of foreign governments and trading entities for the first time in living memory have in China’s yuan an alternative to the dollar for trade settlement. It could have the makings of a perfect storm for the dollar.

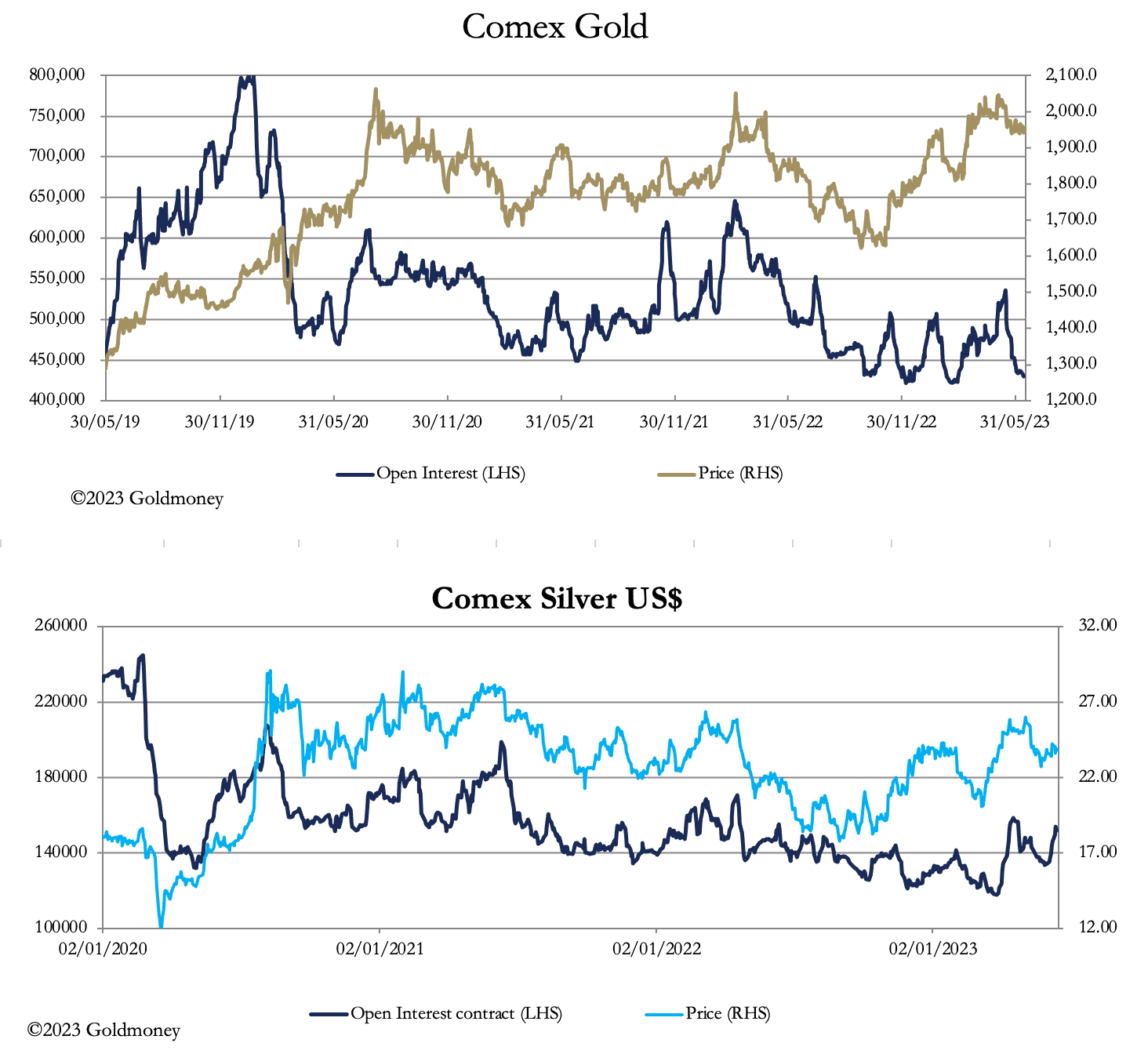

Meanwhile, there is an interesting divergence in Open Interest in Comex gold and silver contracts. This is up next.

While gold’s OI has fallen back to its lowest levels, silver’s OI has been rising taking the gold/silver ratio down to 81.8. This relative outperformance is visible in our headline chart and could be indicative of silver leading the way in a wider squeeze on the shorts, fuelled by solid physical demand.

And lastly, 30.7 tonnes of gold have been stood for delivery on Comex this month so far.