Drop Gold and The Myths We’re Told

Jul 20, 2020·Roy SebagAn inquiry into the monetary fitness of bitcoin relative to gold

INTRODUCTION

Since their creation in 2009, novel cryptocurrencies such as bitcoin have been met with skepticism and excitement. In recent years bitcoin proponents have begun to argue that their man-made technology service exhibits monetary fitness which is equal or, perhaps, superior to that of gold. The bitcoin community has begun advocating that ordinary savers should “drop gold”, which has served as the tangible money of man for thousands of years, for bitcoin, which they esteem to be a supersessory version of gold, acting, in their words, as “digital gold.” In this paper, we will investigate the attributes of bitcoin and, more specifically, bitcoin mining to test whether or not these claims are valid.

MONEY AS MEASURE AND REWARD, OPPORTUNITY COSTS, AND PROSPERITY WITHIN HUMAN COOPERATIVE SYSTEMS

Our objective in this paper is to investigate the monetary fitness of bitcoin in relation to gold and, more broadly, in relation to any tangible commodity which is useful. The term monetary fitness refers to the internal hierarchy of potential moneys according to a self-evident set of first-principles which are known to us through natural observation, measurement, and prediction. We define money as the singular measure and reward of acts of human cooperation which enables final satisfaction of transactions between two or more self-interested individuals. All things being equal, for any cooperative society to desire money over barter, money must be a neutral measure of human agency, by which I mean toil, aligning both individual agency and ambition with an objective, unchanging measure through time.

Individual human toil carries an opportunity cost in the metabolization of foods and fuels, with either a good or service produced as the consequence of that opportunity cost. Money as an objective and immutable measure of toil incentivizes the equitable merit-based distribution of rewards in human cooperative systems. Operating under such money, those who work harder and produce a greater surplus of skill or good are rewarded with more money relative to others. This dynamic, in turn, motivates everyone else to wake up the next day and work more or less hard depending on their personal circumstances and desire for self-actualization. This circuitous relationship between money as a measure and reward for independent acts of cooperation is what allows a complex, interdependent cooperative society to reward patience with merit, toil with leisure, and most importantly, to survive—that is to say achieve and maintain a state of collective prosperity and thus remain resilient through time.

We define prosperity as a state of surplus metabolic energy. Owing to the inherent laws of nature, any cooperative society must first be sufficiently fed, sheltered, and kept warm in order to avoid social and political upheaval and, thus, create an environment for productive cooperative action. Therefore, this existential demand in a non-clannish society must always be maintained. For just one example of the ramifications of a breakdown of this most foundational dynamic in any non-clannish society, look no further than Venezuela or even some western nations these days. It is important to stress that I am purposely avoiding the usage of abstract notions of “wealth,” “capital,” and other nominal measures when discussing prosperity. Such measures, employing the language of mathematics, may be helpful for communicating natural phenomena, but they do not explain the more fundamental first principles of human cooperation which I am focused on in this paper.

This existential requirement to maintain a surplus of metabolic energy necessarily demands that every day, acts of human cooperation must renew and continually transpire within the objective present because the past is entirely powerless, as are all cooperative acts which have taken place within it. As far as non-clannish human cooperation goes, it is only the future that matters. This is due, in part, to the self-evident reality that nature dictates all of the most existentially-mandated goods and services suffer from diminishing marginal utility through time—things grow up and then they die back down, food and energy resources cannot last in their most immediately useful state without the need for a continued investment of metabolic energy in order to preserve them. Because of this, in a non-clannish cooperative society where various self-interested individual human agents are dependent on others and have no altruistic predispositions to produce what they need the next day, week, or month, it is only money which survives into the new day as the measure and motivator of human cooperation.

We can see why time is the most important factor in this dynamic because the motivation of merit is achieved by instilling a sense of the future in the minds of cooperators in the present especially in the face of failure. Thinking about the future, planning for it, and working harder in the present in the aspiration of having to work less hard while enjoying more abundance in the future, is the natural human reaction to the ontological effects of time—which conquers all things and enforces that the powers of entropy pervade all things. The prospect of failure, being the closest embodiment of entropy, ensures that merit and resources–no matter how great–never remain permanent.

ESTABLISHING A FRAMEWORK FOR RANKING MONETARY FITNESS

Having sketched the general contours of money, human cooperation, opportunity costs, and prosperity we must now establish a framework for the ranking of monetary fitness. As we previously mentioned, any and all individual toil carries an opportunity cost in the expenditure of metabolic energy; foods and fuels. Consequently, the best measure and reward would need to display two characteristics: (a) embody the most metabolic energy relative other potential measures (b) effortlessly survive from the past through the present and into the future as an embodiment of that metabolic energy. Ultimately, both characteristics reflect some kind of relative natural scarcity which is self-evident to all cooperators. The higher a potential money ranks according to these two characteristics the more efficient it may be in measuring acts of human cooperation today and motivating future acts tomorrow.

At this point, it may already be clear why any service which lacks corporeality would be excluded from our ranking of monetary fitness. While a service most certainly represents the opportunity cost of metabolic energy expenditure no different than a good there is an important distinction. A service provided can never be divorced from the metabolic energy expenditure which powers it into existence. This presents a problem as our definition of money necessitates final satisfaction of transactions. Anything corporeal, be it an element or a good comprised of elements, circulates far after its original production within a human cooperative system allowing for it to be consumed, used, improved, or exchanged while never requiring the original expenditure of metabolic energy again. A good therefore relies on the first principles of natural law for its unchanging attributes as measurement and reward. A service as money bleeds into, limits, and consumes the prosperity (surplus of metabolic energy) of those employing it by enforcing its cost of existence into the measurement and reward of any and all acts of cooperation. Said differently, by virtue of its constant dependence on metabolic energy, any incorporeal service as money forces all cooperators to conform to open-ended and unpredictable future demands of the service as money. We already know this to be true for another service which functions as money in our present lives: centralized government issued fiat currencies but as we shall soon argue, it is equally true for cryptocurrencies which are decentralized privately issued technology services.

That corporeal “things” have the most equitably demonstrable monetary fitness is why luxury real estate is valued so highly. It is for this same reason that rare paintings, cars, and even shares in joint stock companies can appear to exhibit monetary fitness in relatively advanced societies. In any examples of monetary fitness which remain true to the first principles we have established, you shall find a claim on a corporeal metabolic energy embodiment which can be consumed, used, improved, or exchanged onwards. I freely admit that this is not always simple to see and that speculation, or short-term voting, as Benjamin Graham would famously state at times clouds our picture of the long-term weighing of said speculations. This being the case does not imply that modern economic thinkers should redefine money by rejecting the first principles. If anything, it amplifies why we should be striving harder to anchor our conception of money to first principles in our present day.

Having ruled out services, it should now be clear why our ranking of monetary fitness necessarily demands any potential money be first corporeal and if at all possibly, useful, as something to be consumed, used, improved, or exchanged. This corporeal thing must, as we have just explored, be capable of embodying a greater measure of metabolic energy than other things and effortlessly survive as an unchanging embodiment for longer than other things. In other words, we are seeking something which is rare and immutable relative to other things.

CORPOREAL ELEMENTS

Everything external to the mysteries of the human mind is corporeal, meaning that it is composed of a thing, matter, which we perceive through our human sense perceptions—smell, sight, taste, touch, and sound. This matter can be broken down to a certain observable quantity, at which point it is qualitatively distinct from others. These irreducible building blocks of matter are known as the elements, and, since ancient times, humans have been reasoning about the uniquely identifiable qualities that make one element distinct from another. While there have been many paradigms for describing the elements, today, these observable and measurable intrinsic qualitative attributes are codified within the periodic table of the elements. Think of the periodic table as merely a map providing us with a guide to knowledge which anyone could observe and confirm with their own senses.

This periodic table, introduced to most of us in grade school, shows that there are 88 naturally occurring elements that avail themselves to our sense perceptions.[1] Each element, from hydrogen to carbon to gold, has distinct qualities that are intrinsic. Some are rarer than others, some are toxic to humans, some are better conductors of electromagnetic energy, some are more malleable or ductile, some rust or evaporate, and so on. While the list is extensive, there are known limits to these qualities, and, more importantly, there is an immutable, that is to say unchanging relationship between distinct elements and their inherent qualities through time. Gold is always gold and is always rarer than copper which is always copper. Carbon is always carbon and is always more abundant than silver which is always silver. Each distinct element can be ranked according to its attributes and once this map of attributes has been understood the fixed relationships avail to us the natural order of monetary fitness inherent to all elements, which in turn, set the monetary fitness for all corporeal goods.

The immutability of the elements’ natural attributes is yet another mystery but it is one upon which all language, cooperation, and science is predicated, for it denotes that time’s irreversible arrow, from whence causation arises within the corporeal world, has observable, repeatable, and, thus, predictable laws, which allow us to conjecture about anything from literature to economics. In other words, we are capable of making reasonably reliable predictions about the future because we understand the intrinsic properties of the physical world made available to our common senses from past experience. The important point here is that predictability is endowed by fixed relationships between the elements within the natural order.

THE MONETARY FITNESS OF GOLD

As it relates to a deeper understanding of money and why gold is the best money nature has to offer, these immutable natural laws serve as the wellspring from whence productive natural inquiry must begin—the tectonic plate, or grounding, for our enlarged comprehension. If the corporeal world, and the elements which make it up, were not observable measurable, repeatable, and, thus, predictable, there would be no means by which to induce human cooperation, measure toil, and incentivize merit, which, as I have argued, is what fosters collective prosperity in a non-clannish human cooperative society.

What follows, then, is that the corporeal thing to serve as money must be rare, unchangingly so, which in turn, because it is a corporeal thing, allow the thing to embody the most amount of metabolic energy within the least amount of weight and volumetric space. Why are weight and volumetric space so important? Because scarcity sets the relative expenditure of metabolic energy or opportunity cost to extract, harvest, or acquire the thing. In other words, the relative physical weight and volumetric space directly correspond to the metabolic energy expended and thus embodied within the rare thing. The less physical footprint a thing embodies, the more naturally efficient it is to store, transport, exchange, measure, and trade—allowing it to become, if necessary, a decentralized, fungible measure and reward –money– which serves as a measure of toil and motivator of merit across time and space. Scarcity, weight and volumetric space, then, are critical features which avail to us an ordering of a thing within the prism of monetary fitness.

The less scarce and greater the physical footprint, the less efficient the thing will be. In economics, the term used to denote this phenomenon is “value density” but the reality here is that any person reading this paper can understand the logic in representing as much metabolic energy (that is to say their toil) in the most efficient thing through time (that is to say the least amount of physical space and weight). Interestingly, value density is what ultimately contributes towards a money proliferating throughout human cooperative systems, and, thus, becoming truly decentralized, which, in turn, leads towards independent cooperators transcending geographic locations, cultures, political systems, and time zones, to maintain a network of cooperation by virtue of their adoption of such money. In this case, we can once again see how incorporeal services, such as TCP/IP protocols, need not be required because the laws of nature already make this phenomenon possible in the most elegantly efficient manner in the form of something corporeal, at hand.

When I explain this feature of money to people, I often use the example of the shape of a sugar cube. A sugar cube of gold embodies a tremendous amount of metabolic energy (as measured in weight), which was required to extract the gold from the earth relative to all other elements using the same measure of weight (because it is both the rarest natural element with the highest specific gravity and, therefore, requires the most metabolic energy to extract by weight and volumetric space). That sugar cube also lasts longer on a relative basis to all other elements (because it does not chemically react when exposed to air). What follows is that the sugar cube of gold is more value dense than the same sized sugar cube of silver. If I were to employ my kinesthetic sense perceptions within any present moment, I would invariably reason that the gold sugar cube weighs more, even though visually, the two are identical in size and occupy the same volumetric space.

Weight is a property of the first principles of natural law, as is the metabolic energy embodiment which arises from natural scarcity—the relative abundance or lack of abundance of all elements to one another in the earth. It is for this reason that a tonne of copper last traded at $6,000 while a tonne of Gold last traded at $55 million in commodity markets. The same weight, two different distinct elements, occupying completely different volumes of space, and requiring completely different amounts of metabolic energy to extract. This is also why a tonne of gold occupies just two square feet of space, while a tonne of copper occupies a warehouse.[2]

An analysis of the Periodic Table of Elements shows us why gold, along with the precious metals platinum, palladium, and silver, are the rarest non-toxic natural elements which do not react with air. This means they will always require the most metabolic energy to produce, and, due to their relative scarcity, physically embody that energy in the least amount of space for the longest period of time. What results is that precious metals rank highest in monetary fitness, the ultimate embodiments of metabolic energy to be employed as a measure of toil and merit reward through time.

This relationship between natural scarcity (how rare one element is relative to another), specific gravity (weight), and diminishing utility through time (how long one element lasts relative to another), is the basis on which all exchanges of metabolic energy can be objectively reasoned and why we see precious metals serving as money since the oldest written account of a human cooperative society.

It is often at this stage that the skeptic will protest, raising questions about hypothetical elements or the ability to mine precious metals from asteroids. Both of these propositions stem from an unfortunate departure on the part of the applied sciences from that which is empirical and predictable to that which is incalculable and theoretical—the “ancient aliens” effect on modern science, if you will.

Both asteroid mining and the theoretical elements with half-lives of days or weeks, are, as far as anyone employing their common sense is concerned, nothing more than academic myths. We can imagine them, sure, but have we ever seen them? Do we have any observable reason to believe that they have ever existed or will perpetuate into the future in their same form? Other elements which made their way onto the periodic table over the last century are toxic to humans either through touch or inhalation. Others exist for a few seconds, enough for a scientist to name them as an element (such as the Seaborg elements). Before we pursue mining precious metals from the vacuum of space, we would have better luck mining them from the sediment in our ocean beds. There is a simple test which one should employ before discussing elements: as it relates to monetary fitness, we should be asking whether the element in question can be held in our hands, seen with our eyes, tasted with our mouths, heard with our ears, or inhaled through our nose. If it cannot pass this basic test, the element in question is useless in terms of its viability as money.

THE ABSENCE OF MONETARY FITNESS IN BITCOIN

We have thus far established a framework for monetary fitness and proceeded to rank corporeal elements according to their monetary fitness with the precious metals being money par-excellence according to our investigation. We must now proceed to ground our knowledge of bitcoin, bitcoin mining, and proof-of-work cryptography in order to test how proponents of this man-made invention, a technology service, argue for its monetary fitness.

My exposition of the soundness of money may have already alerted you to some of the similarities in the language which is used by evangelists of cryptocurrencies such as bitcoin. This is no coincidence but is rather the result of an organized attempt to proselytize the adoption of this technology service. The bitcoin community employs a term “proof of work” which ostensibly aims at satisfying our own definition “monetary fitness” which has, in one way or another, come to define money for thousands of years. Alas, as we shall now see, no matter the proof of work involved in the powering of cryptocurrency, the incorporeality of this technology service results in an absence of monetary fitness.

It is true that bitcoin was originally designed to mirror the properties of monetary fitness which have made gold the premier money throughout history.[3] It was precisely for this reason that I found myself involved with bitcoin so early on and why, even today, the thrust of my efforts in this paper are not advocating the idea that investors should “drop” it. The issue for me is that the bitcoin community cannot, on the one hand, base its entire future on the proof-of-work argument while maligning gold, which is the natural ideal which any proof-of-work technology service can only strive but can never embody. As I shall show in the remaining sections of this paper, pursuing this flawed intellectual path which disregards corporeality as the first-principle requirement of monetary fitness introduces a necessary comparison which, unfortunately for bitcoin, renders it inferior to not just gold, but any corporeal good made manifest in naturally scarce elements that survive through time. Ultimately, as we shall show, this hinges on the difficulties of any service to provide a human cooperative system with satisfaction finality as an unchanging measure and reward of metabolic energy.

Bitcoin is no different than any technology service from Amazon Web Services to Slack to Twitter. The delivery of any technology service involves some kind of opportunity cost, or proof-of-work, predicated on the exertion of metabolic energy (the energy expenditure in the form of researching, developing, and manufacturing the computers and servers, the electricity used by the computers that power the service, and the metabolic energy expended by the cooperators who support it). This exertion is an effective opportunity cost for a cooperative society’s surplus of metabolic energy, which, due to the continuous demands of the service, begins to consume the prosperity upon which it depends. With bitcoin, the situation is even more harrowing as the desire to make this service a singular money for the measurement and reward of all acts of corporations necessitates its continued demands for metabolic energy be always and everywhere met. This results in an inversion of the relationship between money as measure and motivator of renewed transactions each day which reflects the complex ebbs and flows of merit and failure within a cooperative society. Rather, this kind of money replaces prosperity as the lodestar which a cooperative society chiefly works towards. This is the difference between money sought for its own sake rather than money sought as a lodestar guiding prosperity. If the money being employed requires an increasing share of prosperity be always and everywhere allocated to it, that money as measure will colour economic calculations and predictions of the household which employs it. Again, we see no difference between this kind of money and government issued fiat currency, which has the same effect.

Without the act of “mining” bitcoins, there could be no bitcoins; not just new bitcoins, but all bitcoins. That is because the genius of bitcoin is also its achilles heel; its apparently decentralized properties which induce cooperation to secure a growing ledger of transactions requires that an increasing amount of metabolic energy be invested in the validation of mining blocks every few minutes. Each block serves a dual purpose of validating the latest transactions and, equally important, as the definitive ledger that tells every holder how much bitcoin they own. This interweaving of the payment systems with the actual ledger affirming who owns what is how bitcoin, as a technology service, attempts to emulate gold’s physical properties as being a measure of toil and motivator of merit. This fact also leads bitcoin proponents to argue that indeed bitcoin is even better than gold or “digital gold” to use their vernacular. This feature of the technology service is in actuality a bug and was achieved by mortgaging the future presenting a serious issue for bitcoin in the long-term.

The term “mining,” in this case, is really a misnomer. Instead of the word “mining,” consider the bitcoin proof-of-work hashing and block validation as a massive, continuous investment of metabolic energy to maintain the network. Without this investment, bitcoin is merely an abstraction—nothing more than lines of code, or, more specifically, mathematical operations that any ordinary person could simply write down with pen and paper.

THE DISTINCTION IN MONETARY FITNESS BETWEEN CORPOREAL GOODS AND BITCOIN

In contradistinction, gold is mined because it is naturally rare and immutable according to the first-order laws of nature. The act of mining does nothing to validate gold’s continued existence just as the act of breathing does nothing to validate the existence of oxygen. I can hold gold in my hand that was mined centuries ago and I can move that gold to any place I desire just as I can breathe oxygen anywhere I choose to live. My breathing of oxygen and my holding gold in my hand relies on the first principles of corporeality rather than the need to participate in a technology service built upon those first principles. That is why throughout history we have seen examples of other corporeal goods from livestock to shells serving as money. While varying corporeal goods will display varying degrees of monetary fitness, their existence at hand does not require an owner to buy into the continued investment of metabolic energy which went into making them. And as we previously established, to an owner, a corporeal good at hand provides maximum potential in consumption, utility, improvement, or exchange allowing them to respond to their individual desires for self-actualization when navigating their individual journey through merit and failure.

Mining more gold makes more gold available, which then circulates forever within and between human cooperative societies. There is no existential need on the part of gold for a continued investment of energy, and the gold, which serves as an embodiment of previously expended metabolic energy, can be worn as a ring or stored in one’s place of shelter. There is no shared ledger, and therefore nobody can truly know how much gold exists or is being owned at any one specific moment in time. That corporeal things depend only on the first order laws of nature is the truest expression of decentralization.

The point here is that gold and anything else which is corporeal doesn’t need to refer to a blockchain to know what it is or what it is not. Bitcoin and other cryptocurrencies require us to constantly divert our collective metabolic energy and time into supporting the integrity of a mathematical abstraction. This activity is, therefore, secondary to the first order laws of nature. When a farmer produces a crop, that action feeds society’s hunger. When a miner produces copper, that action powers society’s energy infrastructure. When a wildcatter discovers oil, it propels humanity’s transportation systems. When a miner decides to take risk and mine gold, that opportunity cost results in additional gold which can be used in computer chips to conduct electromagnetic energy without tarnishing or be employed as money—a lasting, objective measure for the other, more quickly decaying first order products of nature brought to any exchange in a cooperative system. Exchanging gold for something else provides satisfaction finality just as exchanging anything corporeal for anything else corporeal provides satisfaction finality.

Based on the experience of debating this issue for over a decade, I find that this concept has been very difficult to grasp for modern economists, academics, and members of the “service economy” but the simple fact is that it is a self-evident truth. On the other hand, I often find that primary cooperators such as farmers, fishermen, and miners have an easier time understanding this feature of our natural world. It is often members of the primary cooperative that recognize gold is no different than the tomatoes or the lithium or the apples they toil so hard to produce. It is a first order manifestation of human toil and merit arising from direct negotiation with nature.

The secondary cooperative, the “service economy” (to use the current expression), is where bitcoin lives. It is within this mathematical computation realm that crypto appears to be rare, appears to move around with ease, and seems to represent the realization of a long-lasting and immutable state. Alas, none of this is real. At the end of the day, bitcoin is nothing more than a poorly conceived monetary system which taxes metabolic energy rather than preserving it—a system that simply tries to mimic what nature has already perfected and made self-evident.

If the world’s gold miners stopped mining tomorrow, nobody that owns gold would care or even know. One gram of gold would remain one gram of gold. With bitcoin, the reality is entirely different. Any “owner” of bitcoin only owns what the latest version of the ledger says they own. That version exists based on the continued operation of massive computational servers somewhere requiring society to constantly divert its metabolic energy to maintain the apparent utility of the service. In this way, bitcoin, if it is to be used as money, forces itself in between human cooperation in the real world by competing with the prosperity which guides that cooperation.

Having laid out the first principles of why bitcoin, which is a technology service of the secondary cooperative, lacks monetary fitness, I shall now conclude my paper by providing several proofs that show how these first principles manifest in an actual comparison of gold to bitcoin. In so doing, we shall come to understand the true cost in operating a bitcoin monetary system.

THE COST TO MAINTAIN BITCOIN AS MONEY SERVICE TECHNOLOGY

As we have just explored, there is a fundamental distinction between an incorporeal service being offered and the corporeal things upon which the incorporeal service depends. A shoe factory depends on machinery, energy, and people to produce shoes which can circulate as a good thereafter. A shoe factory can work during the day and be shut down during the night, or it can be shut down or repurposed to another activity as the cooperators who support it navigate merit and failure. In all of these potentialities, the historic shoes produced by the factory bear no relation to the goings on in the factory today or tomorrow.

A technology service offers a service so long as the corporeal inputs upon which it depends continue to be consumed by the service. In this way the existence of the service is predicated on both the fixed and flow demand for corporeal inputs. This, as we already discussed, is an inherent limitation of incorporeal services. It is this first principle limitation which unfortunately many proponents of technology services from bitcoin to dropbox to social media struggle to appreciate. An example of this can be found in the ranks of those technology proponents who tout the internet’s existence as a virtual informational exchange network while conveniently disregarding that by 2025, 20% of all electricity will be used to support just the digital data storage requirement demanded by the internet.[4] Is it not clear, according to first principles, that the internet only exists as a virtual service because it consumes a tremendous amount of society's metabolic energy every minute, hour, and day? And is it not clear that in addition to the flow of energy constantly demanded by the internet, we must also consider all the equipment in the form of computational servers as well as all the people who support these services in the form of their own individual metabolic energy expenditures, for they all depend on the corporeal inputs from a segment of the cooperative society that produces them? Consequently, the internet most certainly provides society with a virtual informational exchange network but the cost to society is neither virtual nor free.

Bitcoin proponents build on this flawed understanding of an incorporeal technology service to argue that when one uses Bitcoin to store value or to affect a transaction, that act is virtual rather than physical. As we will now see, these statements amount to sleights of hand which are demonstrably false. When I use my smartphone to create a bitcoin wallet, transfer some coins in, and send them to a friend who’s using a smartphone halfway across the world, this activity may appear to be virtual to myself and my friend. The problem is that behind the virtual act, what is, in actuality, enabling all of this to take place is massive amounts of physical infrastructure in the natural world, comprised of computational hardware, energy transformers, physical space, and human computer engineers. That this infrastructure is not directly tethered to my act of communicating a transaction using the internet changes nothing.

It is intellectually dishonest, indeed it is a severe case of cognitive dissonance, to believe or otherwise misrepresent this fact—calling to mind that famous question posed by Berkeley: If a tree falls in a forest but there is no one there to see it, did it really happen? As it relates to bitcoin, yes, it is happening, and it is currently consuming more energy each year than all of the one hundred million citizens of the country of the Philippines combined.

At this point, a Bitcoin proponent may respond that, alright, the system may indeed exist in the physical world, and may even consume tremendous amounts of metabolic energy, but this is a positive feature for two reasons. First, it proves that indeed bitcoin shouldn’t be considered an incorporeal service, but a claim on corporeal equipment somewhere out there. Therefore, unlike the barber who offers a haircut as a service, with bitcoin, an owner has a claim on something tangible. Second, these physical activities are being carried out in a randomized and decentralized manner somewhere away from one's immediate field of vision. If bitcoin can still achieve the act of virtual payment efficiently as a native currency for the internet this physical activity should be viewed as a necessary cost. In other words, the cost being physically separated from the act makes bitcoin unique as a technology service which serves as money.

The weakness of this argument rests on a misunderstanding of the relations between the two points raised by our theoretical interlocutor. The first point deals with a claim on physical equipment somewhere but disregards the flow of energy constantly being demanded by the equipment. In bitcoin's case, this constant flow of energy demand is unlimited so long as the service is being offered, affecting the nature of bitcoin as a measure through time and therefore its ability to provide satisfaction finality for those employing it as money. The second point takes the decentralized nature of the physical inputs as a given and even as a strength which, if true, necessarily contradicts the first point. If the equipment is decentralized and that is a necessary cost, then no owner of bitcoin can claim to have possession over said equipment. If anything, the miner as the owner of the equipment has the bargaining power by offering the service and exacting both the flow and fixed input costs from those employing the service.

Let us dive deeper and see why these misguided claims about bitcoin are not only incoherent but result in the bitcoin proponent making several important concessions: the dependence of bitcoin as an incorporeal technology service on corporeal metabolic energy flows and fixed equipment.

Drawing on my experience in mining for cryptocurrency, I have taken a balanced perspective towards estimating the size and scale of the bitcoin infrastructure at the time of writing (June 2020).[5] I have chosen to be conservative in my estimations and have avoided making projections about the future, even though a present understanding of bitcoin's source code all but ensures future corporeal demands to be exponentially greater. I am simply trying to understand the cost to maintain the bitcoin network today, in the objective present.

We shall conduct our inquiry by focusing on the two demand inputs which the bitcoin service consumes in order to keep the service running:

1. The flow of metabolic energy required to sustain bitcoin.

2. The fixed corporeal equipment and volumetric space which is required to sustain bitcoin.

In this way, we shall come to understand not only the flow of energy, but the weight and volumetric space which the bitcoin system demands from society as an opportunity cost to power the money service.

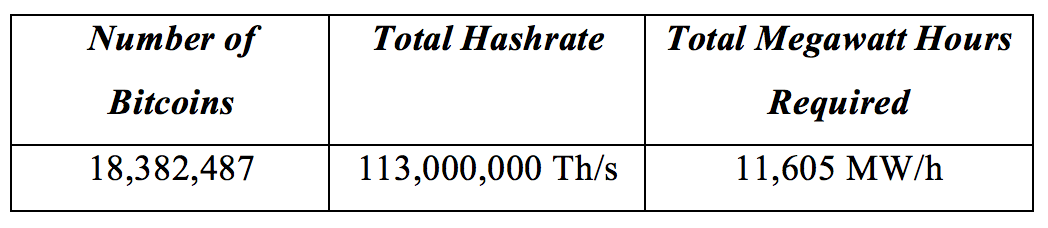

As of June 10, 2020, the key data-points associated with assessing the scale of the bitcoin network, and thus its computational and energy requirements, are:

The flow of metabolic energy required to sustain bitcoin

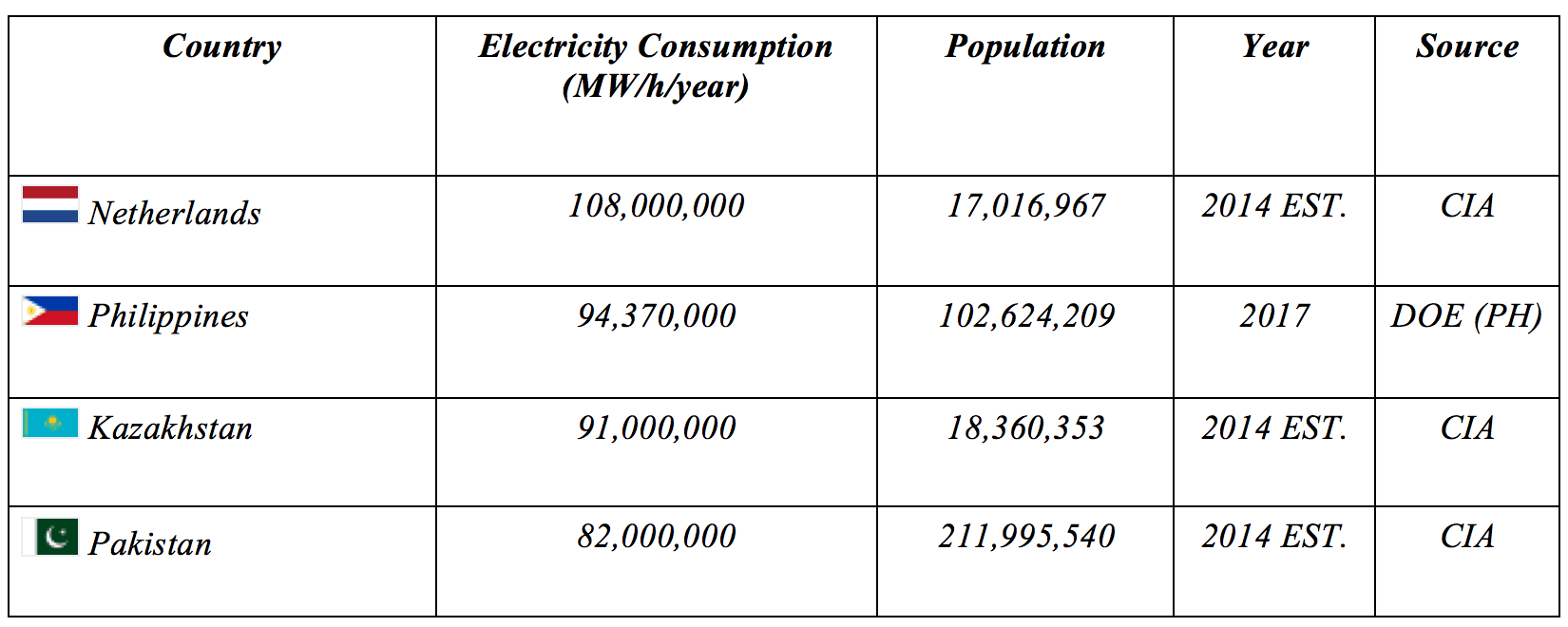

At its current hashrate of 113,000,000 terahashes per second (Th/s), the bitcoin technology service consumes 11,605 megawatt hours (MW/h) of electricity every hour. Consequently, the energy demanded by the service twenty-four hours per day, seven days per week, and three hundred and sixty-five days per year, would result in around 101,659,800 of MW/h. To understand the scale of this continued energy demand for a technology service which is just 11 years old, let us compare to that of entire countries.

Bitcoin already consumes as much flow energy, in the form of electricity, as countries such as the Netherlands, Philippines, Kazakhstan, or Pakistan. We can reason that in a country such as Kazakhstan which is heavily involved in the natural resource extractive industries or Netherlands which is involved in industrial production a large component of that electricity consumption is being used to produce corporeal goods. The Philippines and Pakistan, on the other hand, are interesting examples for they show us how little electricity per capita is needed in a society and therefore how material the electricity demand for bitcoin as a service already is today in relation to societal demands.

At the time of writing, the wholesale cost in US dollars of 1 Mw/h of electricity flow (excluding the capital cost of constructing the electricity generating system) is around $50. This indicates the ongoing cost of electricity at wholesale rates to merely run the bitcoin service is currently $5.1 billion dollars per annum. With the current US dollar value of the bitcoin service being $171 billion dollars, we gain an important insight which is that the cost of maintaining the energy flow demands of the bitcoin network at wholesale rates is circa 3% a year.

This calculation is the bare minimum in estimating the energy flow demand and as I have already mentioned assumes wholesale electricity rates while disregarding the capital cost in achieving those wholesale rates over time. Moreover, the opportunity cost to society in diverting this wholesale energy flow to a monetary system rather than other productive activities is likewise disregarded in these calculations.

These issues notwithstanding, we may begin to see that indeed there is a tangible cost to society for employing an incorporeal technology service as a monetary system. This is consistent with our first principles exploration of the distinction between an incorporeal service and corporeal goods as money. Let us then not dispute that as money, the bitcoin service taxes prosperity. This tax is very much real and certainly not virtual and as it relates to the instrument itself, represents an inherent decay through time for bitcoin, or in options parlance: “theta bleed.

The fixed corporeal equipment and volumetric space which is required to sustain bitcoin

We will now proceed to estimate bitcoin’s fixed corporeal demands in the form of equipment, weight, and volumetric space. We must first calculate the physical infrastructure required to maintain the bitcoin network. At minimum, we need to account for the specialized computer chips (known as “miners”), racks to support the computing infrastructure, and electricity transformers which harness and distribute the electricity from the grid into the computer equipment being employed. Without this basic equipment existing somewhere, consuming energy, and operating at all times, bitcoin as a mathematical abstraction ceases to exist. Given these inputs, let us now estimate the associated equipment and corresponding weights required to sustain the network at its present hash rate and energy flow demands.

By dividing the combined weight of 64,928,340 kilograms of hardware necessary to support the current hash rate of 113,000,000 terahashes per second by the 18,382,487 bitcoins in existence at the time of writing, we arrive at a ratio that mandates at least 3.53 kilograms of physical hardware residing somewhere in the world for every 1 unit of Bitcoin owned by someone residing in some other place in the world.

While Bitcoin proponents may rush to point out that a bitcoin is fungible down to one satoshi this does not change the fact that any abstract unit of bitcoin requires a greater amount of physical weight to power the unit into existence. Therefore, reducing the scale of abstract measure only increases the corpulence of bitcoin relative to anything corporeal and fungible from salt to gold. In this way a unit of bitcoin can be seen to be an indefinite, volatile, and changing measure.

Let us now consider how this differs from gold. Gold units can be measured in atoms with exponents in the “billion-billions”. No matter how big or small the unit in question, a gold unit corresponds to the same ratio of weight being represented by the unit. This makes gold an unchanging measure.

Our inquiry into relative weights has been instructive, but our conservative analysis excludes volumetric space. If we are to ultimately understand bitcoin’s monetary fitness relative to gold, we must incorporate the physical footprint that bitcoin as a money technology service occupies in the material world. In order to understand the volumetric space that the Bitcoin infrastructure occupies, we will engage in the following measurement:

• Total physical footprint required to house the 8,440,296 bitcoin mining chips (Bitmain S9 AntMiner), 4,642 transformers of 2.5MW each, racks and computing hardware associated with the 18,382,487 Bitcoins in existence at the current 113,000,000 terahashes per second network difficulty.

To calculate the physical dimensions that the bitcoin mining operations require, we need to propose a realistic layout for distributing the hardware in a manner that allows it to function efficiently. One cannot merely pack together transformers and S9 chips in the same way one can densely condense atoms of gold.

The most efficient layout that would also be representative of best practices in bitcoin mining these days is to conceptualize a wall of S9 mining hardware. We have been working with a total number of S9’s of 8,440,296, thus, in our calculation, we will assume the wall is 6 units high, resulting in 1,406,716 S9’s stacked side by side. Once the S9 mining hardware is installed and racked, there is a need for at least 3 feet of clearance on the fan intake side and the exhaust side, and a 6 inch gap vertically between S9’s for the power supply and cables, and a 0.6 inch horizontal gap between S9’s (accounting for the space occupied by the racks and supporting posts).

However, if we want to determine the physical footprint, that is to say the square meters or footage in terms of length times width, required to support this infrastructure, we must logically map out where each transformer would physically sit amidst our “wall” of S9’s. I can make a basic assumption that they sit at even intervals along the wall of miners. The power requirement would thus be 11,605 MW of medium to low voltage step down transformers. Using the 2.5MW format which steps down power to 240V, this would result in the 4,642 transformers of 2.5MW, each capable of supporting 1,818 S9 miners, stacked 6 feet high. In other words, for every 303 columns of miners, we would require a 5-foot safety gap, another transformer, another 5-foot safety gap, and then another wall of miners.

Bringing this all together, the resulting supercomputer capable of supporting the entire Bitcoin network would have the following dimensions:

What we have now discovered provides us with another important insight: bitcoin requires physical infrastructure that, if condensed into one physical location, would require a building which was at least 2 meters high and 237,170 meters wide. As we can see, to merely house the physical infrastructure, which gives life to bitcoin beyond the lines of code anyone could replicate manually, requires, at minimum, 33 million cubic feet or 946,627 cubic meters of volumetric space. These examples do not take into account additional costs in upgrading mining equipment. At the time of writing, most bitcoin miners are transitioning to the Bitmain S17 Antminer. This mining chip costs around $2,500. If we were to incorporate a transition from the S9 to S17 mining chips, we would gain some efficiencies in occupied volumetric space but at a cost of several billions of dollars in the purchase of new equipment.

Make no mistake about it, somewhere there are countless physical buildings housing all of this equipment. These buildings must be maintained through time if bitcoin is to be sustained into the future, and their number will only grow if bitcoin continues to exist, irrespective of the ostensible hard limit on abstract units available within the service.

COMPARING BITCOIN’S ENERGY FLOW AND FIXED VOLUMETRIC WEIGHT DEMANDS RELATIVE TO GOLD

At this point, a bitcoin skeptic may once again protest with the following argument: in order to assess gold’s physical footprint, one would need to include all the lands that are physically mined in the world, as well as the associated mining equipment. My response to this claim would be that based on years of experience in the gold-mining industry, over the long-run, a well-managed gold mining project terraforms back via reclamation with little disturbance to the natural world.[6] Therefore, in this case, land is not being employed indefinitely, and in terms of equipment, the equipment required to mine gold can be repurposed to mine any other important element or resource while the forms of equipment demands for the bitcoin service are specialized, fixed-in place, and cannot be repurposed for any other activity.

Once again, we can see how these objections ultimately reduce to the distinction between an incorporeal service constantly demanding corporeal inputs of energy flow and fixed equipment versus the production of corporeal goods which exist independently after the productive act. Essentially this brings us back to the understanding that gold is mined because it is gold while Bitcoin isn’t really being “mined,” but, rather, is being powered into existence via a distributed infrastructure of equipment, land, and buildings, which must always be dedicated to that one act lest the whole monetary system falls apart. Moreover, gold is actually somewhat ironically, an integral component in bitcoin “mining” equipment, making the element an existential ingredient in the bitcoin infrastructure for which no substitute is available. Gold does not need bitcoin in order to exist, bitcoin cannot exist without gold. The very computer chips used to “mine” bitcoin must conduct electromagnetic energy at 300,000 km/s–the speed of light–if they are to be effective. The only material conductor in existence which is capable of achieving this for the longest periods of time is gold. Therefore, in order for bitcoin to be “mined” at all, gold is a necessary input.

In contradistinction, no bitcoin has been or will ever be necessary in order to extract gold from the earth—nothing more than a pan or a pickaxe will do. This fundamental difference points not just to the primacy of gold over bitcoin (we can't have the latter without the former), but to the absurdity of using something which can, in and of itself, serve as a perfect money (gold) to create a manifestly inferior monetary substitute (bitcoin). By using gold in this way, we are taking something which perfectly realizes the intended outcome and using it to create something that diminishes from that intended outcome.

Having addressed the inherent differences between gold mining and bitcoin “mining,” let us continue into our analysis of comparing bitcoin to gold according to our first principles of monetary fitness. What should now be clear is that a more appropriate comparison is to inquire into the relative attributes of already-mined gold on the one hand, to the entire bitcoin service as it exists today.

While I am not a fan of estimates of the total gold stocks (for, as I mentioned, I believe it is a figure which is impossible to truly know, and the more important attribute is natural scarcity), in this instance, I believe it is instructive to rely on the general estimates of 171,000 tonnes.[7] With this weight of gold, we are able to estimate gold’s volumetric space. Unlike bitcoin, gold can be cubed by simply dividing the total weight by its specific gravity of 19,300 kilograms per meter cubed.

The result is that all of the world’s 171,000 tonnes of historically mined gold would fit neatly within a soccer pitch, a cube of approximately 8,860 cubic meters in volumetric space, which, due to gold’s densely packed atoms would measure just 20.7 meters on each side. All told, we arrive at the insight that at the time of writing: all the bitcoin-associated physical infrastructure already requires roughly 106 times more volumetric space than all the gold in the world would occupy. Therefore, the bitcoin service as money occupies more volumetric space than gold.

Let us now turn towards a comparison of the energy flow demands of bitcoin relative to gold according to first principles. As we have shown, if all of the world’s gold were to be cubed it would continue to exist into the future without needing to consume any further inputs of energy or fixed equipment. Now let us imagine billions of people rushing to the gold cube and chipping off a small piece then returning to their homes. They may do something with the gold such as fashion it into jewelry, manufacture a computer chip, send a satellite to space, or they may just hold on to it, knowing that while they wait for someone else to use it for some purpose in the future, their gold remains changeless as a measure and reward of their historic toil and merit.

A similar cube powering the bitcoin service requires a constant flow of energy and fixed equipment which grows with the adoption of the service. With bitcoin, it would be impossible to simply own a piece at hand with lasting satisfaction. Any owner of bitcoin can only make use of the service by communicating with their smartphone or computer thereby consuming even more energy and fixed equipment. This act of communication with the service is in effect its only use. As time goes by, the service demands more from its users and their share in the service must support the growing physical demands for more energy and more equipment. Consequently, their bitcoin is constantly changing as a measure and reward for their historic toil and merit.

This is the true distinction between gold as money, any tangible commodity as money, and an incorporeal service as money according to the first principles of natural observation, measurement, and prediction.

CONCLUSION

In this paper, we have delineated a framework for establishing monetary fitness. We argued that within our framework incorporeal services fail to adhere to the principal attribute of lasting satisfaction. By constantly demanding additional inputs of energy and equipment services as money compete with the prosperity of the society employing it.

We proceeded to show how corporeal goods, ranked according to our framework, exhibit varying degrees of monetary fitness with the rarest and longest lasting being the most fit to serve as money. We then showed why the precious metals ranked highest.

Having established that gold and precious metals were money, we attempted to compare bitcoin as an incorporeal technology to gold testing the claims made by bitcoin proponents in recent years. Our investigation showed that the bitcoin service consumes a tremendous amount of flow energy, physical equipment, and volumetric space to perpetuate its own existence. This amount grows and changes resulting in an actual definition of bitcoin as a volatile and changing measure and reward.

The price of bitcoin rising or falling would change nothing about our analysis for it was predicated on first principles. Conversely, skeptics who rush to argue that gold monetary systems are antiquated or representative of pre-digital era innovation should reconsider their position. It should now be clear to them that anchoring a digital ledger to physical gold requires minimal effort compared to bitcoin and that governments have ceased to do so for fiscal reasons rather than any inherent limitation arising from gold. The only impediment to reimplementing a gold monetary system today by any government in the world is the requirement to transparently reserve a unit of money in circulation to a weight of gold. Therefore, nobody who owns gold should be dropping it for bitcoin. The arguments that bitcoin is “digital gold” are nothing more than myths, no different than the ones of alchemists successfully turning lead into gold in the pre-enlightenment era.

[1] https://www.thoughtco.com/how-many-elements-found-in-nature-606635

[2] http://demonocracy.info/infographics/world/Gold/Gold.html - It is important to note that in these visualizations, gold’s specific gravity is not being fully appreciated for there is space between the bars and pallets. As gold is melted it condenses and occupies less space.

[3]https://books.google.fr/books?id=WfUtAgAAQBAJ&pg=PA205&lpg=PA205&dq=Bitcoin+designed+to+mimic+Gold&source=bl&ots=bnTSEPW7AB&sig=ACfU3U39rU2kHtiaoB1tVL8Tiw4ZT5fjnA&hl=en&sa=X&ved=2ahUKEwjK2ur3iqDiAhXcAGMBHfgSDOEQ6AEwDnoECAgQAQ#v=onepage&q=Bitcoin%20designed%20to%20mimic%20Gold&f=false

[4] https://www.theguardian.com/environment/2017/dec/11/tsunami-of-data-could-consume-fifth-global-electricity-by-2025

[5] I would like to thank Aydin Kilic for his assistance with these estimates.

[6] https://www.youtube.com/watch?v=mEWIoMZQivw

[7] https://www.bbc.com/news/magazine-21969100

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.