Fear Index April 2013 - the calm before the storm

May 3, 2013·Felix Moreno de la Cova SolisFor the second month in a row US M3 has remained basically flat at just under $15.1 trillion, despite the Federal Reserve continuing its monetary injections of $85 billion per month.

The Fear Index slipped slightly to 2.77%, while its 21-month moving average remained at 2.99%. The printing presses are warming up around the world with Japan’s Shinzo Abe vowing to achieve inflation at all costs and the ECB’s Draghi happy to give the eurozone economy a bit of extra oomph in a German election year.

The price of gold continues to see a worrying divergence between physical gold, with rising premiums and huge demand, and paper gold with routs and volatility in major financial markets. Paper gold and fractional reserve gold banking still set the price, but with paper gold 100 times more abundant than metal, it only takes a small percentage of gold “owners” demanding delivery to make the risk of selling unbacked gold promises materialise.

Most analysts and financial advisers continue to value gold as a commodity and actually try to explain the gold price in terms of mining production and average extraction costs. It bears repeating that with a stock-to-flow ratio of 65, with annual mining production accounting for less than 1.5% of the available supply of gold, looking at the profitability of miners and their margins as a way to value gold is almost completely useless. The use of this metric is a good way to signal ignorance.

The only way to value gold rationally is as money. The US Constitution still recognises it as such; states like Utah and Arizona have recently recognised it once more as legal tender, with a dozen other states planning similar measures.

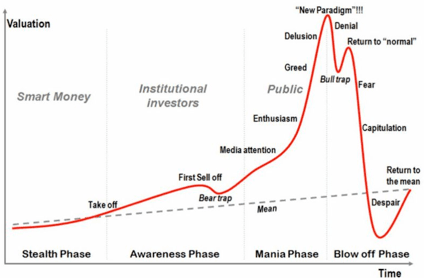

Nevertheless even money can be in a bull market or a bear market, so for those of you who simply cannot resist a bit of technical analysis, I suggest that you take a look at his classic chart.

Since most of the symptoms described here, like “media attention” are hard to measure, let us focus on something objective: participation. Gold remains tremendously under owned with less than 1% of managed money invested in it. Most pension funds hold no gold. The number of institutional investors with significant gold holdings can be counted on one hand, and most of these well-known names jumped in 2010 and 2011. Compared with some popular stocks which are sometimes mockingly called “hedge fund hotels” or to US sovereign debt which is still ubiquitous in pension fund balances, gold’s presence is marginal. So there is a strong case to be made that the gold bull market is currently at the "bear trap" stage and has yet to see its most explosive bullish phase.

With central banks around the world treating negative interest rates as the new paradigm, instead of the “extraordinary, temporary emergency measures” that they were called long, long ago, it is the debt and fiat money bubble that is looking very much like a crowded trade.