Inflation, recession, and new currencies

Jun 30, 2022·Alasdair MacleodCentral bankers are trying to steer markets away from higher interest rates, citing growing evidence of the harm they are doing to economic growth. Quantitative tightening is dead on arrival.

Predictably — because it is a repetitive cycle — bank credit is beginning to contract. But contracting bank credit is associated with periodic systemic crises. The credit contraction crisis promises to be even worse than the Lehman failure and any that came before it. And because central banks are sure to protect financial asset values from collapsing, their currencies are likely to suffer instead. Being entirely fiat unbacked by legal money, currencies are dependent entirely on the public faith in a financial system which lacks the backing of real money.

We are all rapidly drifting onto the rocks which sank John Law in 1720. Central bankers, like John Law with his Mississippi bubble, are prioritising support for financial asset values over their currencies, which is what interest rate suppression is all about. Just as Law’s fiat livres rapidly became worthless, so will today’s fiat currencies.

Therefore, in the interests of one’s own self-protection, it is time to fully understand the difference between legal money, fiat currency and the importance of bank credit.

Central banks refuse public access to legal money, which is their gold reserves. Nor is access demanded by the investment establishment, which has thrived on monetary inflation. Instead, there is a developing debate about collapsing currencies being backed by commodities instead. This article puts these developments into context.

Macroeconomic policies are to blame for the crisis

It is a mark of how bad the condition of Western economies has become when interest rate rises of only a per cent or so is enough to expose their fragility. The blame can be laid entirely at the door of neo-Keynesian macroeconomic beliefs. And like a dog with a bone, their high priests refuse to let them go. They would now have you believe that inflation is transient after all. They say that interest rates have risen enough to tip the world into recession.

In this way of thinking, it is either inflation or recession, not both. A recession is falling demand and falling demand leads to falling prices, according to macroeconomic notions. When both inflation and a recession are present, they cannot explain it and does not accord with their computer models. Therefore, government economists insist that consumer price rises will return to the 2% target, because rising interest rates will trigger a recession and demand will fall. It will just take a little longer than they originally thought.

They now say that the danger is no longer inflation. Instead, interest rate policy must take the growing evidence of recession into account, which means that bond yields will stop rising and after their recent correction equity markets should stabilise. For them, this is the road to salvation.

What is really happening is that bank credit is now beginning to contract. Bank credit represents roughly 90% of currency and credit in circulation and its contraction is a serious matter. It is a change in bankers’ mass psychology, where greed for profits from lending, satisfied by balance sheet expansion is replaced by caution and fear of losses, leading to balance sheet contraction. This was the point behind Jamie Dimon’s speech at a banking conference in New York earlier this month, when he modified his description of the economic outlook from stormy to a hurricane. It is the clearest indication we can possibly have of where we are in the cycle of bank credit.

So, even though their analysis is flawed, macroeconomists are very worried. Nine-tenths of US currency and bank deposits face a meaningful contraction. At the beginning of a credit downturn, it is revolving credit which is first curtailed, hitting businesses which are cashflow deficient. This is a particular problem following covid lockdowns and for businesses affected by supply chain issues. Then, the easiest loans to call in those financing positions in financial assets —bonds and equities. And it is also a simple matter to call in and liquidate financial asset collateral when loans begin to sour. And goodness knows, modern economies are exceptionally exposed to accumulated malinvestments.

Central banks see these evolving conditions as their worst nightmare. They are what led to the collapse of thousands of American banks following the Wall Street crash of 1929-1932. In blaming the private sector for the 1930s slump which followed and was directly attributable to the collapse in bank credit, central bankers and Keynesian economists have vowed that it must never happen again.

But because this tin-can has been kicked down the road for far too long, we are not just staring at the end of a ten-year cycle of bank credit, but potentially at a multi-decade super-cyclical event, rivalling the 1930s, and given the greater elemental forces today potentially worse than that.

We can all understand that unless the Fed and other central banks lighten up on their restrictive monetary policies, a stock market crash is bound to ensue. And this is what we have seen, with the Fed funds rate only increasing by a paltry 1 ½% in the last year — an inadequate response to official US consumer prices rising 8.6% so far. Being forced into rethinking its priorities, preventing a stock market crash is now more important for the Fed than managing the economy’s financial condition. It is not that the Fed doesn’t care, it’s because their cherished neo-Keynesian philosophies are at stake.

Consequently, while we can see the dangers from contracting bank credit, we can also anticipate that the Fed and other major central banks will be pulling out all the currency and credit stops to support markets. Not least because rising bond yields to reflect a CPI rising at 8.6% and going even higher add significantly to the Federal Government’s budget deficit.

In effect, the macroeconomic establishment is making a predictable choice of prioritising the prevention of bank credit deflation over supporting their currencies. Realistically, it has no option but to fight recession with yet more inflation of central bank currency and through further expansion of commercial bank reserves on its own balance sheet.

Besides central bank initiatives to keep bond yields suppressed, runaway government budget deficits due to falling tax income and extra spending to counteract the decline in economic activity will need to be financed. And given that the world is on a dollar standard, in the early stages the Fed will probably assume that the consequences for foreign exchange rates of a new round of currency debasement can be ignored. Currency debasement will be expected to accelerate not just for the dollar, but for all the other major currencies as well keeping their exchange rates in some sort of line.

The macroeconomic establishment is wrong in thinking that the choice is between inflation or recession. It is not a choice. A contraction in commercial bank credit and an offsetting expansion of central bank credit will almost certainly take place. The former leads to a slump in economic activity and the latter is a commitment too large for an inflating currency to bear. It is not stagflation, a condition which according to neo-Keynesian beliefs should not occur, but a doppelgänger rerun of what did for John Law and France’s economy in 1720. The inconvenient truth is that policies of monetary stimulation invariably end with the impoverishment of everyone.

So, what’s the solution?

To understand the solution, it is important to appreciate that with a sound currency system, which is a currency that only changes in its quantity at the behest of its users, the cycle of bank credit expansion must be restricted. Extreme leverage of asset to equity ratios for systemically important banks of well over twenty times in Japan and the Eurozone are entirely due to central bank policies of suppressing interest rates. It is only by such extreme leverage that commercial banks, which are no more than dealers in credit, can make profits from the slimmest of credit margins when zero and negative deposit rates are forced upon them.

Since bank credit is reflected in customer deposits, a cycle of excessive bank credit expansion and contraction renders a currency fundamentally unsound. The solution advocated by economists of the Austrian school is to ban bank credit entirely, replacing mutuum deposits, whereby the money or currency becomes the bank’s property and the depositor the creditor, with commodatum deposits where ownership remains with the depositor. Separately, under these proposals banks act as arrangers of finance for savers wishing to make their savings available to borrowers for a return.

The problem with this solution is that of the chicken and the egg. Production requires an advance of capital to provide products at a profit in due course. The real world of free markets therefore requires credit to function. And savings for capital reinvestment are also initially funded out of credit. So, whether the Austrians like it or not we are stuck with mutuum deposits and banks which function as dealers in credit. For this reason, I have advocated that the solution to the disruptive cycle of bank credit is to limit its extent by making the owners of banks, including outside shareholders, liable for all losses by removing from lending institutions the protection of limited liability. This would also ensure that banks would become smaller, more local, more specialist, and more numerous. The existence of today’s megabanks and the requirement for a central bank to ensure systemic integrity would fall away, and with it the need for bank regulation. Banks creating credit must stand or fall on only their reputation.

That is as far as we can go with commercial banks and bank credit. The other form of credit in public circulation is the liability of the issuer of banknotes. To stabilise their value, the issuer must be prepared to exchange them for gold coin, which is and always has been legal money. And once the issuer has established sufficient gold reserves, the issue of any additional banknotes must be covered by additional gold backing.

But much more must be done. Government budget deficits must not be permitted except strictly temporarily, and total government spending (including state, regional, and local governments) reduced to the smallest possible segment of the economy. It means pursuing a deliberate policy of rescinding legal obligations for government agencies to provide services and welfare for the people, retaining only a bare minimum for government to function in providing laws and national defence. All else is the preserve of people arranging and paying for services themselves. It means that most bureaucrats employed unproductively in government must be released and made available to be redeployed in the private sector productively.

Given political reality, one can see that this cannot happen, except as a considered response following a major credit, currency, and economic meltdown. It is a case of crisis first, solution second. Therefore, there is no practical alternative to the continual debasement of currencies until their users reject them entirely as worthless.

Currency is not money

The collapse of the currency is all but guaranteed. But currency in circulation is not legal money, being only a form of credit issued as banknotes by a central bank, or the counterpart of bank credit in the form of deposits held for the commercial banks. The facts about money and credit are ignored by the macroeconomic establishment today. Officially and legally, money is only gold coin. It is also silver coin, though silver’s official monetary role fell into disuse in nineteenth century Europe and America.

Gold and silver coin as money were codified under the Roman Emperor Justinian in the sixth century and is still the case legally in Europe today. In English law, the unification of the Court of Chancery and common law in 1875 formally recognised the Roman position, and gold sovereigns, which were the monetary standard from 1820, became unquestionably recognised as money in the legal sense from then on.

Attempts by governments to restrict or ban ownership of gold as money must not be confused with the legal position. FDR’s executive order in 1933 banning American citizens from owning gold did not change the status of money. Nor did other government moves elsewhere. And the neo-Keynesian position doesn’t either. Nor do the claims from cryptocurrency enthusiasts that their schemes are a modern replacement for gold’s monetary role. As John Pierpont Morgan stated in his testimony before Congress in 1912, “Gold is money. Everything else is credit”. He was not expressing an opinion but stating a legal fact.

That gold does not commonly circulate as a medium of exchange is explained by Gresham’s law, which states that bad money drives out the good. Originally describing the difference between clipped coins and their intact counterparts, Gresham’s law also applies to gold’s relationship to currency. We hoard gold coin, spending currency banknotes and bank deposits instead, being lower forms of media of exchange. Even central banks hoard gold. And as they have progressively distanced themselves from their roles as servants of the public, they refuse to allow the public to exchange it for banknotes.

The importance of gold as a store of value, that is sound money, appears to be difficult to understand for people not accustomed to regarding it as money. Instead, they regard it as a speculative investment, which can be held in securitised or derivative form while it is profitable to do so. When it comes to hedging a declining currency’s purchasing power, the preference today is for assets that outperform the cost of borrowing. As an example of this, Figure 1 shows London’s residential housing priced in fiat sterling and gold. Housing is the most common form of public investment in the UK, further benefiting from tax exemptions for those who live in them.

According to government data, since 1968 when house price statistics began median house prices in London have risen on average by 115 times. They have probably risen more in London than elsewhere in the UK. But measured in gold, they have risen only 29% in 54 years. With prices having generally risen by less outside London and its commuter belt, some areas might have seen falls in prices measured in gold.

It is virtually impossible to get people to understand the implications. They point out the utility of having somewhere to live, which is not reflected in prices. And if you say that does not apply to property held by landlords, they respond that it then produces a rental income. Furthermore, most buyers leverage their investment returns by having a mortgage.

In investing terms, these arguments are entirely valid. But they only prove that the purpose of owning an asset is to obtain a return or utility from it, with which we can all agree. The purpose of money or currency is different: it is a medium for purchasing an asset which will give you a benefit. What is not understood is that far from giving property owners a return which exceeds the debasement of the currency, they have just about kept pace with it. And if you had bought property elsewhere in the UK, your capital values could have fallen, measured in real legal money, which is gold.

We are now on the cusp of a major currency upheaval. The global banking system is more highly leveraged on balance sheet to equity measures than ever before, and bank credit is beginning to contract. Systemic risks are escalating, even though market participants have yet to realise it. And as economic activity turns down, government budget deficits are going to rapidly escalate. A practical remedy for the situation cannot be entertained, so the debasement of currencies is bound to accelerate. Mortgage borrowing costs are already rising, affecting affordability of residential property in fiat money terms.

The relationship between currency and real money, which is gold coin, will certainly break down. With some ups and downs, the depreciation of currencies against gold has been otherwise a gradual process since the Bretton Woods agreement was suspended in 1971, but that reasonable process is ending. Measured in gold, a banking and currency crisis will have the effect of driving residential property prices significantly lower, while they could be maintained or even move somewhat higher measured in more rapidly depreciating fiat currencies.

Will the transition to commodity-backed currencies save them?

Given that the slump in economic activity will lead to a decline and collapse in purchasing power for the West’s major currencies, it would be logical for the gold-rich Russia-China axis and nations in their sphere of influence to protect their own currencies from this rapidly developing catastrophe. So far, none of them appear to be prepared to do so by introducing gold standards. A few of them are only acquiring additional gold.

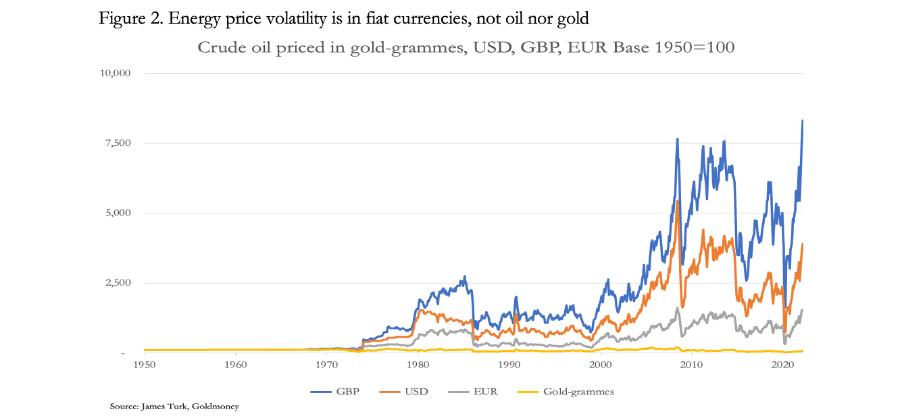

Only Russia, under pressure from currency and trade sanctions has loosely tied its rouble to energy and commodity exports. In the vaguest of terms, it might be regarded as a synthetic equivalent of linking the rouble to gold. Why this is so is illustrated in Figure 2.

Measured in fiat currencies, the oil price is exceedingly volatile, while in true money, gold, it is relatively stable. Measured in gold, the oil price today is just 30% lower than in 1950. Since then, the maximum oil price in gold has been a rise of 107%, and the minimum a fall of 85%. That compares with a rise in US dollars of 5,350% and no fall at all. Undoubtedly, if gold had traded free from statist intervention and the effects of fiat-induced economic booms and busts, the price of oil in gold would most likely have been even steadier.

The Eurasian Economic Union (EAEU), consisting mainly of a central Asian subset of the Shanghai Cooperation Organisation (SCO) has announced plans for a trade settlement currency backed by a mixture of commodities and the currencies of member states. But other than Russia, none of them have announced any plans to protect their own currencies from a Western currency crisis.

So far, members of the SCO have discussed ways of escaping the dollar for the purpose of transactions between them, a long-term project driven not so much by change in Asia but by the failures of American hegemonic policies over time. Following Russian sanctions by the West, it is likely that the dangers of a more immediate dollar crisis are now being discussed in governments and central banks throughout Asia. And the lessons from sanctions against Russia are that reserves held in western currencies can become worthless by diktat.

Yet, there is no sign of these states protecting their own currencies with their gold reserves, or alternatively through some sort of commodity backing.

With the West plunging into a combined systemic and currency crisis, no national government outside the dollar-based system appears to know what to do. Only Russia is being forced by its circumstances into action. Even the Russians are feeling their way, with vague reports that they are looking at a gold standard solution, and others that they are considering Sergey Glazyev’s EAEU trade currency project. Glazyev is a senior economic advisor to Vladimir Putin.

It appears that Glazyev’s EAEU monetary committee has ruled out a gold standard for the new trade currency. Instead, it has been considering alternative structures for some years now without agreement. But for this project to go ahead, proposals reported to include national currencies in its valuation basket must be abandoned. Not only is this an area where Glazyev is unlikely to obtain a consensus from member states, but to include a range of fiat currencies is unsound and will not satisfy the ultimate objective, which is to find a credible replacement for the US dollar for cross-border trade settlements which can be easily joined by other states in the wider SCO and elsewhere.

So long as the trade currency is set by a daily, or twice daily fixing against all member currencies and it does not circulate as a medium of exchange in domestic economies, there seems no reason why it cannot work purely for trade settlement purposes. For it to be widely adopted it must be enshrined in law, stable, seen as a reliable store of value, and even a refuge from fiat currency volatility. In short, it must be a credible alternative for a medium of exchange backed by gold.

Therefore, it must not include commodities of a seasonal nature, such as grains. Nor can it be constructed with reference to national commodity volumes. It can only consist of an unweighted basket of commodities for which daily or twice daily prices can be obtained. Given that gold is not being considered for this role, the objective must be to replicate gold as a close alternative. Only then, might it drive the depreciating dollar out of its hegemonic role in Asia.

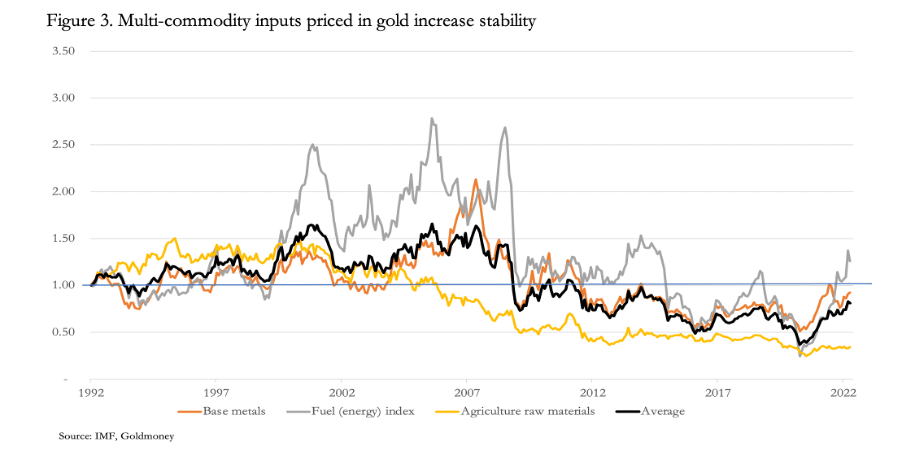

Figure 3 shows a practical example of how such a currency might be constituted. It shows price indexed data based in US dollars converted to prices in gold.

The IMF’s data[i] covers several sectors, but the three selected appear to be the most suitable. Base metals, fuel (energy), and agriculture raw materials represent nineteen sub-components. Not all the subcomponents are necessarily continually priced, so this can only be an illustration of the principals involved. The black line is the average of the three sectors priced in gold, which other than fuel (energy), have demonstrated relatively low volatility.

Since 1992, the average gold value of the three sectors has fallen 19% (the black line) and has shown extremes of a rise of 66% and a fall of 63%. Given that the distortions from the fiat world on both commodities and gold will have caused much of the volatility, Figure 3 shows that a basket of suitable commodities can act as a synthetic equivalent of gold-backing for a trade settlement currency.

If he is to implement such a standard, Glazyev must do what Ludwig Erhard as West Germany’s Economy Minister did in June 1948: present thought-out proposals on the lines above as a fait accompli and then get EAEU members to sign up to it.

Importantly, there is unlikely to be any meaningful opposition to such a plan because it does not involve domestic currencies, apart from a commitment of central banks to always convert it to and from their domestic currencies. Importantly, it does not involve central banks of participating states contributing their own gold reserves. It removes the costs of double-currency settlements involving the intermediation of the dollar and the US banking system. It has the potential to achieve precisely what the EAEU and the members of the SCO want, which is to remove dollar hegemony from their trade. All that the participating central banks will be required to do is to undertake the exchange of their currencies for the new trade currency on demand. It should amount to little more than a one-page agreement between each participating central bank and an overseeing authority.

Commercial banks will be able to maintain deposit accounts and make loans in the new trade currency. But this credit business must be strictly limited to trade finance to ensure it is used for cross-currency trade only. It cannot be a form of backing for any national currency.

Conclusion

We have noted the deteriorating systemic and monetary prospects for fiat currencies, predominantly those of the dollar-based Western currency system. Sound economic theory indicates that a final crisis leading to the end of these fiat currencies was going to happen anyway, and the financial war against Russia is an additional factor accelerating the collapse.

After suppressing interest rates to zero and below, rising interest rates are finally being forced by markets upon the monetary authorities. With good reason, it has become fashionable to describe developments as an evolution from a currency environment driven by and dependent on financial assets into one driven by commodities — in the words of Zoltan Pozsar, Bretton Woods II is ending, and Bretton Woods III is upon us.

For this reason, there is growing interest in how a new world of currencies based somehow on commodities or commodity-based economies will evolve. In recent months, Russia has successfully protected its rouble by linking it to energy and commodity exports and in the process undermined Western currencies.

While it is always a mistake to predict timing, the fact that no one in the financial establishment is debating how to use gold reserves to protect their currencies clearly indicates that we are still early in the evolution of the developing crisis. The few forward thinkers becoming aware of mounting systemic threats are looking at backing currencies with commodities and not gold standards. They still seem to be unaware of why gold coin is legal money and in their own hubris think their cosy world of inflation-driven financial returns is a step evolution away from the past.

In this article I have shown it is possible to devise a new commodity-backed trade settlement currency, which is not permitted to circulate other than purely for trade settlements. This is not a solution for protecting a currency’s purchasing power in the context of its use as a circulating medium. It is not a model for Russia or China upon which to base their future currency systems. As the West’s fiat currencies sink into the dustbin of history, they will have no alternative but to put their roubles and renminbi onto a proper gold coin standard.

With neither the economic establishment nor the public having a basic understanding of what is money and why it is not currency, it is hardly surprising that current financial and economic developments are so poorly understood, and the correct remedies for our current monetary and economic conditions are so readily dismissed.

[i] See imf.org/en/Research/commodity-prices

The views and opinions expressed in this article are those of the author(s) and do not reflect those of Goldmoney, unless expressly stated. The article is for general information purposes only and does not constitute either Goldmoney or the author(s) providing you with legal, financial, tax, investment, or accounting advice. You should not act or rely on any information contained in the article without first seeking independent professional advice. Care has been taken to ensure that the information in the article is reliable; however, Goldmoney does not represent that it is accurate, complete, up-to-date and/or to be taken as an indication of future results and it should not be relied upon as such. Goldmoney will not be held responsible for any claim, loss, damage, or inconvenience caused as a result of any information or opinion contained in this article and any action taken as a result of the opinions and information contained in this article is at your own risk.