Market Report: Dollar up, yields up, gold down

Nov 25, 2016·Alasdair Macleod

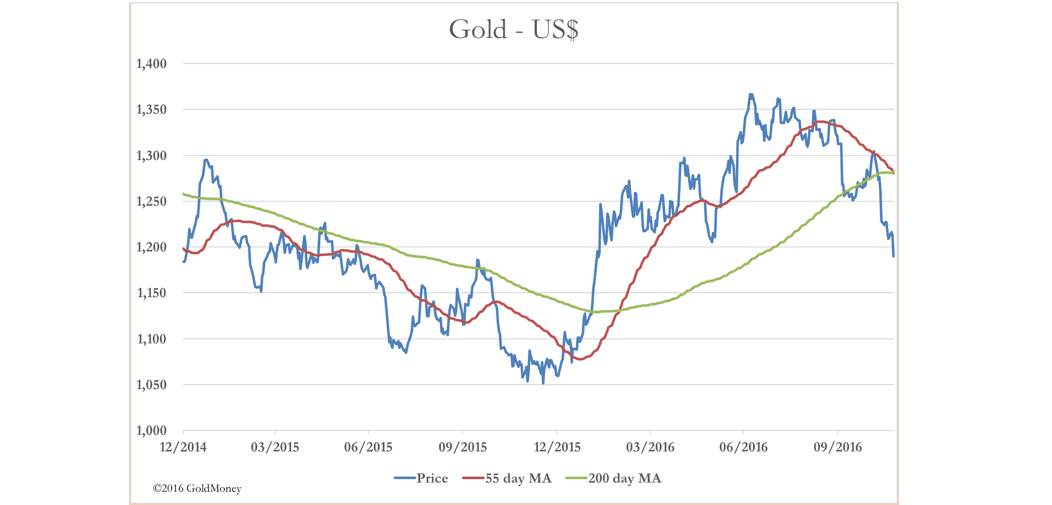

It’s been a torrid week for gold bulls, with prices sliding through the $1200 level, where some support could have been expected, only bottoming at $1175 in late-Asian trade last night.

In early European trade, gold seems to have found some support recovering to $1190. Gold is only up 12% on the year at these levels, and the Dow has now outperformed it. Furthermore, technical analysts will not be cheered by the next chart, which shows gold’s moving averages forming a death cross.

As one might expect, sentiment for gold has turned very negative. The rest of this market report looks at the factors involved, rather than short-term trading considerations.

The first thing to note is the collapse of Open Interest on Comex.

The situation has echoes of an earlier incident in April 2013, when the bullion banks mounted an operation to square their books in the wake of the Cypriot banking bail-in. At that time, there were mounting concerns about other Eurozone countries being forced to bail in their banks, leading to a flight of deposits from those deemed at greatest risk into German banks and to a lesser extent those in Luxembourg. These movements were reflected in growing Target 2 imbalances, so publicly known. What was not widely appreciated was the flight into physical gold, which had to be reversed to avoid a developing crisis in the bullion markets.

The bullion banks made it known to speculators and investors that a large market fall was in the offing, which had the effect of making market traders who were bullish, nervous and readily panicked. Either bullion banks or colluding hedge funds then dumped massive amounts of futures contracts on Comex, triggering an avalanche of selling from nervous bulls. The bullion banks managed to close their short positions profitably, and for them the threat was averted.

Fast-forward three years, and the bullion bank’s short positions were building again from the start of 2016. There has also been a revival of physical demand, reflected in ETF holdings and private purchases of bullion in Europe, leading to a repeat of the strains post-Cyprus. Open interest on Comex hit new records, with bullion banks short, and unable to close their positions. Brexit made things worse, then there was Donald Trump.

Under cover of market confusion about the outlook following the unexpected election result, bullion banks have managed to close most of their short positions. The fundamental explanation promoted by analysts is this: Trump is good for risk assets, so money flows from bonds and gold into equities and the dollar. A rise in the dollar index against other currencies is obviously negative for gold, and more so given the dollar’s rise appears unstoppable.

That is essentially a short-term argument, because Trump’s infrastructure spending and tax cut plans are inflationary. And inflation means a fall in purchasing power for paper currencies, which is ultimately positive for gold.

We can say with confidence that much of the fall in the gold price has been driven by bullion banks looking to square their books. We can also surmise that by driving the gold price below the 55-day and 200-day moving averages, technical analysts have turned uniformly bearish, triggering further selling. It therefore follows that when the bullion banks have long positions, they will be prepared for the market to rise as the inflation outcome develops.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.