Market Report: Lull between bulls and bears

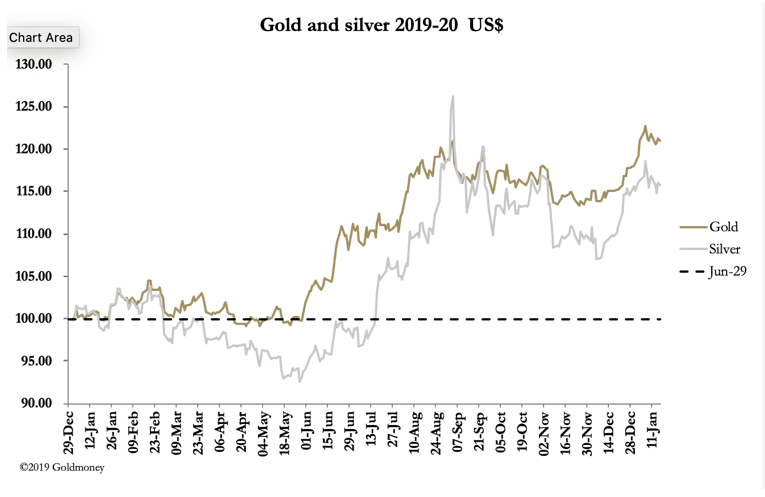

Jan 17, 2020·Alasdair Macleod Gold moved sideways this week in a tight range. The story for silver was the same, but with a little more volatility, as one would expect. By morning trading in Europe, gold had lost $7 from last Friday’s close to trade at $1555, and silver nine cents at $18.01.

Gold moved sideways this week in a tight range. The story for silver was the same, but with a little more volatility, as one would expect. By morning trading in Europe, gold had lost $7 from last Friday’s close to trade at $1555, and silver nine cents at $18.01.Gold’s open interest on Comex rose to just under 800,000 contracts on Thursday, yet another all-time record, and this was despite 32,227 missing contracts recorded as exchanged for physical in the four sessions to Thursday. It really is a high-stakes battle between the bulls and the bears and surely, the shorts must be very concerned because their tactics of using any good news to force the speculating bulls to sell have so far failed.

A key assumption for the bullion banks is that with respect to gold the speculators are always addicted to hopium, and therefore are predictable and can be controlled. But now that the world is showing signs of sliding into a recession, central banks are racking up the money-printing to prevent it. In the case of the US, and therefore for the dollar, the Fed is feeding temporary liquidity into the system through the repo market.

The Fed appears to be creating a new problem for itself, because traders increasingly believe that equities are hitting new records because some of that repo liquidity is fuelling stock prices. In future, if the Fed wishes to reduce its repo operations it will almost certainly be faced with an overvalued stock market crashing.

As a matter of monetary policy, that cannot be permitted.

Another way of looking at the problem is that by injecting repo liquidity into the system, the Fed is suppressing interest rates to below where they would otherwise be to maintain overnight rates at the Fed Funds target rate. And that plays into a rising gold price.

The missing ingredient has been a widespread understanding that this is the case. That ingredient is still missing in the public’s mind, evidenced by the lowest sales of gold eagles for a very long time. But some of the brighter minds in the gold markets are beginning to realise that so long as the Fed continues to suppress overnight rates to the FFR, then gold can only go up. This is why the bullion banks increasingly realise the danger; but they are stuck with massive shorts proving impossible, or at least very difficult, to unwind without moving the market against themselves. Not even a record Comex open interest of 800,000 contracts, plus short positions in London and shorts on their unallocated client accounts, are containing the increasing demand for paper and physical gold.

The only hope for the bullion bears is that the current round of monetary reflation will stimulate the economy and allow the Fed to normalise both its balance sheet and interest rates. The chances of that happening appear to be receding, in which case the gold price is too low.

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.