Bear squeezes in PMs

Aug 8, 2025·Alasdair MacleodLack of physical liquidity is putting a bear squeeze on gold, silver, and platinum group metal derivatives. After a bullish consolidation, gold, silver, and PGMs are set to resume rising.

Gold improved on last Friday’s sharp rise, up a further $36 at $3400 in Europe this morning, and silver is up $1.40 at $38.40. Yesterday, Comex volumes on both contracts rose sharply. But on preliminary figures, gold’s open interest rose by a large 15,203 contracts, but silver’s fell to the lowest level since 30 May while the price rose 1.1%.

There is growing evidence of bear squeezes. The next chart shows how silver’s price is rising while open interest is falling. Clearly, the shorts are running scared in an illiquid physical market with little or no free float.

Turning to Commitment of Traders statistics, we can see why.

The Swaps who take the short side are close to the highest short level ever, only exceeded in February 2020 when silver was $17.00, after which it spiked down to $11.75. That was a total short commitment of $7.5bn. Today, it’s $14.6bn, and we can be sure that the free float is significantly less.

Silver is just one metal being squeezed higher. Besides rare earths uranium, platinum group metals, lithium, steel, iron ore, titanium and copper (despite its tariff-related sell-off) have all been in bull markets in the past year. This tells us that stockpiling governments and large multinational manufacturers have been selling dollars for tangible metals. Therefore, it is hardly surprising that some metal derivatives are running into trouble.

The shorts in forwards and futures are worried for good reason. In the case of silver, platinum, and palladium short squeezes have the potential to propel prices vertically higher. Silver’s technical chart is next, illustrating the point.

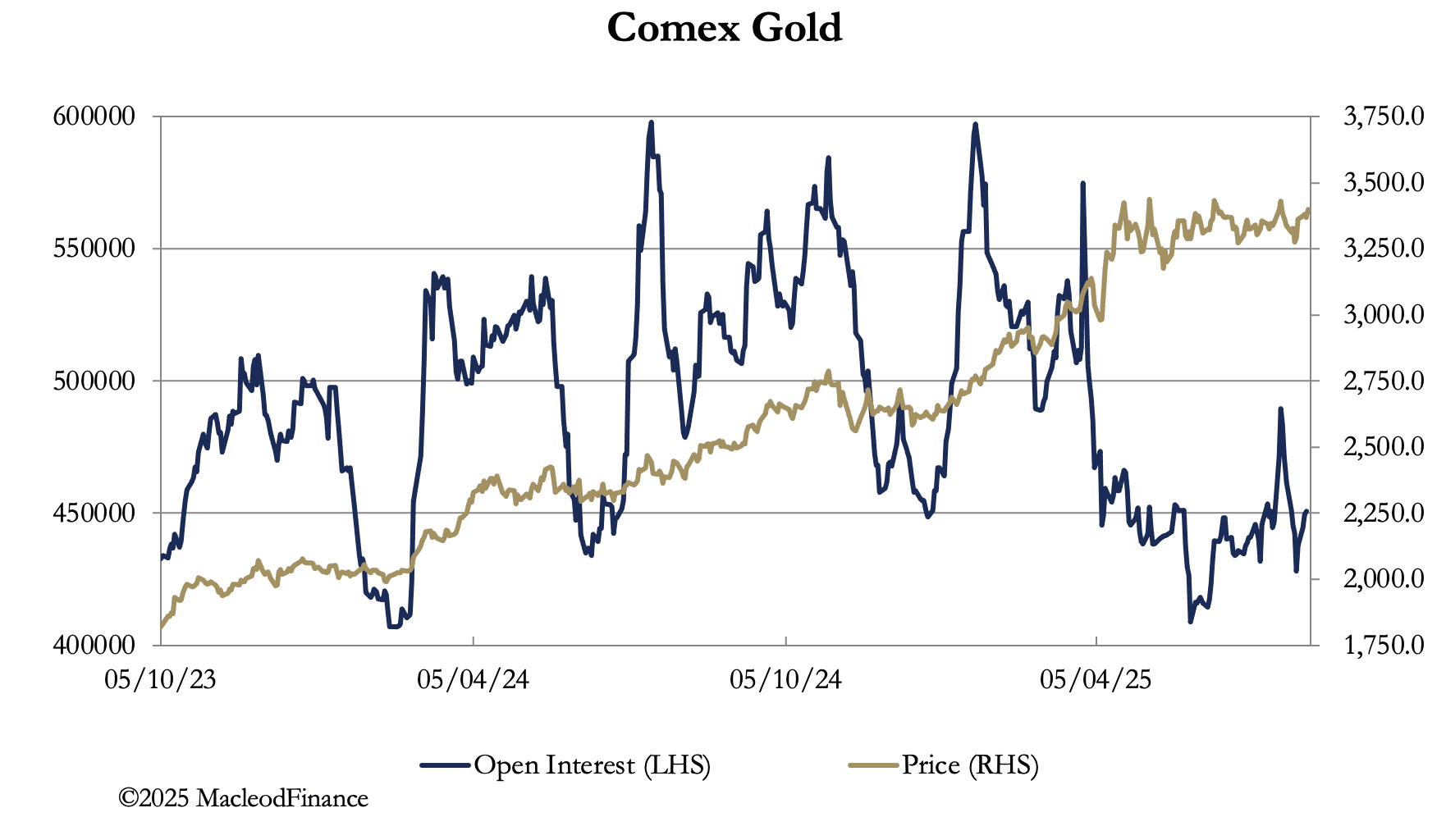

The bear squeeze is also driving gold, with investment participation still unusually low. Next up is Comex open interest in gold and the price.

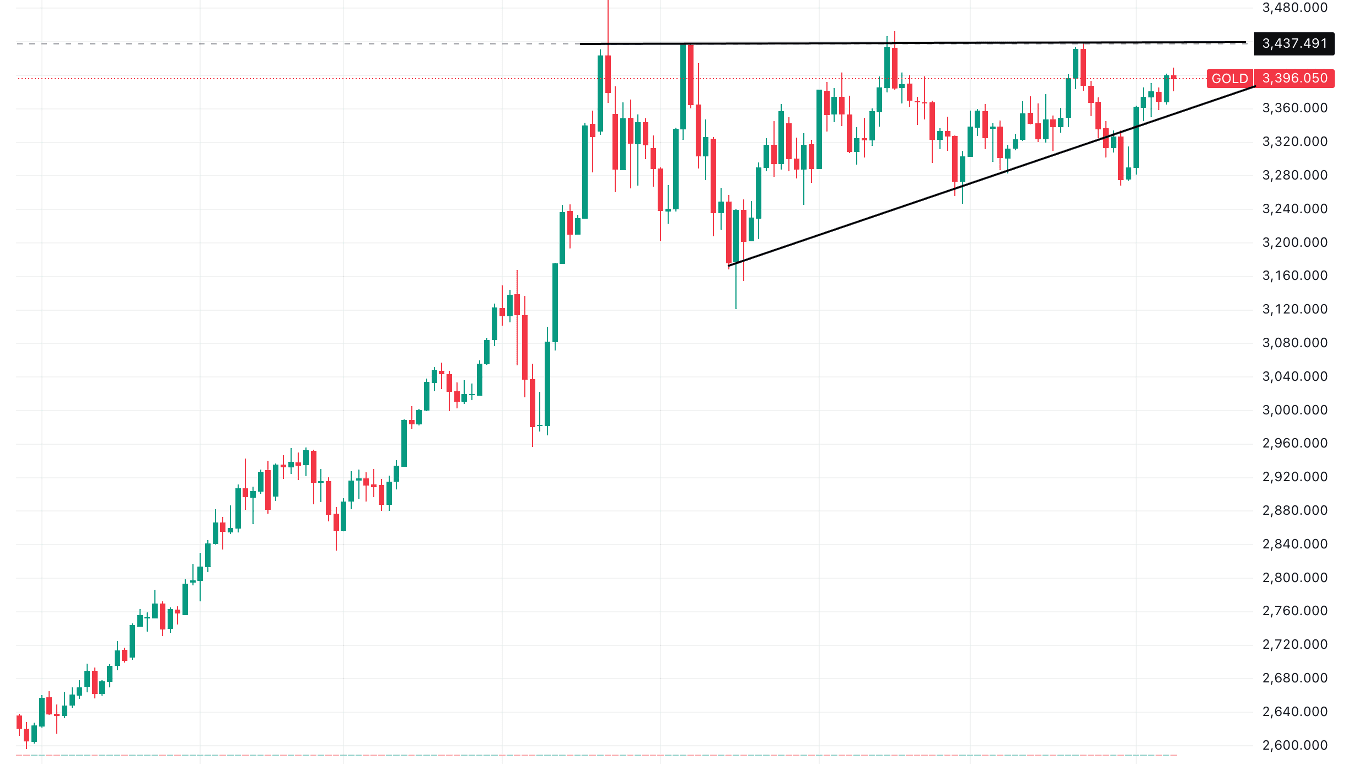

Observe how gold continued to rise despite substantial swings in open interest. More recently, for the last three months gold has consolidated sideways in a narrow range while open interest fell to oversold territory (sub-450,000 contracts). There are signs that this consolidation is now over, and gold is ready for the next bull run. The next daily range chart shows a bullish pennant pattern, which once completed can be expected to see gold rising to well over $4000 by the year end.

The move in (not entirely shown) projects a minimum rise over a similar timescale to the move into the pattern. After the price breaks out on the upside, over $3440, it gives a projected minimum target of $4340. That is purely a technical analysis projection, but it is not hard to see how it might take place.

The move in (not entirely shown) projects a minimum rise over a similar timescale to the move into the pattern. After the price breaks out on the upside, over $3440, it gives a projected minimum target of $4340. That is purely a technical analysis projection, but it is not hard to see how it might take place.

Consider the following:

- The Fed is almost certain to reduce its funds rate by 0.25% in September, despite inflationary pressures. This will almost certainly weaken the dollar.

- Recent job estimates confirm the US economy is sliding into recession while inflationary pressures increase (vide metals and agricultural prices). Forecasts for the US government’s budget deficit are bound to be revised upwards.

- Deteriorating government finances will drive bond yields higher along the yield curve, undermining financial asset values, particularly equities which are expensive at record levels relative to bonds.

- Uncertainty over US tariff policies is undermining global trade, reducing the need for foreign ownership of dollars, being sold to buy physical commodities.

Aside from wilful blindness over bond yields and interest rate outlooks, most of the bullet points are already obvious threats. It is only seasonal lethargy which delays them impacting markets, which we can expect to be corrected as fund managers return to their desks in the next month or so. That breakout in gold’s pennant could be underway by then, ahead of wider developments in financial markets.

Do not be surprised if gold begins to make its move above $3440 next week.