2022 H2 beckons

Jul 1, 2022·Alasdair Macleod

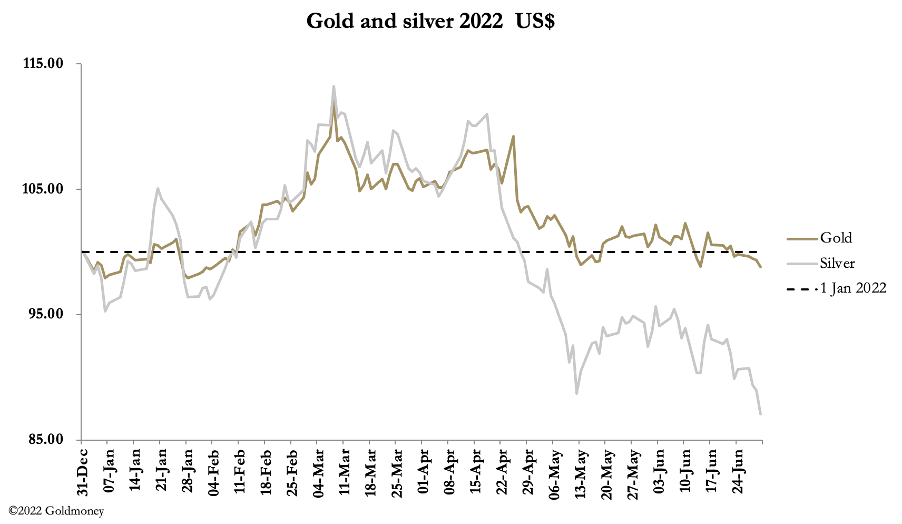

Gold and silver fell sharply this week into the half-year end, as recession scares mount. This morning, in early European trade gold was $1796, down $36 from last Friday’s close, and silver was $19.80, down $1.25. Gold is now slightly below last year’s closing level, and silver is down 15%.

The wider commodity complex also sold down as markets are readjusting their expectations from outright inflationary conditions to growing evidence of a global recession. This is reflected in the chart of a broad-based commodity ETF.

Weakness in precious metals, and for that matter the broader commodity complex, owes much to the banks which run short positions managing half-year mark-to-market values. While they make substantial profits trading derivatives of not just gold and silver, but energy and base metals as well, it is always against a background of short positions. It is at moments such as quarter and half year ends that we often see prices fall significantly as market expectations are carefully managed. Our next chart reflects the gross and net short gold futures positions of the Swap category on Comex, which is mostly bullion bank traders.

Since March, the Swaps’ gross shorts have declined by over $25bn in value, and net of their longs by $21bn. Now that today (1 July) marks the start of H2 2022, could we be close to a turning point?

There is little doubt that market sentiment for gold and silver is at an extremely low ebb. In Comex silver, for example, the Swaps are net long about 4,000 contracts, the short positions carried by hedging producers. We are in a classic sell-off, the condition when all news seems to work against gold and silver and the bulls capitulate. The bullion banks will still want to see lower prices, so the sell-off might not be over yet. But it is getting close.

There is a silver lining. Over-extended banks are reducing their balance sheets, so pressures on trading desks of all sorts to close their positions are growing. Losses incurred are becoming a secondary factor as bank treasurers seek to withdraw from funding financial activities altogether. Not only is this leading to liquidation of bonds and equities held by customers, but also of the banks’ own positions. The fall in lending toinvestors is our next chart, and we can expect its downtrend to continue.

The forces contracting available finance backing for holdings of bonds and equities applies to derivatives as well. In bonds and equities, the prospect is for market making liquidity to reduce as selling intensifies. It works the opposite way for commodities because it is artificial supply that’s being withdrawn, not finance backing long positions.

The ability of the system to control or suppress commodity prices will be compromised by these developments. Market failures, such as the recent nickel spike on the LME, are likely to become more frequent.

In addition to the effects of failing currencies on prices, the second half of 2022 could turn out to be spectacular for gold and silver.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.