Bond yields soaring

Jul 7, 2023·Alasdair Macleod

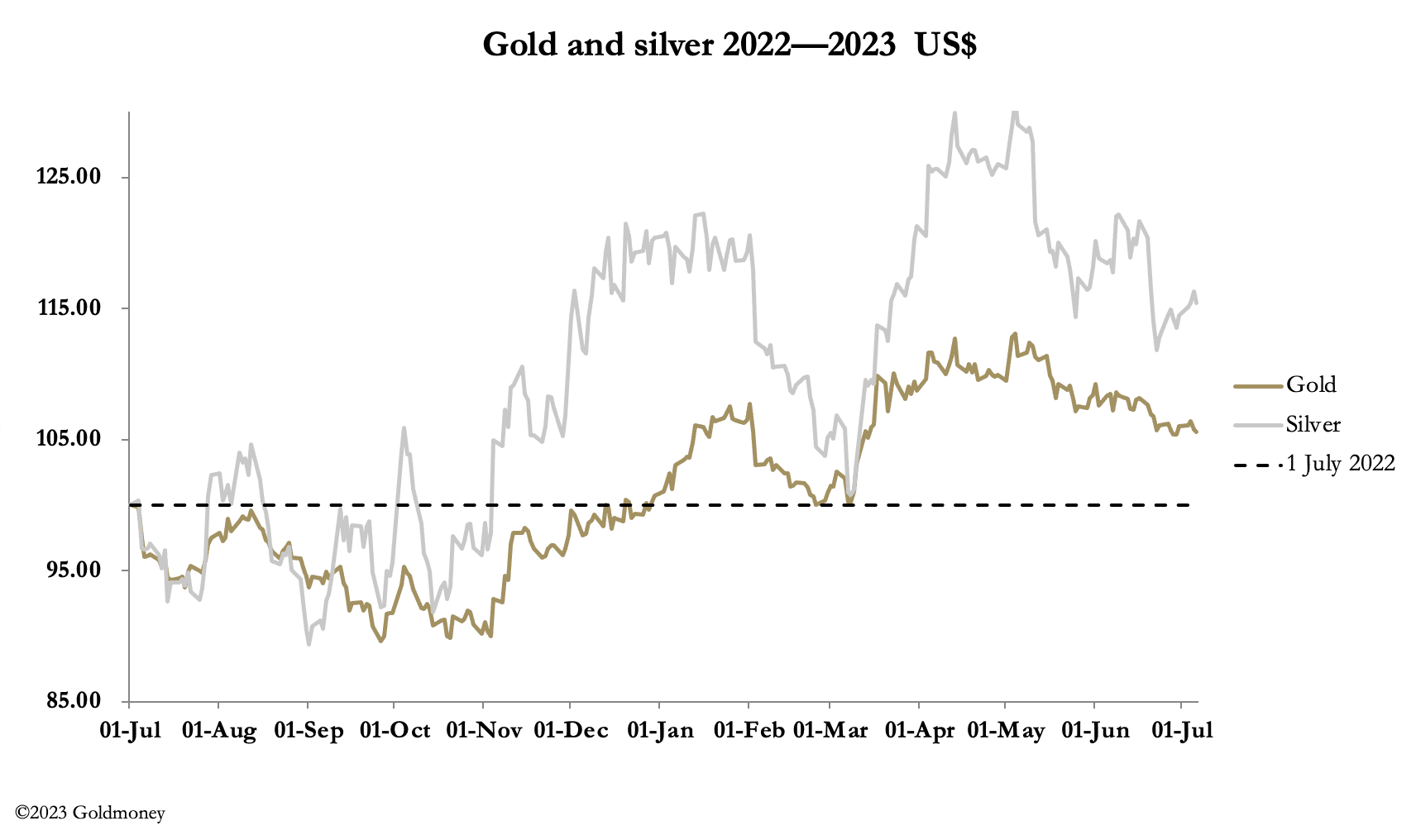

Gold and silver were hardly changed on the week, drifting lower on balance over the week. In Europe this morning, gold was at $1915, down $4, and silver $22.70, down 5 cents. Trade was light, with Tuesday affected by the US Independence Day closure.

Open Interest on Comex remains very low for both metals, though it has begun to creep up in gold. Silver’s OI hit a low of 114,102 contracts, the lowest level for ten years. These charts are next.

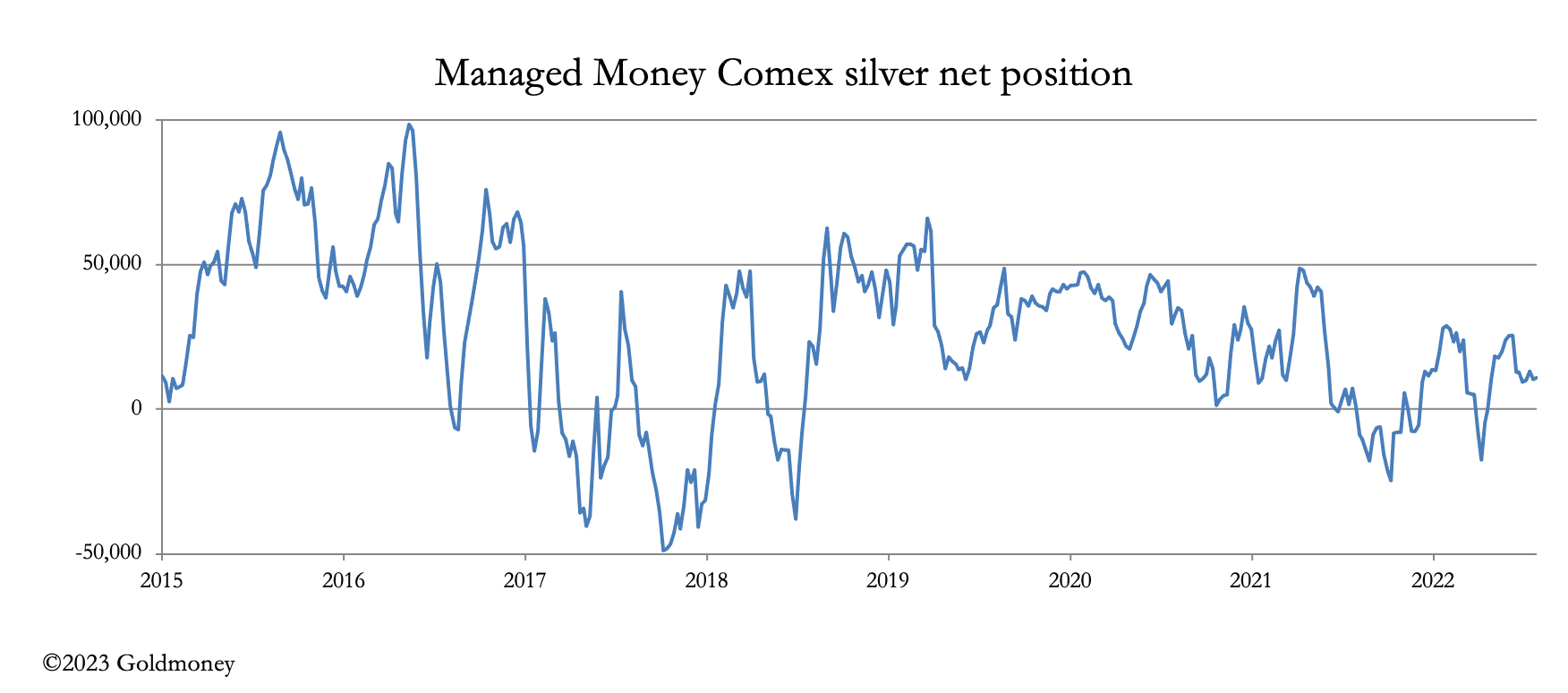

We can generally equate very low Open Interest with oversold conditions. But remarkably, the Managed Money category which can go net short if the hedge funds are collectively bearish, but it is still net long. This is next, showing the position on 27 June, from the most recent COT report.

Technically, there’s room to squeeze the hedge funds even more, but the very low Open Interest suggests that the remaining bulls have become increasingly stubborn.

From the very low level of Open Interest, it would appear that the Swaps, having already shaken out the weak holders now risk a bear squeeze on their silver positions.

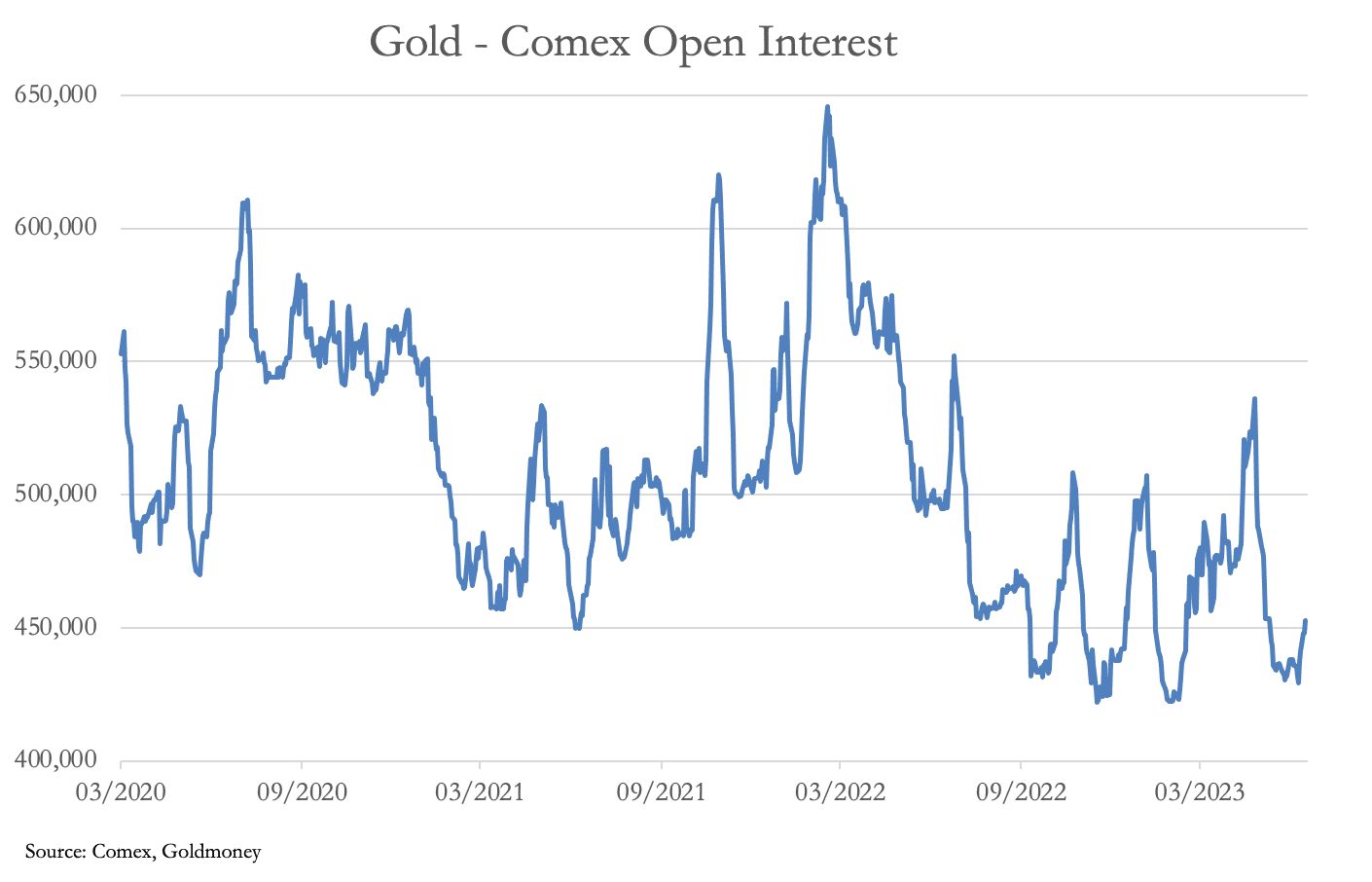

Their position in the gold contract appears to be similar but not as extreme. Even if the gold price falls from here, there are few weak holders left to shake out, leaving the Swaps somewhat stuck. Comex gold Open Interest is next.

From 28 June, OI has increased by some 22,000 contracts, indicating that there is major support at $1900. So, what might drive gold below that level?

The most likely candidate is a new rise in global bond yields. In the last fortnight, the US 10-year Treasury yield has increased by 35 basis points to over 4%, a move echoed in other bond markets. Hopes that recession will allow the Fed to ease off on its tightening policies are evaporating. The dangers of high and yet higher interest rates, the consequences for business failures, and for bad debts in the banking system are becoming evident.

The argument that high interest rates disadvantage gold still gets traction. And the extent to which credit risk escalates initially encourages a flight to the dollar and maybe into short maturity US Treasuries. This means that some of the more stubborn bulls in the Managed Money category could still turn sellers.

But the bullish case is potentially far stronger. Comex is still finding contracts being stood for delivery. Another 1,380 gold contracts (4.3 tonnes) this shortened week and including 30 June, 3,337 silver contracts (519 tonnes) of silver have stood for delivery. Other than an arbitrage between paper and physical, there is the increasing certainty of a new phase in the Ukraine conflict. And then there is the forthcoming BRICS meeting on 22-24 August, when plans for a new trade currency are to be discussed/announced. Depending on how that shapes up, a global de-dollarisation will then dominate markets. It may take a few weeks for the implications to sink in, but then the sell dollar/buy gold trade should get new legs.