China is killing the dollar

Sep 17, 2020·Alasdair MacleodIn the wake of the Fed’s promise of 23 March to print money without limit in order to rescue the covid-stricken US economy, China changed its policy of importing industrial materials to a more aggressive stance. In examining the rationale behind this move, this article concludes that while there are sound geopolitical reasons behind it the monetary effect will be to drive down the dollar’s purchasing power, and that this is already happening. More recently, a veiled threat has emerged that China could dump all her US Treasury and agency bonds if the relationship with America deteriorates further. This appears to be a cover for China to reduce her dollar exposure more aggressively. The consequences are a primal threat to the Fed’s policy of escalating monetary policy while maintaining the dollar’s status in the foreign exchanges.

Introduction

On 3 September, China’s state-owned Global Times, which acts as the government’s mouthpiece, ran a front-page article warning that

"China will gradually decrease its holdings of US debt to about $800billion under normal circumstances. But of course, China might sell all of its US bonds in an extreme case, like a military conflict," Xi Junyang, a professor at the Shanghai University of Finance and Economics told the Global Times on Thursday”[i].

Do not be misled by the attribution to a seemingly independent Chinese professor: it would not have been the frontpage article unless it was sanctioned by the Chinese government. While China has already taken the top off its US Treasury holdings, the announcement (for that is what it amounts to) that China is prepared to escalate the financial war against America is very serious. The message should be clear: China is prepared to collapse the US Treasury market. In the past, apologists for the US Government have said that China has no one to buy its entire holding. The most recent suggestion is that China’s Treasury holdings will be put in trust for covid victims — a suggestion if enacted would undermine foreign trust in the dollar and could bring its reserve role to a swift conclusion.[ii] For the moment these are peacetime musings. At a time of financial war, if China put her entire holding on the market Treasury yields would be driven up dramatically, unless someone like the Fed steps in to buy the lot.

If that happened China would then have almost a trillion dollars to sell, driving the dollar down against whatever the Chinese buy. And don’t think for a moment that if China was to dump its holding of US Treasuries other foreign holders would stand idly by. This action would probably end the dollar’s role as the world’s reserve currency with serious consequences for the US and global economies.

There is another possibility: China intends to sell all her US Treasuries anyway and is making American monetary policy her cover for doing so. It is this possibility we will now explore.

China’s commodity strategy: it’s also about the dollar

Most commentators agree that China has a long-term objective of promoting the renminbi for trade settlement. While China has made progress in this objective, they also agree that the renminbi will not challenge the dollar’s status as the reserve currency in the foreseeable future. Any changes in the relationship between the dollar and renminbi is therefore believed to be evolutionary rather than sudden.

Recent developments have dramatically altered this perspective. China is now aggressively stockpiling commodities and other industrial materials, as well as food and other agricultural supplies. Simon Hunt, a highly respected copper analyst and China-watcher put it as follows:

‘’ China’s leadership started preparing further contingency plans in March/April in case relations with America deteriorated to the point that America would try shutting down key sea lanes. These plans included holding excess stocks of widgets and components within the supply chains which meant importing larger tonnages of raw materials, commodities, foods stuffs and other agricultural products. It was also an opportunity to use up some of the dollars which they have been accumulating by running down their holdings of US government paper and their enlarged trade surpluses.

Taking copper as an example, not only will they be importing enough copper to meet current consumption needs but in addition 600-800kt to meet the additional needs of their supply chains and a further 500kt for the governed owned stockpile. The result of these purchases will leave the global copper market very tight especially in the next two years.’’[iii]

Other than the spread of Covid-19 lockdowns outside China, there was no specific geopolitical development to trigger a change in policy towards commodities, though admittedly relationships with America are on a deteriorating path. Rather than indulging in state piracy on the high seas, fears that the US could blockade China’s imports would possibly be achieved by American action to prevent Western corporate commodity suppliers from supplying commodities — in the same manner as America controls with whom the global banking system transacts.

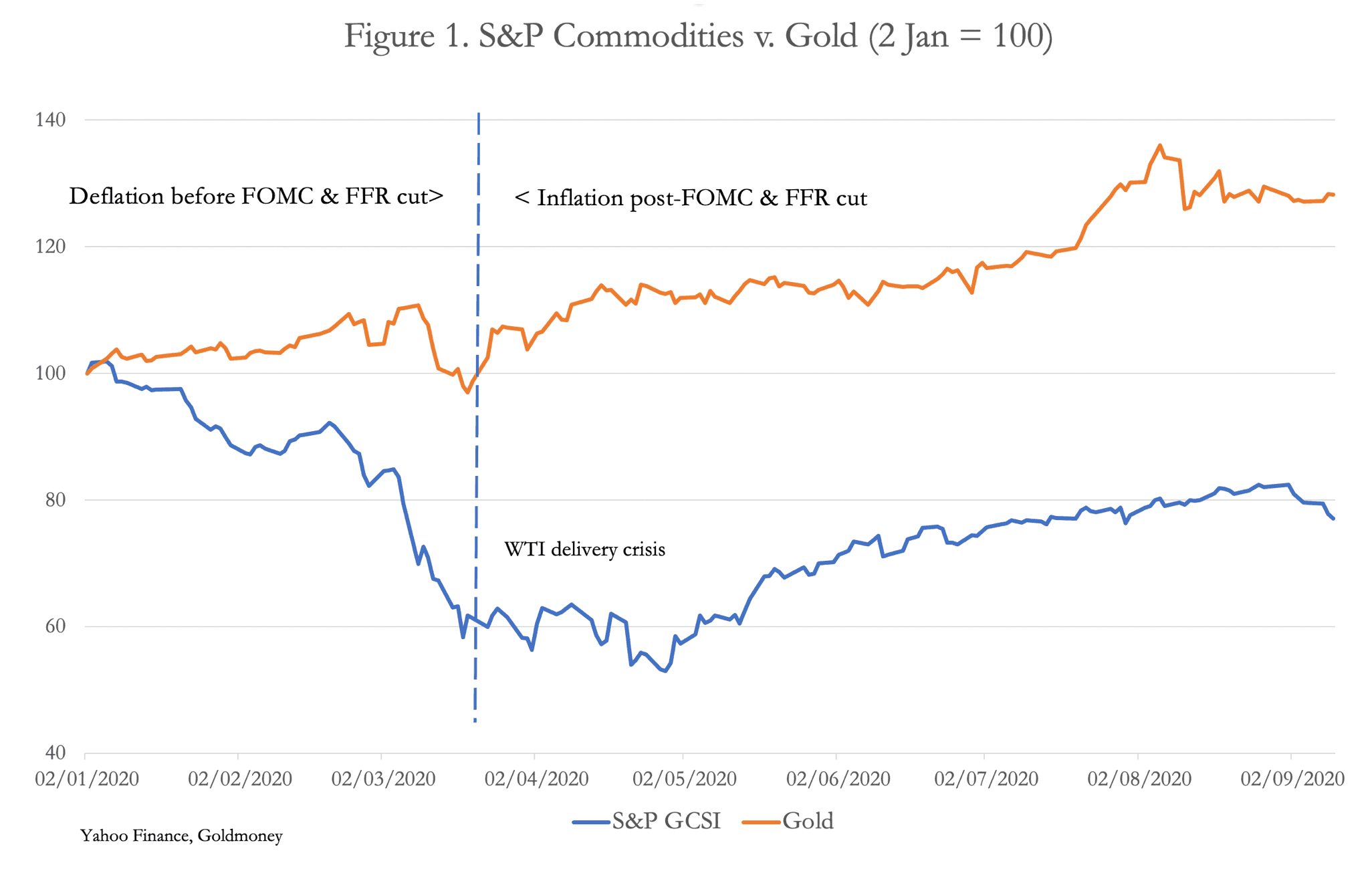

China has already agreed import targets for American soya and maize, only partially delivered, due one presumes, to waiting for this year’s harvest. She has been buying soya from other cheaper sources, such as Brazil, but it is too early to say China is holding back on American imports as part of a trade negotiation strategy. It is the timing of China’s policy to enact more aggressive purchases that is interesting: it coincided with or swiftly followed the Fed’s monetary policy change in late-March embarking on an infinitely inflationary course. Figure 1 points to this relevance.

The pecked line divides 2020 into two parts. First, we experienced the intensifying deflationary sentiment leading to the Fed’s rate cut to zero on 16 March, and then its promise of unlimited inflation in the FOMC statement which followed on 23 March. The second part is the inflationary period that commenced at that time as a consequence of those moves. The S&P 500 index then reversed its earlier fall of 33% and started its dramatic move into new high ground, and the dollar’s trade weighted index peaked, losing about 10% since then. Gold took the hint and rose 40%, while commodities turned higher as well, gaining a more moderate 20% so far. The gold/silver ratio collapsed from 125 to 72 currently, as the monetary qualities of silver resumed an importance. The S&P GCSI commodity index was initially suppressed by the WTI futures contract delivery debacle in April, but crude oil’s recovery has resumed. Both gold and commodities are clearly adjusting to a world of accelerating monetary inflation, where bad news on the economic front will accelerate it even more.

If China’s decision to increase the rate of importation for commodities and raw materials did occur at that time, it is very likely that rather than solely based on geopolitical reasons, the decision was driven by China’s reading of prospects for the dollar. When all commodity prices are rising, there can only be one answer, and that is the currency common to them all is losing purchasing power. And from its timing that is what appears to be at least partially behind China’s decision to accelerate purchases of a wide range of industrial and agricultural materials.

With a reasonable level of commodity stockpiles before 23 March, China might have taken the more relaxed view of buying additional imported commodities as and when needed. But the one stockpile she has in enormous quantities is of dollars, of which about forty per cent is invested in US Treasuries and agency debt. A short trillion or so has been loaned to trading partners, predominantly in sub-Saharan Africa and South America, as well as partners in the land and sea silk roads. The indebtedness to China of her commodity suppliers makes further protection from American interference more difficult perhaps, supporting the thesis of China dumping dollars. Furthermore, we should add it is possible that China has hedged some of her dollar exposure anyway. If so, against what is not known but important commodities such as copper would make sense.

That China owns and is owed massive amounts of dollars confirms her primary interest was in a stable dollar. In March she will have found that position no longer tenable. She has cleared the decks with the Global Times front-page article, which assumes America will continue to escalate trade and financial tensions, thereby ignoring China’s warning.

The likelihood that she has now abandoned a stable dollar policy has been missed by the mainstream commentary cited at the beginning of this article, yet the consequences for the dollar will be far-reaching. China is only the first nation using dollars for its external purchases to take the view it should get out of dollars as money and into something tangible. Others, initially perhaps other members of the Shanghai Cooperation Organisation, seem bound to follow.

The monetary consequences for America

The switch from a deflationary outlook to one of indefinite monetary inflation commits the Fed to purchase US Treasuries without limit. For this to be achieved will require the continued suppression of the cost of the government’s funding, which in turn will assume that the consequences for prices are strictly limited, and that existing holders of US Treasuries do not turn into net sellers in unmanageable quantities. If the Fed is to succeed in its monetary objectives it will be required to absorb these sales as well, which could be on a scale to ultimately defeat the Fed’s funding efforts.

According to the latest US Treasury TIC figures, out of a total foreign ownership of $7.09 trillion US Treasuries, China owns $1.073 trillion of which according to the Global Times $300bn will definitely be sold.[iv] But then there is the other matter of $227bn in agency debt, and $189bn in equities, which added to the remaining $800bn Treasuries after China’s planned sales tells us that there is a further amount of $1.2 trillion of securities that will be on the market “if China sells all of its US bonds in an extreme case, like a military conflict”. When an important holder begins to liquidate, others are sure to follow.

Until recently, the US Government’s funding has not presented a problem, because the trade deficit has not been translated into a balance of payments deficit. Foreign exporters and their governments have held onto and even added to their dollars, which is how they have ended up with $20.534 trillion in securities, together with additional cash at end-June as well as T-bills and commercial bills totalling a further $6.227 trillion.[v]

We know the relationship between trade and deficit nations’ demand for recycled monetary capital, because the relationship between the deficits and net savings form an accounting identity, summed up by the following equation:

(Imports - Exports) ≡ (Investment - Savings) + (Government Spending - Taxes)

The trade deficit is equal to the excess of private sector investment over savings, plus the excess of government spending over tax revenue. In basic English, if expenditures in the domestic economy exceed the incomes produced in it, the excess expenditures will be met by an excess of imports over exports. This is further confirmed by Say’s law, which tells us we produce in order to consume. If we decrease our savings and the government increases its spending, there will be less domestic production available relative to enhanced consumption. The balance will be made up by imports, giving rise to a trade deficit.

It follows that a decline in the currency can only be deferred for as long as importers are prepared to increase their holdings, in this case of US dollars, instead of selling them.

So far, we have not adequately addressed the impact on monetary policy, and how it affects prices in the context of trade imbalances and capital flows. We know from the relationship of the budget deficit with the trade deficit that other things being equal the rapid increase in the US budget deficit will lead to an equally dramatic increase in the trade deficit. This is not something the US Government is prepared to tolerate, and China would become even more of a whipping boy with regard to trade.

In terms of capital flows, China is disposing of dollars and buying commodities just at the moment the US’s budget and trade deficits are spiralling out of control. At the same time, she is adjusting her economic policies away from reliance on export surpluses to enhancing living standards for its population by promoting infrastructure spending and domestic consumption. By encouraging consumers to spend rather than save, the accounting identity discussed above tells us that China’s trade surpluses will tend to diminish, and consequently exchange rate policies will move from suppressing the renminbi exchange rate to make exports artificially profitable.

We can see this effect in Figure 2. Given the time between a central government directive and its implementation, the turn in the yuan’s trend in May seems about right in the context of a change of commodity purchasing policies initiated by central government a month or two before.

In the case of the US, the accounting identity which explains how the twin deficits arise informs us that in the absence of the balance of payments surplus which America has enjoyed heretofore we must consider new territory. If foreign importers dump their dollars there are two broad outcomes. Either the quantity of dollars in circulation contracts as the exchange stabilisation fund intervenes to support the exchange rate, thereby taking them out of circulation. Or they are bought by domestic buyers, at the expense of the exchange rate but remaining in circulation. It should now be apparent that attempts to maintain the exchange rate and accelerate monetary stimulation, which is the Fed’s post-March policy, are bound to fail.

Whether America decides to increase tariffs or ban Chinese imports altogether is immaterial to the outcome. The problem is rapidly becoming one of increasing quantities of inflationary money chasing a reducing quantity of American produced goods while imports are tariffed or blocked. And domestic production is also hampered by coronavirus lockdowns and the desire of bankers to decrease lending risk to the non-financial sector.

Anything the US Government does in an attempt to reduce the trade deficit without reducing the budget deficit is bound to lead to additional price inflation, or put another way, a reduction in the dollar’s purchasing power. We don’t know for sure, but it is reasonable to assume the planners in Beijing will have worked at least some of this out for themselves. If so, America’s exorbitant monetary privilege will no longer be at China’s expense.

It is increasingly difficult to see how a cliff-edge for the dollar can be avoided. Decades of benefiting from Part 1 of Triffin’s dilemma, whereby it is incumbent on the provider of a reserve currency to run deficits in order to ensure adequate currency is available for that role, is coming to an end. Those who cite Triffin tend to ignore the stated outcome; that Part 2 is the inevitable crisis that arises from Part 1. And with over 130% of current US GDP represented by dollars and securities in foreign hands, Triffin’s cliff-edge beckons.

China’s forward planning

If China is to prosper in a post-dollar world it must be ready to adapt its mercantile model accordingly. The evidence is that it planned a long time ago for this eventuality. Its Marxist roots from the time of Mao informed China’s economists and planners that capitalism would end inevitably with the destruction of western currencies.

Since those days, China’s economists have adapted their views towards the macroeconomic neo-Keynesianism of Western governments. While this is a natural process, the extent to which their earlier Marxian philosophy has been changed is not clear. And while this leaves a potentially dangerous lack of theoretical understanding of money and credit, we can only assume Western currencies are still viewed as inferior to metallic money.

It was Deng Xiaoping who led China following Mao’s death until 1989 and authorised monetary policy. And it was he who set China’s policy on gold and silver. On 15 June 1983 the State Council passed regulations handing the state monopoly of the management of the nation’s gold and silver and all related activities, with the exception of mining, to the Peoples Bank of China. Ownership of both metals by individuals and any other organisation remained unlawful until the establishment of the Shanghai Gold Exchange in 2002, since when it is estimated on the basis of withdrawals from the SGE’s vaults that publicly owned gold has accumulated to over 15,000 tonnes.

Since then, China has moved gradually but surely to gain control over physical gold markets and to become the world’s largest miners, both in China and through the acquisition of foreign mines. The Shanghai Gold Exchange dominates physical markets both directly and through ties with other Asian gold exchanges. Joining these dots leaves one dot concealed from us; and that is the true extent of physical gold owned by the Chinese state.

We can assume that China started from a position of some gold ownership when the 1983 regulations were enacted. The fact that precious metals other than gold and silver were excluded is in accordance with the Chinese view of gold and silver as monetary metals. And the permission for the general population to buy gold and silver on the establishment of the Shanghai Gold Exchange in 2002 suggests that in the nineteen years since 1983 the state had accumulated sufficient gold and silver for its anticipated needs.

In Deng’s time, foreign exchange activity at the Peoples’ bank was frenetic, with inward capital flows as foreign corporations established manufacturing operations in China. From the 1990s, while these flows continued, they were more than compensated by growing trade surpluses. Taking into account these flows and the contemporary bear market in gold prices, it is possible (though not provable) that the state accumulated as much as 20,000 tonnes.

Whatever the actual amount, little or none of this is declared as monetary gold. A strict policy of no gold exports has been enforced ever since — with the sole exception of limited quantities for the Hong Kong jewellery trade, which ends up being bought and reimported by day-trippers from the Mainland.

Even though state economists have increasingly used neo-Keynesian policies to artificially stimulate China’s economy, we should be in no doubt about China’s Plan B. It is not for nothing that she has deliberately taken control of physical gold and even run advertising campaigns through state media, following the Lehman crisis, urging her people to acquire it.

We cannot yet say when, how or if China will introduce gold-backing to ensure the yuan survives intact the problems faced by the dollar. But for now, with the new policy of a rising yuan illustrated in Figure 2 above, the impact on domestic costs for imported raw materials will be reduced and we can expect the yuan/dollar rate to continue to increase accordingly.

The implications

China’s threat to dump US Treasuries “in an extreme case, like a military conflict” is an important development for the dollar. It was a clear shot across America’s bows, and will have been seen in that context by the American administration. We have yet to see a response.

A firm plank of American monetary policy has been to suppress the price effects of monetary inflation. In the case of commodity prices, this has been achieved through the expansion of derivative substitutes acting as artificial supply. For the moment, the deteriorating outlook for the global economy persuades the macroeconomic establishment that demand for industrial commodities and raw materials will ameliorate, leading to lower prices. But this view does not take into account the changing purchasing power of the dollar.

At some point the threat to the dollar will be taken seriously. But before then, the political imperative in the run up to the presidential election is likely to continue and even intensify pressure on China. But China’s renewed determination to dump both dollar denominated bonds and dollars is a developing crisis for America and the Fed’s monetary policy. We can expect further threats to materialise from the Americans to China’s ownership of US Treasuries and agency bonds. It is a situation that could threaten to escalate rapidly out of control before China has disposed of the bulk of her dollar-denominated bonds.

The certain victim will be the dollar. And as the dollar sinks, China will be blamed and tensions are bound to escalate between China and her Asian partners on one side, and America and her security partners on the other. The start of this additional crisis was the turning point last March, when the Fed publicly stated its inflation credentials. With nearly $3 trillion in its reserves, it is not surprising that China is acting to protect herself.

With so much dollar debt and dollars in foreign ownership, it is hard to see how a substantial fall in the dollar’s purchasing power can be avoided and the Fed’s funding of the budget deficit badly disrupted.

[i] See https://www.globaltimes.cn/content/1199833.shtml

[ii] Tweeted by James Rickards (@JamesGRickards) 16 September: “There is one story that may be bigger than the elections, the riots, and the pandemic, but it will take a few years to play out. The U.S. will convert China's $1.2 trillion of Treasury notes to a trust fund for COVID-19 victims and for economic damages. Bye-bye China reserves.”

[iii] Private email correspondence with Simon Hunt of Simon Hunt Strategic Services

[iv] See https://ticdata.treasury.go/Publish/mfh.txt

[v] See https://ticdata.treasury.gov/Publish/bltype.txt

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.